|

CIMC ENRIC(3899)

Analysis:

CIMC Enric Holdings (3899) is primarily engaged in the manufacture and sale of a wide range of equipment and construction for the storage, transportation, application, processing and distribution of clean energy, chemical and environmental, liquid food. For the six months ended 30 June 2022, the Group`s consolidated revenue rose by 12.7% to RMB8,948,693,000. Profit attributable to shareholders increased by 14.6% to RMB439,315,000. Stripping out amortisation of share base incentive scheme expense and convertible bonds related finance expenses, its core profit increased by 34.5% to RMB531,831,000. Gross profit margin improved by 1 ppt to 15.9%. During the first half of 2022, the newly signed orders of the Group totalled RMB10.7 billion, representing an increase of 16.8% compared with the same period last year. At 30 June 2022, the total orders on hand of the Group reached RMB17.3 billion, recording an increase of 41.7% compared with the same period last year. (I do not hold the above stock)

Strategy:

Buy-in Price: $8.30, Target Price: $9.10, Cut Loss Price: $7.80

|

WEIGAO GROUP(1066)

Analysis:

For the six months ended 30 June 2022, revenue of Shandong Weigao Group Medical Polymer (1066) was approximately RMB6,975million, representing an increase of 12% YoY. Net profit attributable to the shareholders was RMB1,459million, representing an increase of 20.6% YoY. If excluding Wego Blood Purification issued new shares to investors, resulting in a one-time gain, net profit was RMB1,391million, representing an increase of 15.0% YoY. During the Period, the clinical care business recorded a turnover of RMB2,298million, representing an increase of 9.2% YoY. The pharmaceutical packaging business recorded a turnover of approximately RMB1,056million, representing a growth of 10.3% YoY. The orthopaedic business recorded a turnover of RMB1,091million, representing an increase of 0.6% YoY. The interventional business recorded a turnover of RMB893million, representing an increase of 3.2% YoY. Meanwhile, Weigao newly added 388 hospitals, 8 other medical institutions and 217 distributors to its PRC customer base. As at the date of 30 June 2022, company has a PRC customer base of 8,595 in aggregate and an overseas customer base of 6,953 in aggregate. The national healthcare reform policies entered into full implementation continuously. The negotiations on medical insurance, the seventh round of centralised procurement, the volume-based procurements of high-value consumables and DRGs/DIP are exerting farreaching influence on the medical industry. In the orthopaedic segment, new prices will be implemented one after another after the completion of national and regional centralised procurement of joints, trauma and other products. The national volume-based procurement procurement of spine was also actively promoted, which is expected to be completed by the end of this year. In the clinical care segment, the volume-based procurement of different products will be promoted in various provinces continuously. Through various means such as the upgrading and updating of products, cost control and expansion of grass-roots markets, expected that Weigao would further expand its market share.

Strategy:

Buy-in Price: $10.44, Target Price: $11.20, Cut Loss Price: $9.80

|

|

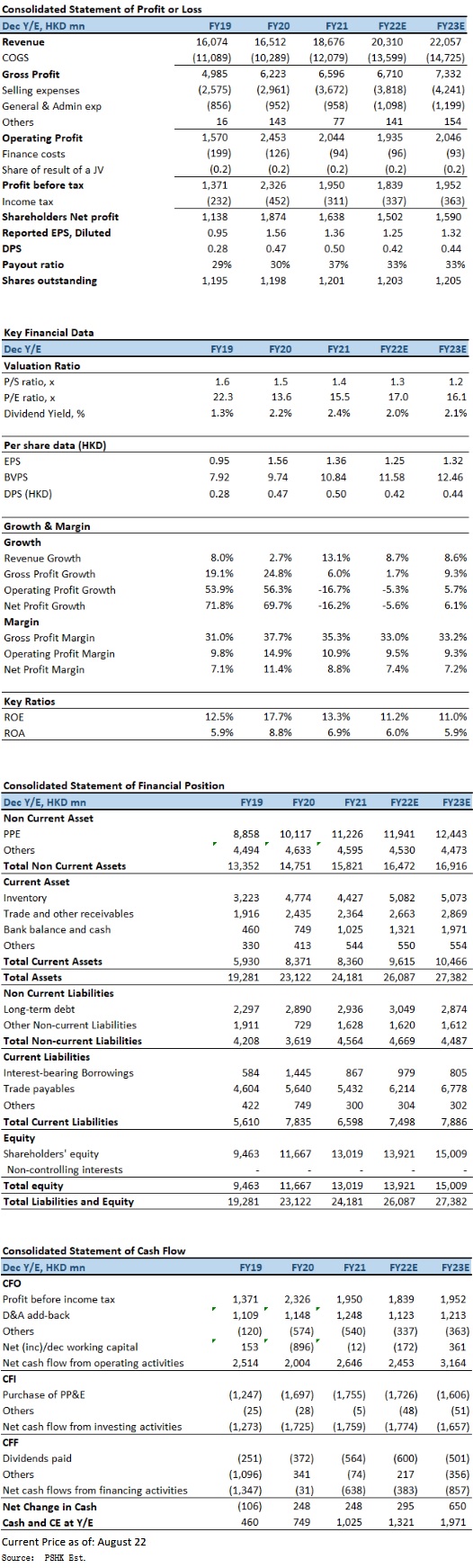

Vinda International (3331.HK) - Focus on Premiumization, implement pricing initiatives to mitigate costs increases

Focus on premiumization, implement pricing initiatives to mitigate costs increases For 1H2022, total revenue of Vinda International increased by 6.6% (growth at constant exchange rates:6.9%) to HK$9,680mn. Overall revenue in 1Q2022/2Q2022 was HK$4,566mn (+2.2%YoY) and HK$5,114mn (+10.8%YoY) respectively. Net profit declined by 34.1% to HK$638mn. Net profit for 1Q2022/2Q2022 was HK$344mn (-37.8%YoY) and HK$294mn(-29.1%YoY) respectively. The net profit margin narrowed by 4.0ppts to 6.6%. Basic EPS was 53.0 HK cents (1H2021: 80.6 HK cents), with interim dividend of 10.0 HK cents per share for the Period. In terms of business segment, the tissue segment accounted for HK$7,963mn of revenue, an increase of 6.1% YoY or 5.9% at constant exchange rates, representing 82% of the total revenue (1H2021: 83%). Focus on premiumization strategy has contributed to an increased share of premium portfolio. This effort to drive higher category margins helped to soften the impact of rising raw material costs and promotional pressures. However, gross margin of the tissue segment was still dropped to 31.6% (1H2021: 37.8%). Revenue from the personal care business increased by 9.0% to HK$1,717mn in 1H2022, which was a 11.7% increase at constant exchange rates and represented 18% of the total revenue (1H2021: 17%). Gross margin of the personal care segment was 34.1% (1H2021: 35.3%). In terms of sales channel, traditional channel, key accounts managed supermarkets and hypermarkets, B2B corporate clients and e-commerce platforms accounted for 26%, 23%, 10% and 41%, respectively, of the total revenue. As the dominant consumption channel, e-commerce revenue recorded an organic sales increase of 14.3%. Gross profit was down by 8.7% to HK$3,100mn. Gross profit was negatively impacted by input costs pressures such as raw material, energy and distribution costs. Vinda took decisive actions including multiple pricing initiatives in mitigating input cost pressures. Although other mechanisms such as disciplined cost management and continuous product mix improvement were also deployed, gross margin was still dropped 5.4ppts to 32.0%. Company valuationCOVID containment measures in mainland China in response to COVID-19 resurgence has led to lower demand and logistic disruptions, Vinda's earnings were also negatively impacted by continuous rise in input (wood pulp prices at high levels) and logistic costs. However, the overall sales performance remained resilient. In addition, believed that Vinda will continue to implement pricing initiatives, and enhance cost management, to mitigate headwinds from raw material and other input costs increases, and expects that this unfavorable situation will be alleviated in the second half of the year. We expect FY2022E-FY2023E EPS to HK1.25 and HKD1.32 respectively, with TP HKD21.0, implies a FY2022E P/E of 16.8x, in line with its 5-years average. Our investment rating is “Neutral”. Risk factors1) Resurgence of COVID-19 in China; 2) Large fluctuations in wood pulp prices; 3) Economic recovery momentum slower than expected, consumer confidence weakens further; and 4) Industry competition is intense than expected. Financial

Click Here for PDF format...

| Recommendation on 31-8-2022 | | Recommendation | Neutral | | Price on Recommendation Date | $ 21.200 | | Suggested purchase price | N/A | | Target Price | $ 21.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|