China SSS growth returned to positive in June

Chow Tai Fook Jewellery (CTF) announce certain unaudited key operational data of the Group for the three months ended 30 June 2022 (1QFY2023), with both Mainland China and Hong Kong and Macau recorded negative SSSG. Retail Sales Value (RSV) decreased 3.7% YoY, due to the resurgence of the pandemic and a high base of comparison.

1QFY2023, by region, Mainland China RSV recorded –2.8% YoY, with contribution to group RSV 89.9%. Same Store Sales (SSS) dropped by 19.3% YoY and SSS volume growth decreased by 22.8% YoY. Yet, sequential improvement was seen with June SSSG returned to positive. In Hong Kong and Macau, RSV dropped by 11%, contribution to group RSV 10.1%. SSS declined by 6.4% and SSS volume growth decreased by 8.4%. Hong Kong's SSSG was 7.3% in the Quarter, estimated to be driven by consumer coupons. Macau registered a negative SSS of 34.3% as tourist traffic reduced due to the pandemic in the Mainland.

In the Mainland, SSS of gem-set, platinum and k-gold jewellery category dropped by 17.2%, while its RSV decreased 6.3% during the Quarter. SSS of gem-set, platinum and k-gold jewellery category in Hong Kong and Macau declined by 18.4% during the Quarter. Same Store Average Selling Price (“ASP”) trend of gem-set jewellery was stable in both markets during the Quarter. In the Mainland, Same Store ASP remained at HK$7,300 (1QFY2022: HK$7,300) while that of Hong Kong and Macau increased to HK$16,500 (1QFY2022: HK$14,000).

Gold jewellery and products category includes those selling by weight and at fixed price, while the average international gold price in the Quarter was 3.0% higher when compared to the same period last year. In the Mainland, SSS of the product category decreased by 17.0% during the Quarter, yet its ASP was lifted to HK$5,600 (1QFY2022: HK$5,200). In Hong Kong and Macau, SSS of the product category slightly increased by 1.0% and ASP was HK$6,100 (1QFY2022: HK$6,000).

Expansion strategy by leveraging franchisees, domestic consumption is recovering

With continues retail expansion strategy leveraging franchisees` local knowledge, RSV of the franchised portion in CHOW TAI FOOK JEWELLERY increased by 9.4% YoY and its contribution to the RSV of CHOW TAI FOOK JEWELLERY increased to 63.8% (1QFY2022: 57.6%) in the Mainland during the quarter. Smart retail (includes RSV contributed from e-commerce and smart retail applications. Major e-commerce platforms included Chow Tai Fook eShop, Tmall, JD.com, Vipshop; Smart retail applications refer to the use of digital tools, such as CloudSales 365, Cloud Kiosk, Smart Tray, etc) RSV in Mainland China decreased by 23.9% YoY yet its volume recorded an increase of 6.7% in the First Quarter. However, its contribution to Mainland China's RSV was 7.5% in the Quarter of which 1.6% was contributed by smart retail applications.

During the quarter, Chow Tai Fook added a net of 312 POS in Mainland China, including 338 net POS openings of CHOW TAI FOOK JEWELLERY (24 self-operated stores and 314 franchised stores). As at 30 June 2022, 74.7% of our CHOW TAI FOOK JEWELLERY POS in the Mainland were in franchised format. In Hong Kong & Macau of China and other markets, the group closed 1 MONOLOGUE POS in Hong Kong while opened 1 CHOW TAI FOOK JEWELLERY POS in other markets. As at 30 June 2022, the group had 5,931 CHOW TAI FOOK JEWELLERY POS and 283 POS for other brands in total.

According to the data released by the National Bureau of Statistics of China, the growth rate of total retail sales of consumer goods turned positive in June, from a YoY decline of 6.7% in May to a YoY increase of 3.1%. the growth rate of retail sales of most goods picked up in June; among them, the gold and silver jewelry category grew by 8.1%, significantly better than the -15.5% in the previous month.

Investment Thesis

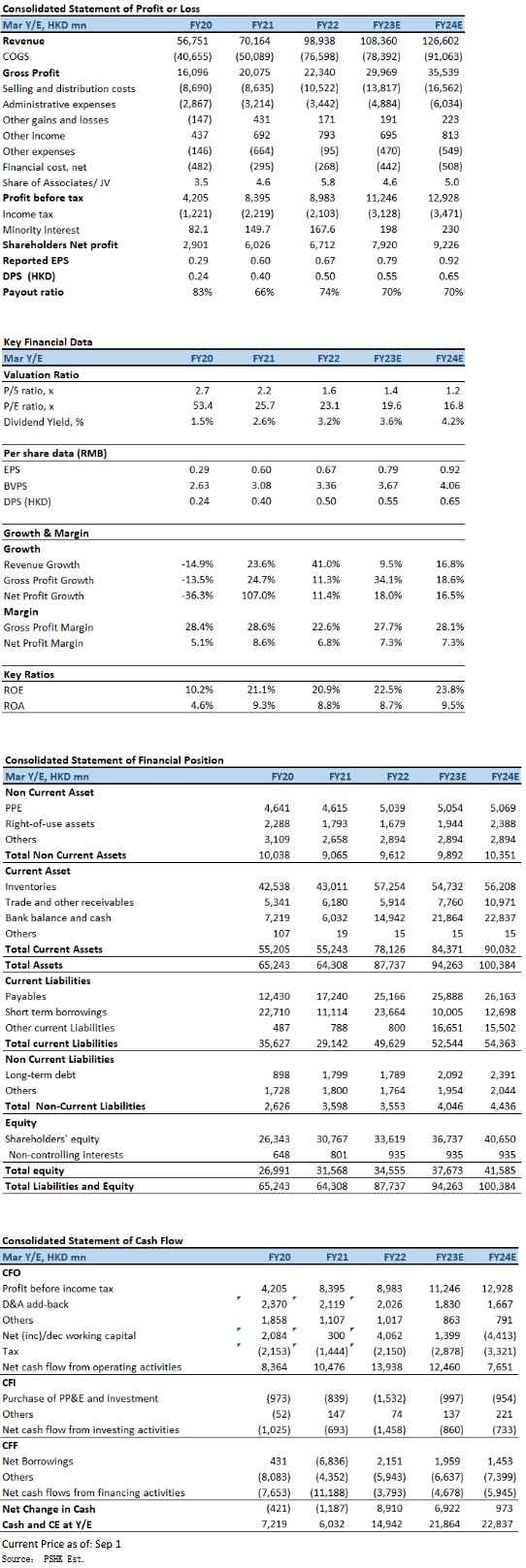

Despite the restrictions eased in China, management pointed out that SSS in China have started to improve month-over-month recently, but the resurgence of COVID variant will remain a near-term risk. We expect FY2023-FY2024 EPS to be HKD0.79 and HKD0.92 respectively, with PT of HKD15.52, implies a FY2023E P/E of 19.6x (~2-yrs historical average). Our investment rating is “Neutral”.

Risk factors

1) Resurgence of COVID in Mainland China; 2) Sharp fluctuations in FX and gold price; 3) Economic recovery momentum slower-than-expected, consumer confidence weak; and 4) higher-than-expected operating costs.

�Financial

Click Here for PDF format...