Company profile:

Founded in 1997, Shanghai Baolong Automotive Corporation started with tire valves. Later, following the automobile development trend, the Company continuously expanded the product line, and successively engaged in wheel weights, exhaust pipes, lightweight structural parts, TPMS (tire pressure monitoring system), as well as the intelligent automotive field of sensors, ADAS (that is, advanced driver assistance systems, mainly based on vision products and millimeter-wave radars), and air suspension.

The Company has manufacturing sites or R&D and sales centers in Shanghai, Ningguo and Hefei in Anhui Province, Wuhan in Hubei Province, the United States, Germany, Poland and Hungary. Its major customers include major global OEMs (such as Volkswagen, Audi, Porsche, BMW, Mercedes-Benz, Geely, Great Wall, Chery, BYD, NIO, Xpeng, and Ideal), tier 1 suppliers (such as Faurecia, Tenneco, BorgWarner, Marelli, Yanfeng, Magna, Continental, Knorr-Bremse, and ZF) and independent aftermarket distributors (such as Discount Tire, TireKingdom, ASCOT, and Würth). With excellent and diversified customer resources, the Company has strong anti-risk ability. The Company raised RMB620 million through an IPO on the Shanghai Stock Exchange in 2017 and raised RMB920 million through a private placement in May 2021 to invest in the R&D of new projects and products.

After more than 20 years of development, the Company is at the forefront of the segment in terms of the market share of traditional business, namely, tire valves, wheel weights, exhaust pipes, and TPMS. With strong competitiveness, the traditional business is currently the main source of revenue and profit. Specifically, the Company has reached top third in the world in terms of the TPMS scale and ranked third in the world in terms of the market share of tire valves, with an annual shipment of more than 30,000 thousand units. The Company's emerging business covers intelligent drive solutions-related parts and hydraulic lightweight structural parts, such as sensors, air suspension, and ADAS. The emerging business is currently the core direction of the Company's vigorous development, and will be an important growth point for future revenue and profit.

With Sound Profitability, the Traditional Business Maintains Steady Growth

The Company's main product technology is leading the industry, passing the Ford Q1, and the certifications of CNAS and General Motors GP-10 system. The perennial high R&D investment (6-7%) has supported the Company's several strategic upgrades, facilitated the continuous expansion of the product line, and brought the sound profitability. The gross margin and net profit margin remained stable at approximately 30% and 10%, respectively, above the industry average. In 2021, the Company's R&D investment accounted for 7.20% of the operating revenue. As at December 31, 2021, the Company and its subsidiaries had a total of 396 domestic and foreign patents.

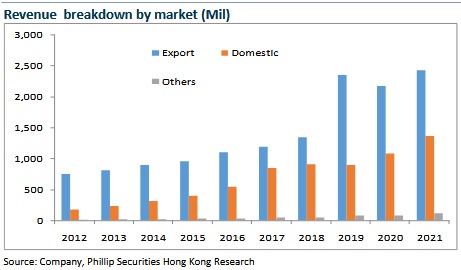

At the beginning of its establishment, the Company mainly engaged in the export of parts, with a high proportion of overseas business. After 2000, it gradually laid out the domestic market, and the proportion of the domestic market increased from 19% in 2012 to 35% in 2021.

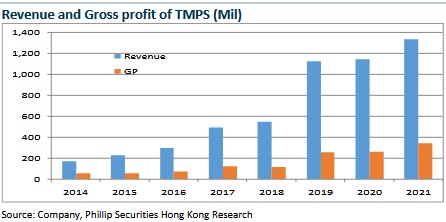

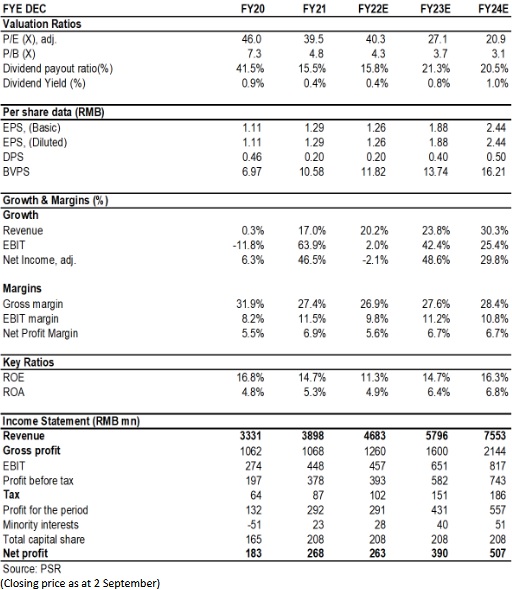

From 2008 to 2021, the Company's revenue rose from RMB608 million to RMB3,898 million. The net profit attributable to the parent company climbed from RMB32 million to RMB268 million. The CAGR was 15.36% and 17.76%, respectively, maintaining stable and rapid growth. In recent years, the rapid growth of TPMS scale is the main reason for the increase in revenue. Since 2010, the United States, the European Union and China have successively announced the regulations on mandatory TPMS installation, which has led to a significant increase in TPMS penetration. As an industry leader, the Company has fully enjoyed the market dividend. The Company's TPMS segment generated a CAGR of 33% in revenue from 2012 to 2021 and currently contributes 1/3 to the gross profit. The Company's share ranked third in the world and first in China after the Company and Huf established a joint venture BH SENS in 2018. In the future, with the integration and exploitation of customer resources and the exertion of scale effects, there is room for further improvement in profitability.

In 2021, the Company reported a gross revenue of RMB3,898 million, a year-on-year increase of 17.01%. Specifically, the revenue from traditional business, namely, tire valves, automotive metal tubing and TPMS, accounted for 18%, 30% and 34%, respectively, the revenue from emerging business accounted for approximately 9%, and that of other business accounted for approximately 9%. During the reporting period, the net profit attributable to shareholders was RMB270 million, a substantial increase of 46.5% year-on-year..

Sensors + Air Suspension Relay the Future High Growth in Results

The Company's emerging business covers sensors, ADAS, air suspension and hydraulic structural parts, all of which are the main directions for future automotive development.

1) Sensors are the terminal of the automobile control system, responsible for sensing and transmitting the operation status of automobiles. They are experiencing a phase of rapid growth from the period of product introduction with the rapid development of the current intelligent drive automobiles. With the core technology accumulated in the TPMS, the Company will extend the development of SoC and other sensor categories with independent intellectual property rights. Meanwhile, the Company's external acquisition of equities in PEX of Germany and Longgan Technology helps it quickly obtain more mainstream customer resources and expand its product line. In the future, the Company is expected to have a share in the automotive sensor market monopolized by foreign capital.

2) Air suspension can improve the controllability, comfort and safety of automobiles, with the advantages of stable vibration isolation, adjustability, good adaptability and sound insulation, and light weight. In the past, it was mainly configured on a small number of luxury models, and the matching price of single vehicle exceeded RMB15 thousand. With the high-end development of new energy vehicles, the demand market for air suspension sinks to mid-end models. The value of single vehicle can drop below RMB8,000. The increase in industry penetration rate is expected to accelerate, which also provides an opportunity for domestic substitution. The Company's air suspension began in 2012. Starting from commercial cars, its customers include ZF, Adient, Goldrare, and Shanghai Komman Vehicle Component Systems Co., Ltd. The Company began to enter the passenger car market in 2017. It currently has obtained the fixed-point projects of five leading new energy vehicle enterprises, and has successively won orders. According to the Company's announcement, the total order amount has accumulated RMB782 million since October 2021. The Company's current production capacity of air suspension is approximately 100 thousand units. It plans to increase the production capacity by 400 thousand units in the future. With the accelerated implementation of orders and production capacity, the revenue of air suspension is expected to reach RMB2 billion in 2024, accounting for half of the gross revenue in 2021.

3) Intelligent drive solutions has entered the phase of increasing ADAS penetration, especially closing to L0-L2+ of automated driving. It is one of the fastest growing automotive application fields that the Company has accelerated mass production in recent years. ADAS features that used to be available only on some high-end models, such as adaptive cruise, automatic braking, and lane departure warning, have been delegated to more and more low-grade models, which will bring a huge incremental market to the 360 surround view system, the dual front view system, the DMS (driver monitoring system), and other ADAS products that the Company has mass-manufactured. At present, the customers for whom the Company has mass-produced mainly include Geely, FAW, and Dongfeng. The Company has signed in-depth cooperation agreements with several software and hardware enterprises (Nanfang Black Sesame Group Co. Ltd., Leadmove, Chuhang Tech, and Metoak) to bring more breakthroughs in products.

4) Lightweight is one of the important directions of automobile development. Compared with traditional stamping and welding products, the weight of hydroformed structural parts is reduced by 20%-30%, which can effectively reduce the weight of the body and achieve automobile light weight. The Company has independently developed a 3,000-ton double-station and double-supercharged internal high-pressure forming machine and a 5,000-ton internal high-pressure molding machine. Its customers have covered tier 1 suppliers such as Gestamp, Shanghai Huizhong (Cadillac), and Pos-Austem (Volvo), as well as independent brands such as Great Wall, Dongfeng Liuqi, and BYD. In 2021, the Company reported a revenue of approximately RMB80,000 thousand in lightweight structural parts, a year-on-year increase of approximately 30%. With the growth of automotive lightweight demand, the Company is expected to accelerate the sales volume of lightweight products in the next few years.

Investment Thesis & Valuation

In 2022Q1/Q2, the Company saw a year-on-year decline of 40%/60% in net profit, mainly due to 1) the impact of local political conflicts on the European business, 2) the suspension of production due to the pandemic, 3) the rising sea freight of raw materials, 4) the share incentive expenses, and 5) exchange losses arising from the appreciation of the RMB. We expect the headwinds to dissipate as the automotive industry gradually recovers from the pandemic. In the medium and long term, the Company's traditional business is expected to maintain stable growth, and the emerging business is expected to enter a period of rapid growth with the promotion of intelligence.As analyzed above, we expected diluted EPS of the Company to RMB 1.26/1.88/2.44 of 2022/2023/2024. And we accordingly gave the target price to 57.6, respectively 30.7x P/E for 2023. "Accumulate" rating. (Closing price as at 2 September)

Financials

Click Here for PDF format...