Company Profile

Techtronic Industries (`TTI`) founded in 1985 and is a world leader in Power Tools, Accessories, Hand Tools, Outdoor Power Equipment, and Floorcare and Cleaning for Do-It-Yourself (DIY), professional and industrial users in the home improvement, repair, maintenance, construction and infrastructure industries, with brands like MILWAUKEE, RYOBI and HOOVER etc. MILWAUKEE is the number one and fastest-growing global brand in the professional tool market. MILWAUKEE professional cordless outdoor equipment, which is now the fastest-growing brand of cordless professional-grade outdoor products for landscapers and lawn and garden enthusiasts. RYOBI is the number one DIY tool and cordless outdoor power equipment brand worldwide.

The Power Equipment Division includes industrial power tools, accessories, hand tools, storage, layout and measuring tools, outdoor products, and professional, consumer, and trade power tools. The vast array of products in this division provide a complete line of products for household, construction and infrastructure projects.

The Floorcare and Cleaning Division includes upright vacuums, canisters, bagged and bagless vacuums, stick vacuums, broom vacuums, and a complete line of carpet and floor cleaners. Each product line contains specific designs for both home and commercial use.

In addition to developing one runaway successful product after another, the network effect of TTI interchangeable battery systems. For example, the flagship MILWAUKEE M18 platform now has 251 products that run off the same M18 battery and is rapidly growing. This is attractive to new customers who gain access to a wide range of tools that run off the same powerful battery. It also creates a loyal customer base with access to a continuous stream of new products available as bare tools powered by batteries they already own.

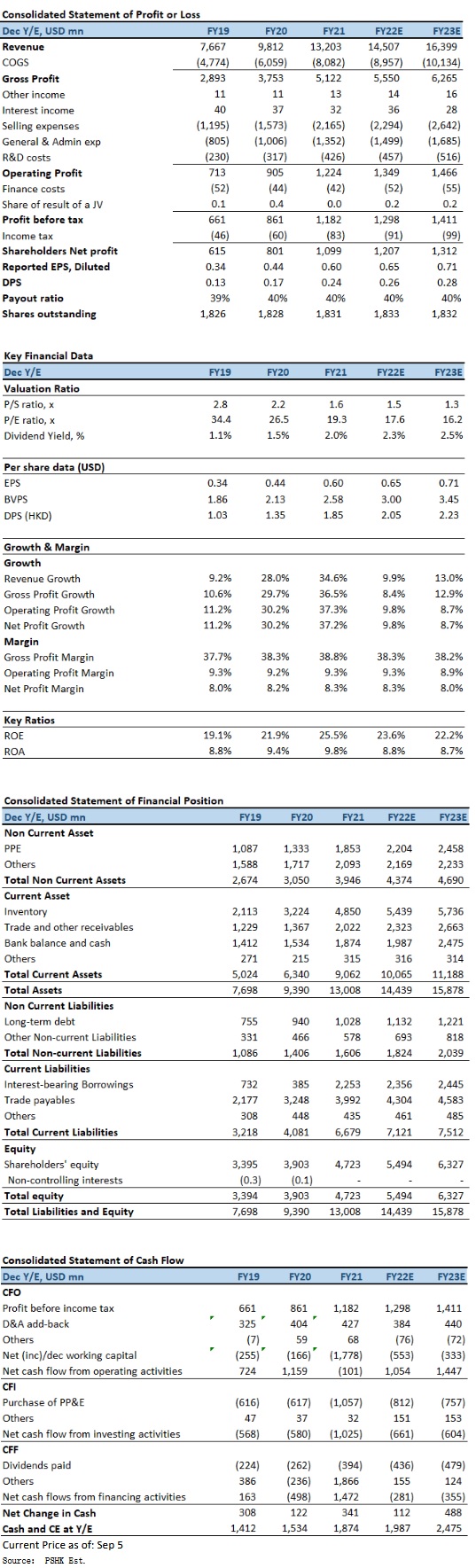

Gross margin increased 50bps, result of new product introduction

For the 1H2022, TTI reported revenue for the period grew by 10.0% YoY, amounting to US$7,034mn. EBIT amounted to US$633mn, an increase of 10.7% as compared to the US$572mn reported in the same period last year. Profit attributable to Owners of the Company amounted to US$578mn as compared to US$524mn reported in the same period last year, an increase of 10.4%. Basic earnings per share was at US31.59 cents (2021: US28.62 cents), an increase of 10.4% YoY. Interim dividend per share approx. US12.23 cents, an increase of 11.8% YoY.

Gross margin increased 50bps to 39.1% as compared to 38.6% reported in the same period last year. The margin improvement was the result of new product introduction, product mix, category expansion, improvements in operational efficiency and supply chain productivity together with very effective action plans to navigate global supply constraints, commodity headwinds and logistic costs increase.By business segment, Power Equipment segment delivered sales growth of 14.9% YoY in local currency to US$6.6bn. Flagship MILWAUKEE business continued to flourish with 25.8% local currency sales growth YoY. DIY (Do-it-Yourself) /Consumer Power Equipment business grew low single digits in local currency, while the RYOBI Outdoor business outperformed the overall market despite being impacted by unfavorable weather conditions. Floorcare and Cleaning business was impacted by a reduction of COVID-related demand, leading to a decline in sales of 17.8% YoY to US$472mn in 1H2022.

All geographic regions delivered solid sales growth in the first half. Rest of World featuring Australia and Asia delivered outstanding 23.0% YoY growth in local currency. Europe grew 14.1% YoY in local currency and North America grew 10.5% YoY in local currency.

Investment Thesis

For 2022FY revenue guidance, management is expecting revenue growth at mid-single digits. While there is doubtful of the outlook for the U.S. economy, especially as the U.S. housing market continues slow down. However, Home Depot, one of TTI's customers, beat its 2Q2022 results, citing consumers spending more time in their homes and continued structural support for demand for home improvement projects, and reaffirming its guidance of approximately 3% revenue growth in 2022. Therefore, we expect TTI to at least meet its revenue guidance, or even slightly beat in 2H2022. We expect FY2022-FY2023 EPS to be USD0.26 and USD0.28 respectively, with PT of HKD112.4, implies a FY2022E P/E of 21.9x (~5-yrs historical average). Our investment rating is “Buy”.

Risk factors

1) Resurgence of COVID in Mainland China; 2) The pace of product innovation is lower than expected; 3) Hikes in commodity prices; and 4) Industry competition is greater than expected.

Financial

Click Here for PDF format...