Investment Summary

Company Profile

Sanhua is the world's largest manufacturer of HVACR controls and components, focusing on heat management business with heat pump technology as the core. It operates the domestic and commercial air conditioning business as well as automotive heat management fields, establishing a leading position in the industry. The products of the Company such as electronic expansion valves of air conditioning, four-way reversing valves, solenoid valves, micro-channel heat exchangers, automotive electronic expansion valves, new energy vehicle heat management integrated components and omega pumps have the highest market share across the world. The market proportion of service valves, thermostatic expansion valves for vehicles and receivers rank top among the world.

The Company Earns 20% More in H1

According to its 2022 interim report released, in H1, Sanhua Intelligent Controls reported a revenue of RMB10.16 billion, a year-on-year increase of 32.4%, and a net profit attributable to the parent company of RMB1 billion, a year-on-year increase of 21.8%. Specifically, in Q1 and Q2, the Company reported a revenue of RMB480,4 million and RMB535,6 million, a year-on-year increase of 40.94% and 25.56%, respectively, and a net profit attributable to the parent company of RMB453 million and RMB550 million, a year-on-year increase of 25.81% and 18.63%, respectively. Compared with Q1, there was a decline in the year-on-year growth of revenue and profit in Q2, mainly due to the negative impact of the pandemic. However, the Company still reported a sound growth on a yearly and quarterly basis, showing strong resilience.

The Auto Parts Segment Sees High Growth

In terms of segmented business, the traditional refrigeration segment recorded a revenue of RMB6.96 billion in H1, accounting for 68.5% of the total revenue, an increase of 25% year-on-year, significantly better than the downstream industry. According to industry data, China saw a year-on-year decline of 4.1% and 10.4%, respectively in the cumulative production volume of air conditioners and refrigerators in H1. The main reason is due to changes in the industry pattern and the increase in orders generated by relatively high prosperity of overseas markets. In view of the continued high temperatures across the world, the demand is expected to remain strong in H2.

The Company reported a revenue of RMB3.2 billion from the auto parts segment in H1, a significant increase of 52% year-on-year, and its proportion in the total revenue increased by 4 ppts to 31.5%. This was mainly due to the improvement in prosperity of the downstream new energy vehicle market, which drove the Company's business growth. In H1, 2,600 thousand new energy vehicles were sold in China, surged by 120% year-on-year. The Company's new energy auto parts business has accounted for 87% of the auto parts segment, enlarged by 12 ppts over the same period last year. With the continuous resumption of work and production in the automobile industry after the pandemic, and the national policy support, it is expected that the enthusiasm of the new energy vehicle market will continue. The Company has sufficient orders on hand, and closely cooperates with car companies. With the release of subsequent production capacity in factories in Mexico and Binhai, the future revenue is expected to continue to grow faster.

With Rise and Fall of Gross Margin, There Is Room for Improvement in the Future

The overall gross margin during the reporting period was 24.2%, a year-on-year decrease of 1 ppt. The main reason we estimate is that transportation expenses were adjusted to operating costs due to changes in accounting standards. After the restored adjustment of accounting standards due to the transportation expenses, the Company's gross margin in Q1 and Q2 of 2022 actually decreased by 1.8 ppts year-on-year, basically remaining unchanged at approximately 23.3% and 25%, respectively.

In terms of segments, the gross margin of the traditional refrigeration segment was 23.7%, a year-on-year decrease of 1.99 ppts, mainly due to 1) the faster growth of low-priced products as a result of the product structure decline; 2) the significant rise in sea freights and raw material prices compared with the same period last year; 3) the exchange rate. The gross margin of the auto parts segment was 25.4%, a year-on-year increase of 1.4 ppts, mainly benefiting from 1) the increased proportion of self-made products among the integrated components; 2) the gradually appearance of scale effect; and 3) the gradual reflection of the agreement in which customers jointly share the increase in prices of raw materials such as aluminum and freights.

The overall net interest rate in H1 reached 9.87%, a year-on-year decrease of 0.86 ppts. In addition to the gross margin, there were also some hedging and forward contract losses, which offset the exchange gains.

Since H2, raw material prices and sea freights have fallen more than the prior highs, and driven by the improvement of the linkage mechanism of raw material prices, the exchange depreciation and the profitability of the auto parts segment, the overall profitability growth is expected to resume.

Investment Thesis

Sanhua is the leading company of refrigeration parts and components with obvious technical advantages in its products. The thermal management of new energy vehicles, dishwashers and cold-chain logistics are all promising business areas in line with the general direction of social development in the future. We expect that the Company's home appliance business will benefit from the market share increase year by year. There is a broad market for the thermal management of new energy vehicles in the future.

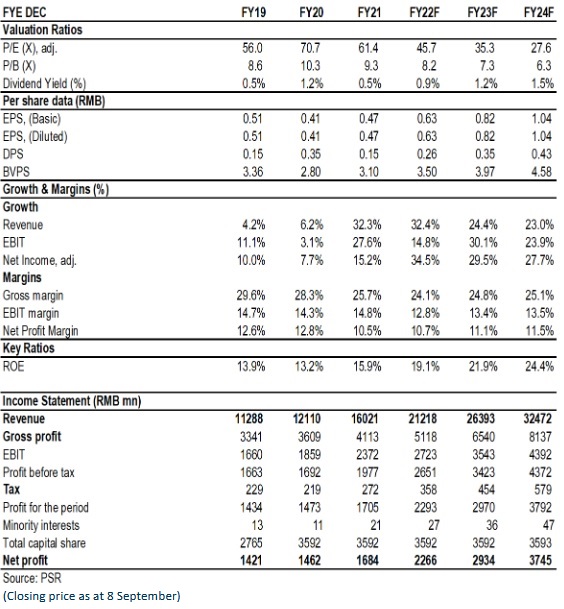

As for valuation, taking into account the negative impact of the increase in raw material prices/ocean freight, we adjusted the company's 2022/2023 earnings per share to 0.63/0.82 yuan (previously 0.70/0.85 yuan), and introduced a 2024 earnings per share forecast ( 1.04 yuan), a year-on-year increase of 35%/29%/28%,. And we accordingly gave the target price to RMB33.5, respectively 53/41/32x P/E for 2022/2023/2024. "Accumulate" rating. (Closing price as at 8 September)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

Click Here for PDF format...