Investment Summary

Company profile:

Tuopu Group is an industry leader in the field of automotive NVH that is capable of synchronous design with the original equipment manufacturer. In recent years, on the basis of the original business of shock absorbers and interior functional parts, the Company has proactively arranged the module of the lightweight chassis system and the automotive electronics business as the future Ŗ+3" strategic development projects, in order to adapt to the trend of electrification, intellectualization and lightweight of vehicles.

Continuing a High Growth amid the Pandemic, the Results Are Expected to Increase by 45%-60% in H1

Tuopu Group recently disclosed good news about the results. It is expected that the revenue will reach RMB6.54-6.9 billion in H1 of 2022, up 33-40% yoy; the net profit attributable to the parent company will be RMB667-737 million, up 45-60% yoy. In the first quarter of 2022, the Company recorded RMB3.75 billion of revenue and RMB390 million of net profit attributable to the parent company. Base on this, the Company reported a revenue of RMB2.8-3.2 billion in the second quarter, up from 12% to 27% yoy, and down from 25% to 16% qoq; the net profit attributable to the parent company was RMB280-350 million, up from 32% to 64% yoy, and down from 27% to 9% qoq. Considering the impact of the pandemic on Tesla's Shanghai factory in the second quarter, the figures declined qoq. However, the profitability still remained stable, reflecting the Company's rapid market expansion and order growth relying on the forward-looking layout of new energy vehicles and platform advantages, and hedging against the impact of unfavorable factors such as the pandemic and rising raw material prices. The results continued to grow at a high rate.

Meanwhile, the Company is also continuing to actively seize the opportunity of improving the electrified and intelligent automobiles. It has developed new projects with higher value of single vehicle, including the air suspension system factory, integrated die-cast rear cabin of 7200T, heat pump products, and intelligent electronics related products, which are expected to achieve new breakthroughs in customers and orders in the coming one or two years.

The Company Deeply Binds Tesla and Actively Expands the Customer Base

In terms of major customers, Tesla delivered approximately 260 thousand units in the second quarter, including 150 thousand units in overseas markets, up 51% yoy and up 13% qoq, and 110 thousand units in the Chinese market, up 8% yoy and down 37% qoq. With the resumption of work and production, the production capacity of Tesla's Shanghai factory will benefit from the transformation of the production line in H2. It is expected that Tesla's contribution to the revenue throughout the year will increase from 47% in 2021 to 50%. Both parties have maintained a deep cooperative relationship. In addition to Tesla, GM, Geely, Ford, and FCA, the Company has also expanded customer base to new car-making forces, North American new energy vehicle companies (Rivian and Lucid), as well as Huawei, Jinkang, and Xiaomi, which will continue to promote high growth in orders.

The Company Issues RMB2.5 Billion of Convertible Bonds to Accelerate the Layout of Electrified and Intelligent Automobiles

On July 11, the Company announced that it intends to publicly issue RMB2.5 billion of convertible bonds, mainly for the construction project of lightweight chassis system. The total investment of the project is expected to be RMB2.66 billion. After full capacity, the Company is expected to achieve an annual production capacity of 4,800 thousand sets of lightweight chassis system, including 1,600 thousand sets of subframes, 1,600 thousand sets of suspension system, and 1,600 thousand sets of steering knuckles. In 2021, the Company's production capacity of lightweight chassis system was approximately 2,800 thousand sets, with a capacity utilization rate of approximately 102.24%. The product was in short supply. The Company launched the project of lightweight suspension system after 2003, and has currently mastered the forming processes of high-strength steel and six major light alloys related to the lightweight chassis system module. Through the construction of this convertible bond project, the Company can further enhance its global supply capacity, consolidate its market position, and fully benefit from the trend of electrified and intelligent automobiles.

Investment Thesis

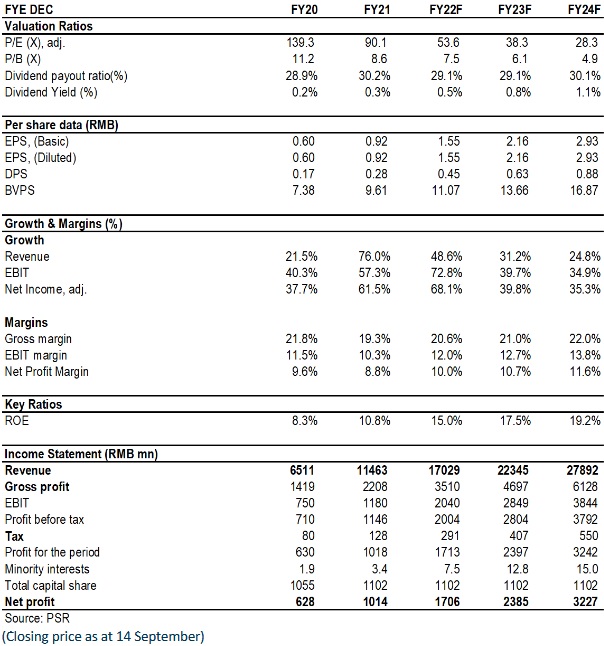

As raw material prices have fallen since July, we expect the Company's gross margin to pick up in the second half of the year. As the leader of the new energy auto parts industry, the Company accelerates the expansion of customer base, and optimizes the R&D and design of products, while continuously expanding new categories. The Company is expected to continue to gain market share..In terms of valuation, we expect the EPS to be 1.55/2.16/2.93 yuan in 2022/2023/2024. We are optimistic about the development prospects of the company's lightweight business and automotive electronics. So, we lift the Company's target price to RMB 97.5 yuan, respectively 63/45/33 x P/E for 2022/2023/2024, a "Accumulate" rating. (Closing price as at 14 September)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...