Investment Summary

Company Profile

Minth Group is a world-renowned supplier engaged in the design, manufacturing and sales of automotive interior and exterior trim and body structure parts. The domestic market share of its core products exceeds 30%. The company has production bases in China, the United States, Mexico, Thailand, Germany, Serbia and other countries, and its customers cover major vehicle companies in the market. Based on a variety of new materials and surface treatment technologies, in recent years the company has developed new electrified and smart product lines such as aluminum power battery boxes and smart front faces, forming a series of competitive terminal products.

Due to Multiple Factors, H1 Results Drop by 4.5% Yoy But Improve Hoh

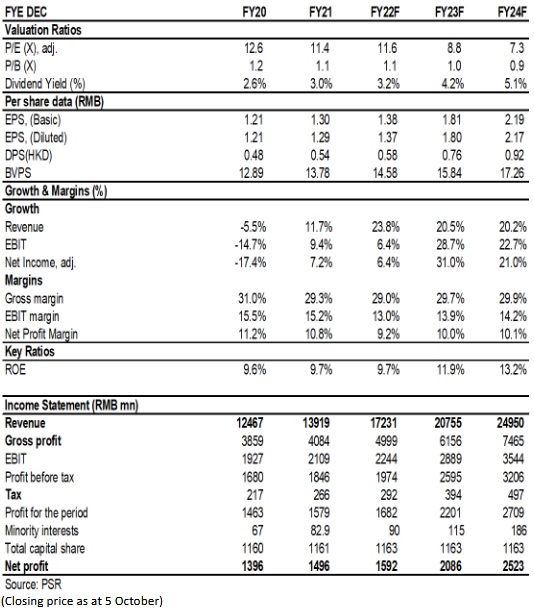

In H1 of 2022, the global auto market was affected by the chip shortage, the Russia-Ukraine war and the pandemic. However, with the mass production of the Company's battery housing business and the rapid growth of overseas business, Minth Group's turnover increased by 8.9% yoy to RMB7.25 billion; the net profit attributable to shareholders was RMB660 million, down 27.0% yoy. Excluding the one-time gain from the disposal of a subsidiary in H1 of 2021, the net profit actually fell by 4.5% yoy. The year-on-year decline in results was mainly due to higher selling expenses resulting from the rising raw material costs and sea freights, as well as higher R&D expenses arising from the Company's continuous promotion of new products such as battery housings. However, compared with H2 of 2021, the results rose by approximately 10% hoh.

On a closer look at markets, the domestic market revenue grew by 2.8% yoy to RMB3.89 billion, falling short of expectations. This was mainly affected by the pandemic in Q2; while the overseas market presented brilliant performance. Its revenue soared by 16.9% yoy to RMB3.36 billion, and its proportion in the gross revenue rose by 3.2 ppts to 46.3%. The Company's factory in Serbia continued to climb. The Company is accelerating the layout in Poland and the United States for further advancement.

Gross Margin Is under Pressure, and Expense Ratio Is Basically Stable

During the reporting period, the overall gross margin was 29.1%, down approximately 2.8 ppts from 31.9% in the same period. It mainly suffered pressure from the depreciation of old products and the high volatility of raw material prices. In the meanwhile, the overall gross margin was dragged down by the increased proportion of turnover of some overseas factories in the climbing period. In H1, the total selling, administration and R&D expense ratio grew by 0.4 ppts yoy to 20.8%. Specifically, the selling expense ratio increased by 1.1 ppts yoy, reflecting the rising sea freights, and the administration expense ratio decreased by 1.2 ppts yoy, reflecting the improvement of operating efficiency and the reduction of options tariff.

Battery Housing Business Is Going through an Explosive Period, and New Orders Hit a New High

In H1, the Company's four major products, namely metal and trim products, plastic products, aluminum products and battery housings, reported revenue of RMB2,548 million, RMB2,095 million, RMB1,740 million and RMB498 million, respectively, up 8.24% and 6.97%, down 0.2% and up 435.0% yoy, respectively. The battery housing business has entered an accelerated explosive period, with a growth rate of 374 ppts higher than the same period last year. The segment margin of battery housings rose from 5.8% to 18.0%. Although it is still below the overall gross margin of approximately 30%, we think that as production capacity continues to explode, the gross margin, benefiting from the scale effect, is expected to increase to 23% in 2023.

In H1, the Company's new orders reached a new high. With an annualized turnover of RMB9.3 billion, the annual turnover is expected to reach RMB12 billion. At present, the orders in hand witness a net increase of RMB30 billion from the end of last year, reaching RMB180 billion. Specifically, battery housings, plastic products, aluminum products, and metal and trim products account for 38%, 22%, 22% and 17%, respectively. Looking ahead, in anticipation of continued strong growth in the battery housing business, the Company's management has given guidance on the growth rate of revenue and profit of more than 30% in H2.

Valuation

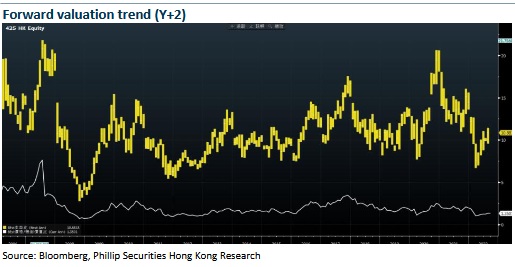

We revised the forecast of EPS of 2022/2023/2024 to be RMB 1.38/1.81/2.19 yuan. And we believe that it is reasonable to give the company a valuation of 19.7/15/12.4x P/E and 1.9/1.7/1.6x P/B for 2022/2023/2024, equivalent to target price of HK$ 31 and BUY rating. (Closing price as at 5 October)

Financials

Click Here for PDF format...