Company Profile

The Prada Group (1913) is a leading business in the luxury goods industry, where it operates with the Prada, Miu Miu, Church's and Car Shoe brands producing and distributing leather goods, footwear and apparel. It also operates in the food industry with Marchesi 1824, in the most prestigious sailing races with Luna Rossa and in the eyewear and fragrance industries under licensing agreements.

The Prada owns 23 manufacturing plants (20 in Italy, 1 in the United Kingdom, 1 in France and 1 in Romania) and its products are sold in 70 countries worldwide, primarily through directly operated stores. The Prada Group's products are also sold directly through the brands` e-commerce activity and indirectly by selected prestigious department stores, independent retailers in very exclusive locations, and important e-tailers.

1H2022 net revenues up by 22.5% at constant exchange rates

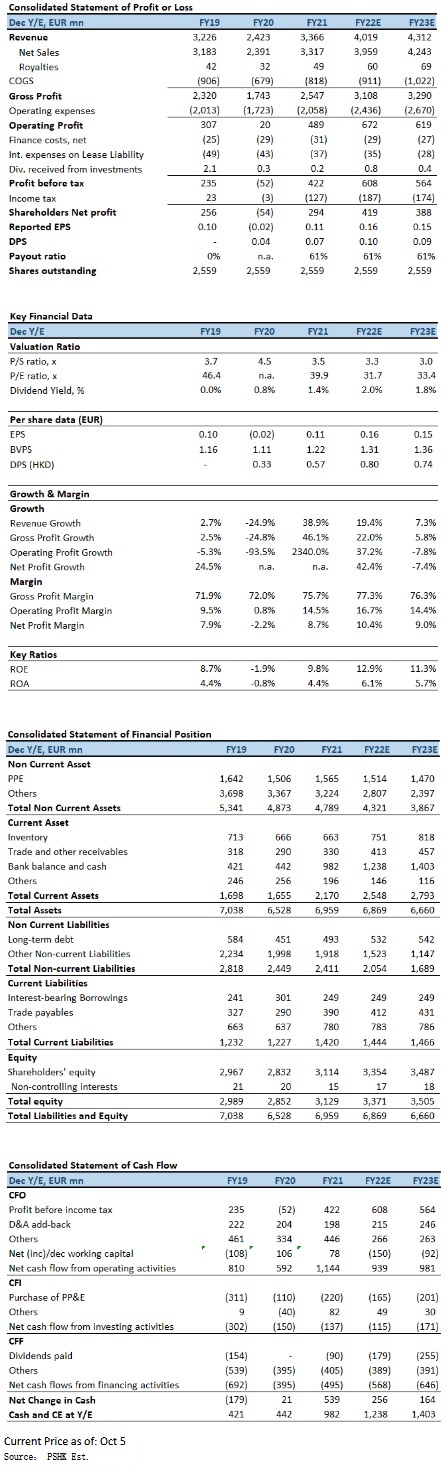

For the 1H2022, Prada Group generated net revenues of EUR1,900.9mn, up by 22.5% at constant exchange rates from those of the 1H2021 and by 22.2% from 1H2019, exceeded pre-pandemic levels. At current exchange rates, the 2021 performance was boosted by 26.6% growth. The recurring operating result for the period, or EBIT Adjusted, was EUR331mn, whereas in increased by 99.4% compared to 1H2021 (EUR165.9mn). The EBIT Adjusted was also considerably higher than 119.8% that of the 1H2019 (EUR150.5mn). Profit attributable to shareholders was EUR188.3mn, an increase of 93.6% YoY. Basic EPS were EUR0.074 (1H2021: EUR0.038), an increase of 94.7%.

By distribution channels segment, sales of the retail channel had double-digit growth of 26.4% (at constant exchange rates) against the same period of 2021; the increase was 37.7% versus the same period of 2019. Direct e-commerce sales (included in the above results) in the first half rose by 29.1% versus the same period of 2021 and accounted for approximately 7% of total retail sales, which is in line with the annual 2021 data. There were 627 stores at June 30, 2022, following 7 openings and 15 closures in the period, 9 of which related to the Church's brand.

In Asia Pacific, the retail sales of the six months ended June 30, 2022 decreased by 6.7% at constant exchange rates from those of the same period of 2021, due to the decline in China ensuing from the restrictions imposed by the authorities following Covid-19 outbreaks. The situation improved in June 2022 when the restrictions were relaxed, and the decline was offset by double-digit growth in all the other countries in the region (Korea and Southeast Asia in particular). Compared with the 1H2019, Asian Pacific sales increased by 26.1%.

Retail sales in Europe, driven by domestic consumption and the tourism recovery in the second quarter of the period, showed an upsurge of 88.7% at constant exchange rates against 1H2021, and of 34.4% against 1H2019. The retail sales of the American market rose by 41.1% at constant exchange rates from those of 2021, staying on the positive trend of double-digit growth underway in 2021. Compared with 1H2019, the sales had triple-digit growth. All the countries in the region reported sales gains. The retail sales of the Japanese market rose by 28.2% at constant exchange rates compared 1H2021, which was still suffering from persisting restrictions; the growth accelerated further in the second quarter. Set against 1H2019, the Japanese market showed a slight decline of 2.9%. At constant exchange rates, retail sales in the Middle East were 24% higher than 1H2021 and 59.4% above 1H2019, continuing on 2021's growth trend there as well.

By products segment, retail growth across all product categories. Sales of RTW rose by 32.1% YoY, and footwear sales, up by 38.5%. Sales of leather goods rose by 18.1% YoY. The increases compared with 2019 were: 64.8% for RTW, 46.3% for footwear and 23.9% for leather goods.

By brands segment, Prada brand retail net sales were 28.1% (at constant exchange rates) higher than in the first six months of 2021 and 45.5% (at constant exchange rates) above 1H2019. Miu Miu's sales increased by 13.6% (at constant exchange rates) from 1H2021 and by 5.3% (at constant exchange rates) from that of 1H2019. Miu Miu finds itself in a relaunch phase. Church's, the brand most affected by the geographical exposure to Europe, reported a gain of 28.7% (at constant exchange rates) on the 2021 sales. Royalty income, supported by the growth in the eyewear segment, rose by 22.2% YoY.

For the 1H2022, the gross margin corresponded to 77.7% of the net revenues, up substantially 340bps from the 74.3% of 2021. Despite cost inflation, for example in logistics costs, a higher average price, greater absorption of production overheads, a better sales mix in terms of distribution channels and a favorable exchange rate were behind the improvement of operation result. The increase is even more significant when comparing the 2022 margin with that of the 71.7% in 1H2019.

Investment Thesis

For 2H2022, management would benefit from further operating leverage and also remains optimistic on the underlying demand of the Chinese market. However, we believe that some concerns around the macro outlook remain, resulting in continued volatility in coming results. We expect the company's EPS forecast for FY2022-FY2023 to be 0.16 EUR and 0.15 EUR (mainly because we are concerned about the risk of global economic regression, significant exchange rate fluctuations and continued high inflation that will have a more negative impact on the company's operations in 2023), with PT of HK$54.40 (if we use the fairly low EUR/HKD exchange rate of $7.5 to $7.6 for the recent month, the corresponding target price would be HK$52.4 to HK$53.1), implies a FY2022E P/E of 42.6x (~5-yrs historical average). Our investment rating is “Buy”.

Risk factors

1) Resurgence of COVID in Mainland China; 2) Sharp fluctuations in foreign exchange rate; 3) Brand transformation is not as expected; and 4) Global economy contracted more than expected.

Financial

Click Here for PDF format...