Investment Summary

FY2022H1 Was Severely Hit by the Pandemic

In H1 of 2022, the business of Shanghai Airlines suffered a huge shock because Shanghai implemented continuous static management from late March to combat the pandemic. Specifically, the revenue during the reporting period decreased by 35.4% Y-o-Y to RMB1,166 million, resulting in a net loss attributable to the parent company of RMB1.26 billion and expanding the loss by RMB520 million compared with the loss of RMB740 million in the same period last year. The main reason for the loss was that the normal operation of the airline industry was hampered by the pandemic, the revenue dropped sharply while the cost was relatively fixed, and the vacancy rate of production capacity was high, which severely suppressed profitability. The impact of the pandemic was particularly significant in Q2, when the net loss was as high as RMB748 million, and Q1 recorded a net loss of RMB510 million.

Both Aeronautical and Non-aeronautical Revenue Decreased Dramatically

The Company's business volume declined sharply in H1 under the impact of the pandemic. Specifically, there were 92.4 thousand aircraft movements in total, down by 51.37% Y-o-Y. The passenger throughput was 5,742.9 thousand, down by 68.53% Y-o-Y. The cargo and mail throughput was1,472.1thousand tons, down by 30.66% Y-o-Y. The domestic passenger throughput was close to zero (-99%) in Q2 during the static period. The decrease in the number of flights and the passenger throughput led to a substantial drop of 41% Y-o-Y in the Company's revenue from the aeronautical business in H1 to RMB574 million, down by 72% compared with the same period in 2019. The separate revenue from aircraft movements and from the passenger, cargo and mail throughput decreased by 26% and 63%, down by 52% and 87%, respectively compared with the same period in 2019.

Because of the decrease in the number of passengers, the Company's non-aeronautical revenue also decreased dramatically by 28.6% to RMB592 million. Specifically, the revenue from commercial catering and other non-aeronautical revenue dropped by 47% and 17% Y-o-Y, respectively, down by 94% and 35%, respectively compared with the same period in 2019. The rental from duty-free shops recorded RMB139 million in H1, down by approximately RMB80 million YoY. The rental from duty-free shops in Q1 and Q2 was RMB117 million and RMB22 million, respectively, and the duty-free business in Q2 was under pressure.

With Relatively Fixed Costs, Multiple Measures Were Taken to Relieve Pressure

The Company's pressure at the cost end was partially relieved because of the measures taken by the Company, such as extending the depreciable life of fixed assets (including terminal buildings, runways and aprons) to reduce the depreciation rate of fixed assets Y-o-Y, as well as support policies such as rent reduction and exemption from the controlling shareholder. However, due to fixed costs, the operating cost during the current period decreased by 9.6% to RMB2,684 million, still less than the decline in revenue. Additionally, the affiliated companies and joint ventures in which the Company has a stake also performed poorly in terms of operating efficiency due to the pandemic, resulting in a Y-o-Y decrease of 91.8% in investment income to RMB35 million. Other income increased by RMB163 million Y-o-Y mainly as a result of the receipt of special support funds for the pandemic during the current period.

Investment Thesis

According to the latest operating data, the Company's business volume rebounded rapidly after the pandemic. The passenger throughput of Pudong Airport fell by 76% Y-o-Y in July and rebounded by 26.2% Y-o-Y in August, a growth rate of 439% and 88% M-o-M, respectively, which indicated that the Company's strengths in location and competitiveness did not undergo essential change amid the pandemic. Recently, favorable policies for international routes have been released continuously, including relaxing restrictions on flight suspension, optimizing isolation policies, resuming the entry approval of some foreigners and increasing the number of international flights. With the expectation that international flights will continue to resume, the value of the duty-free business will return, and the Company's performance and valuation will be restored. Furthermore, after the completion of the issuance of additional shares and the overall listing of Hongqiao Airport and other assets at the end of July, the linkage between Hongqiao Airport and Pudong Airport will be strengthened, and the operating efficiency will be enhanced.

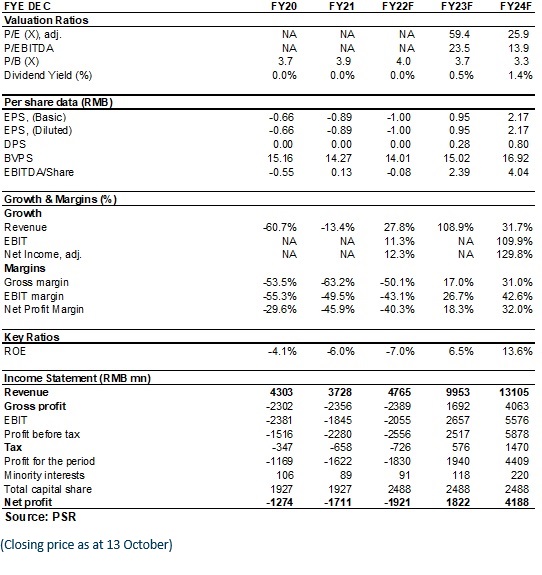

Considering the pandemic impact, we revised the EBITDA predicted value of SIA in 2022/2023/2024 to -0.08/2.39/4.04 yuan, and revised the target price to RMB 64.5 (formerly RMB 62.3), and the "Accumulate" rating is given. (Closing price as at 13 October)

Financials

Click Here for PDF format...