A Brief introduction to the company

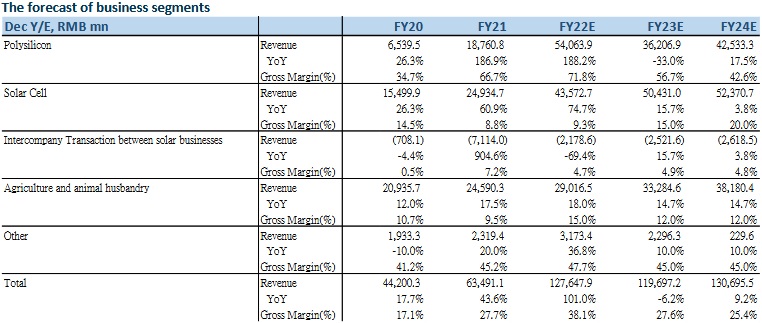

Tongwei(600438.SH) is a leader in the production of polysilicon and photovoltaic cells. Founded in 1982, the company has been operating agriculture and animal husbandry businesses. In 2006, the company acquired Sichuan YongXiang(永祥股份), penetrating polysilicon, PV cells, and PV power plants businesses. At present, the company's main business includes polysilicon, PV cells, and agriculture and animal husbandry businesses, accounting for 24%, 32%, and 32% of total revenue.

A review of 2022 H1 Results

On October 9, the company released a performance forecast. The net profit attributable to shareholders in the first three quarters of 2022 is expected to be 21.4-21.8 billion yuan (the same below), up 260.0%-266.7% YoY; the Q3 net profit attributable to shareholders is expected to be 9.18-9.58 billion yuan, up 208.0%-221.5% YoY and 30.5-36.2% QoQ, far exceeding Bloomberg's consensus expectation of 5.94 billion yuan. The net profit attributable to shareholders after deducting non-recurring gains and losses in the first three quarters is expected to be 21.6-22 billion yuan, 264.2-271.0% YoY; the Q3 net profit attributable to shareholders after deducting non-recurring gains and losses in Q3 is expected to be 9.11-9.51 billion yuan, a year-on-year increase of 210.2%-223.8% and 23.8%-29.2% QoQ, far exceeding Bloomberg's consensus expectation of 5.94 billion yuan.

The company explained that the reason for the sharp increase in profit is that the demand for polysilicon products continued to be strong, and the price rose YoY. In addition, the company's new production capacity quickly ramped up, resulting in a substantial increase in volume and profit. The outputs and sales of the PV cells boomed significantly, and the product mix continued to be optimized, resulting in an increase in profitability. There has been optimization of market strategy in the agriculture and animal husbandry businesses, resulting in sales and profit growth. However, with our calculation and understanding of the production capacity of the polysilicon industry, we believe that the main reason for the company's higher-than-expected profit is that the company's capacity utilization rate exceeds 110%, making the output of Q3 polysilicon much higher than the design capacity.

The company expands its polysilicon production capacity rapidly; the output of polysilicon is expected to rise

The company has been significantly expanding its polysilicon production capacity. We expect the company's polysilicon production capacity to increase from 180,000 tons in 2021 to 230,000/350,000/750,000 tons at the end of 22/23/24. In 2022, the BaoTou Phase II 50,000-ton silicon production line was put into operation in June. We expect the LeShan Phase III 120,000-ton silicon production line will be put into operation in the second half of 2023. Subsequently, the BaoTou Phase III and BaoShan Phase II 200,000 production lines will be put into operation in early 2024. According to the company's long-term production capacity plan released on April 25, the company expects the polysilicon production capacity to reach 800,000-1,000,000 tons in 2024-2026. Due to the company's plan to significantly expand its production capacity, we expect the company's polysilicon output to increase significantly from 107,000 tons in 2021 to 234,000/280,000/480,000 tons in 22/23/24.

The electricity cost dropped significantly; the cost advantage of polysilicon is obvious

Aside from silicon metal, the main cost of polysilicon comes from electricity consumption. In 2021, 29% of the company's polysilicon cost come from electricity, second only to silicon metal, which accounts for nearly 50% of the cost. Since the room for reducing the amount of silicon metal in the production of polysilicon is very limited, the ability to control electricity costs is the core competitiveness of polysilicon companies. The company's electricity cost control comes from two aspects: electricity price advantage and electricity consumption reduction. In terms of electricity price advantage, the company established polysilicon production lines in Sichuan, Yunnan, Inner Mongolia, and other low electricity price areas, and signed a lower electricity price agreement with local governments. The cost of electricity was between 0.25 and 0.3 Yuan/kWh level. In terms of electricity consumption reduction, the company announced in April this year that the company's power consumption for producing one kilogram of polysilicon is 50kWh/kg, down 12% YoY, exceeding the market expectation and much lower than the average power consumption level of 63kWh/kg. Originally, some market participants expected that it was difficult for the power consumption of the modified Siemens method to drop below 50 kWh/kg-Si. We believe that the company will use a large-scale polysilicon reduction furnace to reduce the power consumption level to below 50 kWh/kg-Si, and as a result, the company's gross profit margin could be much higher than its peers due to the company's advantages.

Lv Jinbiao, deputy director of the expert committee of the Silicon Industry Branch, said that with the doubling of production capacity in the coming two years, the polysilicon production capacity will reach 2.74 million tons in 2023, and excess supply of polysilicon is inevitable. We expect that the price of silicon material (including tax) will gradually drop from the current 30 yuan/kg-Si to the production cost of the old polysilicon factory, which is about 10 yuan/kg-Si. Despite the drop, we expect the company's polysilicon gross profit margin to remain above 30% by then.

With its polysilicon purity technology leading the industry, the company benefits from the transition from p-type PV tech to N-type PV tech

With the PV industry experiencing a transition from P-type PV technology to a more photoelectrically efficient N-type PV technology, the market share of N-type PV technology will be increasing significantly. N-type silicon wafers require that the minority carrier lifetime in the silicon wafers is greater than 1000 microseconds, so the N-type silicon wafers require that the purity of the polysilicon be at least the second grade of electronic-grade polysilicon. The purity of the company's polysilicon leads the industry. The company announced that the company could increase the proportion of N-type polysilicon up to 80% of total polysilicon produced, which is higher than Daquan Energy's 30%-40%. Besides, the quality of GCL tech's FBR-based granular silicon is far worse than that of the second grade of electronic-grade polysilicon. We believe that with the development of the N-type photovoltaic cell, the company's polysilicon purity advantage will allow the company to maintain its market share.

The company rapidly increases PV cells production capacity; the capacity utilization is expected to remain high

The company's PV cell production capacity will be greatly improved. At present, the current capacity is around 54GW, and we expect the capacity will be around 70GW by the end of the year. The company announced in April this year that the planned cell production capacity in 2024-26 will be 130-150GW, which is about twice the current production capacity. In addition, the company's self-supplied polysilicon is used as the raw material for the PV cell, which keeps the capacity utilization rate of the company's PV cell production line at a high level. The cell capacity utilization rate in 2021 was 99.47%, which is much higher than the global average capacity utilization rate of 40-60% (according to Heraeus Photovoltaics), allowing the company to keep the proportion of depreciation costs at a low level. We believe that due to the continuous high utilization rate of cell production capacity, the rapid growth of PV cell production capacity will effectively drive the company's PV cell output to grow simultaneously.

Investment in a 25GW module production line to build a vertically integrated business

On September 22, the company announced that it will invest 4 billion yuan to build a 25GW high-efficiency PV module production line in YanCheng. Previously, the company has successively won the bids for central enterprises` components bidding projects such as China Resources Power, Guangdong Electric Power, China Southern Power Grid, and State Power Investment Corporation. We believe that the company's active expansion in the module market is due to the company's cost advantage in producing modules and the company's intention to reduce its earnings volatility. In terms of cost advantages, in the event of an insufficient supply of polysilicon, the company can supply raw materials such as polysilicon and silicon wafers to ensure that the production capacity utilization rate of the company's modules remains high to share the fixed costs. In terms of reducing the volatility of the company's earnings, the market believes that the polysilicon may be oversupplied in 2024. When the price of polysilicon falls, the company's profitability will be damaged. Therefore, the company's module business will hedge against the volatility of the earnings of polysilicon, which will reduce the volatility of the company's total earnings. Since the construction period of the project is within 24 months after obtaining the complete procedures of obtaining land and other procedures, we expect the project will start to realize the PV module's revenue to the company in late 2024 or early 2025.

Company valuation

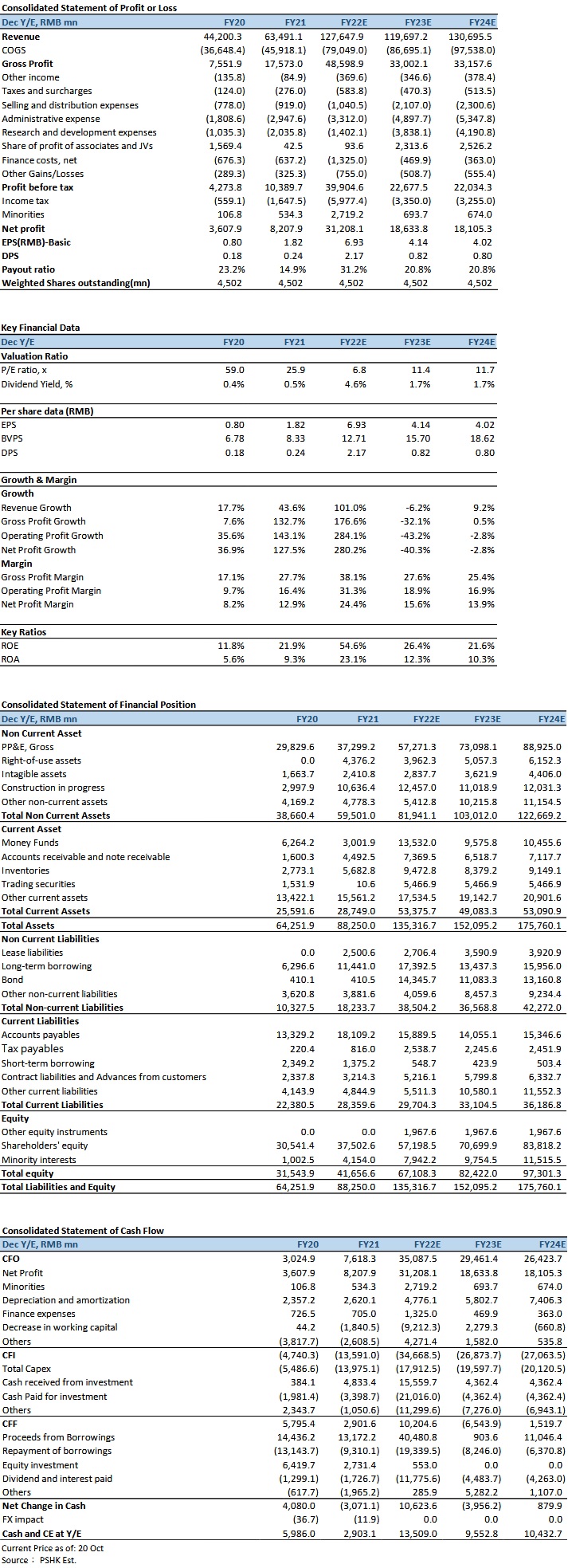

We believe that the company has significant cost and purity technology advantages in the field of polysilicon. In the future, the company's substantial expansion of production capacity will drive the company's polysilicon output. However, the expected decline in polysilicon prices in the next two years may lead to a decline in the company's earnings. The company's PV cell business is supported by its own supply of raw materials, and its capacity utilization rate is much higher than the industry average. Therefore, we expect the company's PV cell shipments to grow substantially, in line with the expansion of production capacity. We estimate that the net profit per share attributable to the shareholders in 22/23/24 will be 6.93/4.14/4.02 yuan, corresponding to 6.8/11.4/11.7x price-earnings ratio (P/E). With the reference to the valuation of polysilicon and PV cell companies, we believe that the company's valuation should be much higher than that of peer polysilicon to reflect the company's competitive advantage and the valuation of cell business, but the valuation should be lower than the PV cell company Aiko. We conservatively give the company a 13x PE in 2023, with a target price of 53.8 yuan and an “accumulate” rating. (Current price as of October 20)

Risk factors

1) PV demand is lower than expected; 2) Market competition intensifies; 3) The company's production capacity is lower than expected.

Financial

Click Here for PDF format...