Company Profile

L`OCCITANE is an international group that manufactures and retails beauty and well-being products that are rich in natural and organic ingredients, through its brands �X L`OCCITANE en Provence, Melvita, Erborian, L`OCCITANE au Brésil, LimeLife by Alcone, ELEMIS, Sol de Janeiro and Grown Alchemist. As at 31 March 2022, the Company has more than 3068 retail outlets (a decrease of 20 or 0.6%). including around 1,500 owned stores, and is present in 90 countries. The total number of own retail stores was 1375 as at 30 June 2022, representing 115 net closings year to date.

The Company further closed underperforming stores during FY2022, including 21 shops in the US. At the end of March 2022, the breakdown of the 1,523 own stores by brand and change over last year were as follows: L`Occitane en Provence (1,354; -35), L`Occitane au Brésil (65; +1), Melvita (39; -11), Erborian (14; -1) and ELEMIS (18; +13). The number of non-own stores increased by 13 or 0.8%.

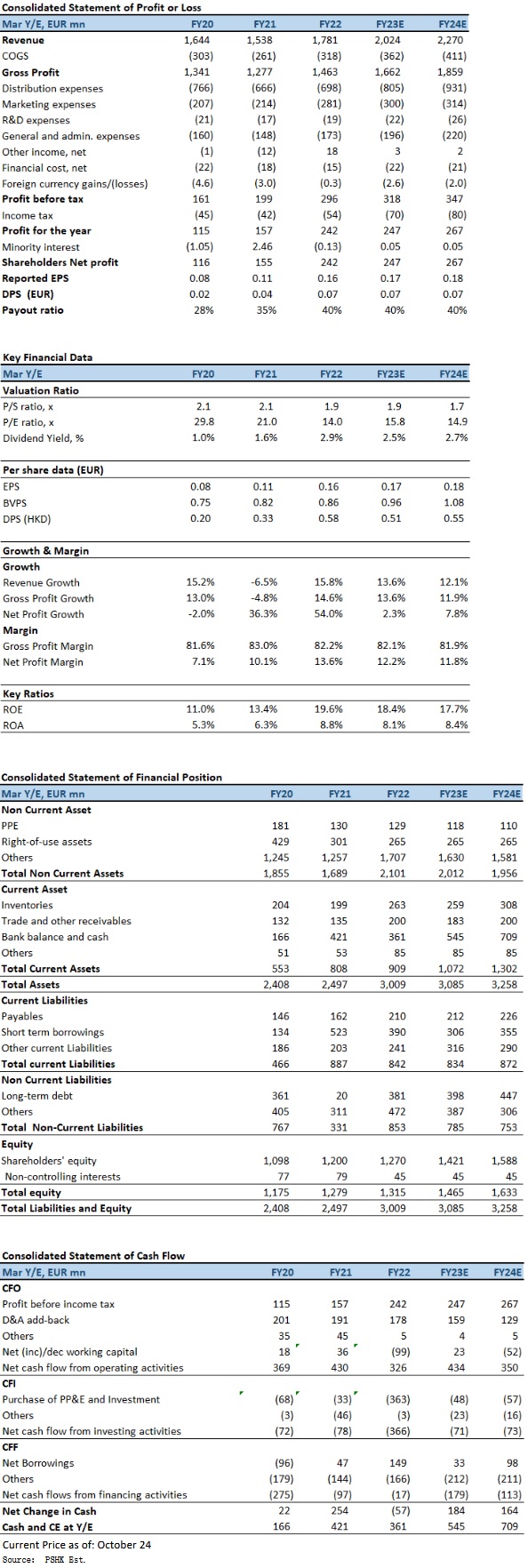

net profit for FY2022 hits record high, op margin the highest level since listing

For the FY2022 (at the end of March 2022), the Company's reported net sales were ��1781.4mn, representing an increase of 15.8% YoY at reported rates. The business environment continued to improve as countries in Europe and the Americas began to lift the COVID-19 related restrictive measures. Retail channels saw a strong rebound in footfall while online channels remained dynamic. Travel retail, spas and cruise ship businesses also benefited from the comeback of local and international travelers. During the period, net profit for FY2022 was a record ��241.9mn, an increase of 57.5% or ��88.3mn as compared to restated ��153.6mn for FY2021, and a 17.4% operating margin, the highest level since listing. Basic and diluted earnings per share in FY2022 were ��0.165 and ��0.164 respectively (FY2021: basic ��0.103 and diluted ��0.103), an increase of 60.2% and 59.2% respectively. Dividend payout ratio from 35% to 40%, with a dividend per share that is 78.6% higher than it was in FY2021.

Performance by brand, L`OCCITANE en Provence accounted for 76.8% of the company's total sales, growing 13.2% at constant rates. Sales momentum of the brand rebounded strongly in Europe and the Americas following the removal of restrictive measures related to COVID-19. Retail business contributed most to overall growth as stores reopened and footfall normalized. ELEMIS accounted for 12.5% of the total sales in FY2022, an increase of 2.3 points as compared to FY2021. ELEMIS posted an exceptional growth of 37.4% at constant rates. The spa wholesale and cruise ship businesses rebounded strongly as travel restrictions loosened. Online channels continued to grow, thanks to the successful omni-channel business model and strengthened collaborations with digital partners. The US contributed most to the brand's overall growth in FY2022, followed by the UK and China.

The Company began to consolidate Sol de Janeiro in January 2022 and it contributed ��26.1mn, or 11.0% to overall growth in FY2022. In local currency, Sol de Janeiro delivered 46.7% growth in 4Q2022FY. LimeLife posted a sales decline of 31.3% at constant rates in FY2022. In addition to the high base last year, the brand faced difficulties in recruiting and retaining beauty guides as the US economy returned to normal and employment conditions improved. The other brands together finished FY2022 with 19.0% growth at constant rates, with key contributions from the continuous success of Erborian and the strong rebound of L`OCCITANE au Brésil. Both retail and wholesale channels benefited from the removal of restrictive measures.

By geographic area, Japan's net sales for FY2022 were ��206.0mn, a decrease of 4.3% as compared to FY2021, accounted for 11.4% of the total sales. At constant exchange rates, the growth was 0.4%. Hong Kong's net sales for FY2022 were ��118.9mn, an increase of 25.7% as compared to FY2021. At constant exchange rates, the growth was 24.0%, accounted for 6.6% of the total sales. China's net sales for FY2022 were ��328.0mn, an increase of 24.4% as compared to FY2021. At constant exchange rates, the growth was 16.8%, contributing most to the Overall Growth, accounted for 18.1% of the total sales. Online channels were particularly dynamic and skillfully implemented well-thought-out campaigns that leveraged celebrities on TMall and JD.com to drive social media buzz and recruit new customers. As a result, L`OCCITANE en Provence outperformed the market during key shopping festivals and remains one of the top-ranked brands in the premium body care and hand care categories. Taiwan's net sales for FY2022 were ��51.5mn, an increase of 8.6% at reported rates. At constant exchange rates, the growth was 2.8%, accounted for 2.8% of the total sales.

France's net sales for FY2022 were ��96.0mn, an increase of 10.8% as compared to FY2021, accounted for 5.3% of the total sales. The United Kingdom's net sales for FY2022 were ��197.5mn, an increase of 27.9% as compared to FY2021. At constant exchange rates, the growth was 21.4%, accounted for 10.9% of the total sales. The United States` net sales for FY2022 were ��296.8mn, an increase of 14.8% as compared to FY2021. At constant exchange rates, the increase was 13.5%, accounted for 16.4% of the total sales. Brazil's net sales for FY2022 were ��48.3mn, an increase of 40.1% as compared to FY2021. At constant exchange rates, the increase was 37.0%, accounted for 2.7% of the total sales. Russia's net sales for FY2022 were ��62.6mn, an increase of 22.8% as compared to FY2021. At constant exchange rates, it achieved growth of 24.8%, accounted for 3.5% of the total sales. Other geographic areas` net sales for FY2022 were ��404.4mn, an increase of 16.1% at constant exchange rates. Countries with strong positive contribution were Korea, Mexico, Spain and Canada, accounted for 22.3% of the total sales.

The reported cost of sales increased by 22.0%, or ��57.2 million, to ��317.9 million in FY2022. The gross profit margin decreased 0.8 points to 82.2% as compared to FY2021. The decrease is attributable to the following factors: deconsolidation of US subsidiary during the Chapter 11 proceedings for 0.6 points; unfavourable channel mix from higher sell-in proportion and unfavourable brand mix from ELEMIS and Sol de Janeiro, which have more sell-in businesses; and higher freight and duties, partly due to inventory rebuild and partly due to higher shipping costs.

Positive start into FY23Q1 with solid sales growth

Positive start into FY23Q1 (for the three months ended 30 June 2022) with sales of ��416.0mn and double-digit sales growth at reported rates (+23.4%) and constant rates (+15.8%), despite the macroeconomic challenges in Q1. On a like-for-like basis, i.e. excluding the recently acquired brands, the Russia market due to divestiture, and the deconsolidation of the US subsidiary, sales growth was 5.1% YoY.

Performance by brand, strong growth posted from L`OCCITANE en Provence (5.9% at constant rates), ELEMIS (9.8% at constant rates) and recently acquired brands Sol de Janeiro and Grown Alchemist, approximately an increase of 60% in local currency as compared to the same quarter last year, prior to the acquisition.

As the COVID-19 restrictions and lockdowns severely impacting major markets such as China, A lockdowns and restrictive measures in Shanghai and other major cities in April and May 2022. Both offline and online sales were affected. In addition to store closures, the warehouse in Shanghai was also closed, causing disruption to store replenishments nationwide, which caused APAC only grew 1.2% at constant rates. However, sales rebounded strongly t in June 2022 as soon as the restrictive measures were eased. China ended the first quarter with a high-teens decline at constant rates. Americas grew 55.5% at constant rates. EMEA saw a rebound in the quarter and grew 10.3% at constant rates, with strong contribution from travel retail and distribution sales in the region, as well as a rebound in retail sales in France and Germany.

Accelerated sales growth in FY23Q2

Accelerated sales growth in FY23Q2, achieving sales of ��900.5 million in FY23H1, representing a growth of 24.2% at reported rates or 16.1% at constant rates. Like-for-like sales growth was 5.9% in FY23H1, an acceleration from 5.1% in FY23Q1 to 6.7% in FY23Q2. Solid performance in FY23H1 was driven by key brands L`OCCITANE en Provence (+3.4%) and ELEMIS (+13.1%), as well as the inclusion of Sol de Janeiro (+65% in local currency). The fastest-growing region was Americas (+59.8%), followed by EMEA (+8.2%) and APAC (+1.9%).

Investment Thesis

However, towards the end of FY2022, the macroeconomic conditions turned challenging, with a resurgence in COVID-19 outbreaks in many key markets and the geo-political situation in Ukraine and Russia. 110 of the net closings were in Russia, due to the company's divestiture in June 2022, which would have a negative impact on FY2023 revenue. In addition, we believe that some concerns around the macro outlook remain (especially the risk of a global economic downturn, sharp currency fluctuations and persistently high inflation), resulting in still relatively volatile financial results. We expect FY2023E-FY2024E EPS to be ��0.17 and ��0.18 respectively, with FY2023E PT of HKD25.89 (with fairly low EUR/HKD exchange rate of $7.5 to $7.6 for the recent month, the corresponding target price would be HK$25.09 to HK$25.42), implies a FY2023E P/E of 19.9x (~5-yrs historical average). Our investment rating is ��Buy��.

Risk factors

1) Resurgence of COVID in Mainland China; 2) Sharp fluctuations in FX; 3) Operation risks in overseas business; and 4) Global economy shrinks more than expected.

Financial

Click Here for PDF format...