Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

Automobile & Air (ZhangJing)

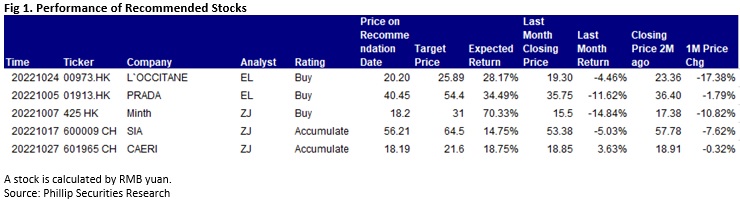

This month I released 3 updated reports of Minth (425 HK), SIA (600009 CH) and CAERI (601965 CH), which got attention by their unique Competitive edge. Among them, we prefer CAERI.

CAERI is the only listed company in the A-share automotive industry that is engaged in automotive technology service business. It has strong automotive R&D and testing capabilities. In H1 of 2022, CAERI reported a revenue of RMB1,340 million, down 25.58% yoy. The decline in revenue was mainly due to the Company's initiative to control the scale of the equipment manufacturing business with declining market prosperity, resulting in a sharp decline in its revenue by nearly 80% yoy. However, the significant improvement of the sales structure led to a sharp increase in the gross margin during the reporting period, which greatly improved the profitability. The Company reported a net profit attributable to the parent company of RMB300 million, up 14.1% yoy, and a net profit attributable to the parent company excluding non-recurring items of RMB299 million, up 19.26% yoy.

On a closer look at the business segments, 1) the Company reported a revenue of RMB1,139 million in the automotive technical service business, up 30.16% yoy, mainly due to the effectiveness of the Company's strategy of strengthening market development, as well as the continuous optimization of the business structure, which led to a year-on-year improvement in the non-regulatory business such as wind tunnel, new energy and intelligent connected business; 2) the Company reported a revenue of RMB201 million in the equipment manufacturing business, down 78.27% yoy, mainly because under the impact of the market quotation on the SPV modification and sales business, the Company strengthened risk management and controlled the scale of the business, resulting in a year-on-year decrease in the revenue.

During the reporting period, the Company continued to make breakthrough in the innovative business, and the revenue proportion of the automotive technical service business with high gross margin (gross margin of 51%) expanded by 36.4 ppts to 85%. A better sales structure has driven a sharp increase in the profitability: In H1, the Company's comprehensive gross margin reached 43.68%, up 14.69 ppts yoy, and the net profit margin climbed to 23.4%, up 8.3 ppts yoy.

With the entry of Internet companies and new car-making forces, the vehicle architecture has evolved to "intelligent cockpit + autonomous driving + skateboard chassis", and the integration of automotive technology and cross-sector technology has accelerated. The Company's high value-added business is expected to enter the fast lane, and its future results will also benefit from the rising proportion of high value-added business.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released 2 reports of L`OCCITANE (973.HK) & PRADA (1913.HK).

The Prada Group (1913) is a leading business in the luxury goods industry, where it operates with the Prada, Miu Miu, Church's and Car Shoe brands producing and distributing leather goods, footwear and apparel. It also operates in the food industry with Marchesi 1824, in the most prestigious sailing races with Luna Rossa and in the eyewear and fragrance industries under licensing agreements.

The Prada owns 23 manufacturing plants (20 in Italy, 1 in the United Kingdom, 1 in France and 1 in Romania) and its products are sold in 70 countries worldwide, primarily through directly operated stores. The Prada Group's products are also sold directly through the brands` e-commerce activity and indirectly by selected prestigious department stores, independent retailers in very exclusive locations, and important e-tailers.

For the 1H2022, Prada Group generated net revenues of EUR1,900.9mn, up by 22.5% at constant exchange rates from those of the 1H2021 and by 22.2% from 1H2019, exceeded pre-pandemic levels. At current exchange rates, the 2021 performance was boosted by 26.6% growth. The recurring operating result for the period, or EBIT Adjusted, was EUR331mn, whereas in increased by 99.4% compared to 1H2021 (EUR165.9mn). The EBIT Adjusted was also considerably higher than 119.8% that of the 1H2019 (EUR150.5mn). Profit attributable to shareholders was EUR188.3mn, an increase of 93.6% YoY. Basic EPS were EUR0.074 (1H2021: EUR0.038), an increase of 94.7%.

By brands segment, Prada brand retail net sales were 28.1% (at constant exchange rates) higher than in the first six months of 2021 and 45.5% (at constant exchange rates) above 1H2019. Miu Miu's sales increased by 13.6% (at constant exchange rates) from 1H2021 and by 5.3% (at constant exchange rates) from that of 1H2019. Miu Miu finds itself in a relaunch phase. Church's, the brand most affected by the geographical exposure to Europe, reported a gain of 28.7% (at constant exchange rates) on the 2021 sales. Royalty income, supported by the growth in the eyewear segment, rose by 22.2% YoY.

For the 1H2022, the gross margin corresponded to 77.7% of the net revenues, up substantially 340bps from the 74.3% of 2021. Despite cost inflation, for example in logistics costs, a higher average price, greater absorption of production overheads, a better sales mix in terms of distribution channels and a favorable exchange rate were behind the improvement of operation result. The increase is even more significant when comparing the 2022 margin with that of the 71.7% in 1H2019.

For 2H2022, management would benefit from further operating leverage and also remains optimistic on the underlying demand of the Chinese market. However, we believe that some concerns around the macro outlook remain, resulting in continued volatility in coming results.

Click Here for PDF format...