Overview

NetEase (9999.HK) is a leading internet and technology company in China. Its main business includes gaming and related value-added services. The company develop and operate a variety of popular and enduring mobile and PC games in China. Besides, NetEase's other businesses include: (2) its subsidiaries Youdao (NYSE: DAO), mainly provide technology-based intelligent learning services and products. (3) its subsidiaries NetEase Cloud Music (9899.HK), mainly provide online music service and rich music community experience. (4) its innovative businesses and others, for example the self-operated lifestyle brand NetEase Yanxuan.

A review of Q2 2022 Results

NetEase (9999.HK) has announced the operating data from Mar to June 2022. NetEase (9999.HK) revenues amounted to RMB 23,159.1 million, representing an increase of 12.8% YoY, but a decrease of 1.7% QoQ. Gross profit amounted to RMB 12941.5 million, representing an increase of 15.7% YoY, and an increase of 0.82% QoQ.

Gaming and related value-added services revenue amounted to RMB 18,139.8 million, representing an increase of 15% YoY, but a decrease of 2.7% QoQ. Among them, online games are the main component of games and related value-added services. In this quarter, the revenues from online games accounted for 92.8% of net income from games and related value-added services. In the previous quarter and the same period last year, the proportion was 92.7% and 92.1% respectively. The net revenues from mobile games accounted for 66.1% of the net revenues of online game, it accounted for 66.9% and 72.1% in FY2022Q1 and FY2022Q2 respectively. In addition, Gross profit margin accounted for 64.9%, it accounted for 62.2% and 63.2% in FY2022Q1 and FY2021Q2 respectively. The YoY increase in games and related value-added services gross profit was primarily due to increased net revenues from both mobile and PC games, including the newly launched Naraka: 4 Bladepoint and Harry Potter: Magic Awakened which were released in the third quarter of 2021 and other existing games such as Fantasy Westward Journey Online.

Youdao revenue amounted to RMB 956.2 million, representing a decrease of 26.1% YoY, and a decrease of 20.3% QoQ. The gross profit margin accounted for 42.8%, it accounted for 53.1% and 52.3% in FY2022Q1 and FY2021Q1 respectively. The QoQ decrease in Youdao gross profit primarily resulted from a decline in economic scale due to decreased learning services revenues in the second quarter of 2022. The YoY decrease was mainly due to the conclusion of its after-school tutoring services for academic subjects under China's compulsory education system.

NetEase Cloud Music revenue amounted to RMB 2191.5 million, representing an increase of 29.5% YoY, and an increase of 6.01% QoQ. Gross profit margin accounted for 13%, it accounted for 12.2%% and 4.1% in FY2022Q1 and FY2021Q1 respectively. The QoQ and YoY increases in Cloud Music gross profit were primarily due to increased net revenues from its membership subscriptions and social entertainment services, as well as improved cost control.

Innovative businesses and others revenue amounted to RMB 1871.5 million, representing an increase of 6.1% YoY, and an increase of 13.7% QoQ. Gross profit margin accounted for 25.8%, it accounted for 21.7% and 27.3% in FY2022Q1 and FY2021Q1 respectively. The QoQ increase in innovative businesses and others gross profit was primarily due to increased gross profit contribution from Yanxuan and advertising services.

Game business features

NetEase owns many popular and profitable games, it can be divided into two markets, China gaming market and overseas gaming market (some popular games are successful in both markets).

In China gaming market

The series of Westward Journey include Fantasy Westward Journey Online, etc. In 2004, the PC version was officially operated for a fee and the mobile version was launched in 2015. As the `Evergreen Tree` of NetEase, Westward Journey has brought NetEase a stable and substantial income. On the mobile version, according to the data survey agency Sensor Tower (the data does not include third-party Android platforms in China and other places, the same below), Fantasy Westward Journey online ranked 7th in global mobile game revenue and ranked 3rd in China in July. It is a pity that the theme of `Westward Journey` has not been able to enter the overseas market for many years, and it only developed in China.

Infinite Lagrange is an interstellar themed mobile simulation game. Since its launch in August 2021, it has mainly developed in the China gaming market. According to Sensor Tower, Infinite Lagrange has 400,000 downloads and USD 8 million revenue in August. Also, its ranked 12th in China mobile game revenue in July.

In overseas gaming market

Naraka: Bladepoint is a martial arts-style action-adventure battle royale game. It only has a PC version for the time being, and the mobile version is still in the development stage. the global sales of Naraka: Bladepoint exceeded 10 million In June 2022, becoming the first domestic buyout game with global sales exceeding 10 million, and 50% of them came from overseas markets.

Identity V is a multiplayer asymmetric competitive mobile game, it released in April 2018. Although the popularity in China has waned, the performance in the Japanese market is still very strong. The game continues to cooperate with other famous Japanese cultural works to attract players and maintain its popularity. For example, it cooperated with the popular Japanese animation `Death Note` in May 2021. According to Sensor Tower, Identity V has 200,000 downloads and USD 5 million revenue in August.

Knives Out is a survival battle royale game, its situation is similar to Identity V, the popularity in China has waned, but the performance in Japanese market is still very strong. The game is also through cooperate with other popular Japanese cultural works to attract players and maintain its popularity. For example, it cooperated with the popular Japanese animation `Sword Art online`in July 2022. According to Sensor Tower, Knives Out has 90,000 downloads and USD 1200 million revenue in August.

Diablo: Immortal is a massive online multiplayer action role-playing game jointly launched by NetEase and the global game giant Blizzard Entertainment on June 2, 2022. The Chinese server was released on July 25, and it was launched on both PC and mobile platforms. The series of Diablo launched by Blizzard in December 1996, and the series has sold more than 24 million worldwide. It is deeply concerned and loved by players around the world. According to Sensor Tower, after Diablo: Immortal released, the mobile version of this game ranked 8th July globally. Since the China server was launched on July 25, the data did not fully reflect the explosiveness and profitability of the game. In addition, the mobile version of this game took only 8 weeks to reach USD 100 million in revenue, making it the second fastest mobile game in the world, only two weeks longer than Pokemon Go.

Positive factors

1. Developing overseas gaming market to drive revenue growth

In recent years, NetEase has actively explored the overseas gaming market. The CEO Ding Lei said that his company 80% of R&D resources are invested in China currently, the overseas market only takes over 10%, but it will expand to 40% to 50% in the future. In Japan market, Onmyoji, Knives Out and Identity V, etc. have successively entered the Japanese mobile game market, NetEase builds their reputation and image among Japanese players. Investors can expect more games will be popular and profitable in Japan in the future. In addition, the Diablo: Immortal jointly launched by NetEase and Blizzard swept the world, however the interim report did not reflect the profit that created by Diablo: Immortal in time. Investors can expect this game to be a catalyst for NetEase's revenue and stock price, but investors need to keep observing the game sustainability.

2. Expert in games localization to increase game competitiveness and longevity

NetEase is good at localizing games to integrate and enter the local market. For example, when the Identity V entered the Japanese market, it did not attract much attention. Later, it attracted Japanese players to try it through the cooperation with Junji Ito, a well-known Japanese horror cartoonist, and then became famous. NetEase's strategy attracts players by cooperating with other famous cultural works. It can achieve the purpose of increasing the competitiveness and longevity of the game, and it also proves that this strategy can bring freshness to players and attract new players.

3. New games are expected to improve profitability

Besides the popular game Diablo Immortal, the trendy casual competitive game Egg Go launched in May also caused a boom in China. According to Sensor Tower, the game was downloaded 2 million in China in August, and it was most downloaded game by NetEase in August. Investors can expect this game to monetize and increase profitability while stabilizing player enthusiasm. In addition, NetEase is preparing to launch mobile version of popular PC games like Naraka: Bladepoint, Justice and Ghost World Chronicle. It also expected to boost the company's revenue from mobile gaming platforms.

Risk factors

1. U.S. delisting risk

NetEase is listed on the Nasdaq Stock Exchange and regulated by the U.S. Securities and Exchange Commission. In recent years, due to the U.S. Holding Foreign Companies Accountable Act, Chinese companies and other foreign companies need to comply with relevant regulations, such as allowing relevant US personnel to check the company's audit documents. However, due to the reservations from relevant Chinese authorities to disclose sensitive information, the company may fail to comply with U.S. regulations, so there is a delisting risk to relevant companies. If NetEase delists from Nasdaq Stock Exchange, there is a chance that the stock price will fluctuate significantly. However, the relevant departments of China and U.S. have reached an agreement recently. The delisting risk of listed companies in the U.S. such as NetEase has been slightly reduced, but it is still necessary to pay attention to the relevant news.

2. Policy risks from China

Policy risks can be divided into two categories, include the restriction of teenager's online game time policy and the game license approval policy. In term of restriction of teenager's online game time policy, Chinese teenagers who under 18 years old are only allowed to play games for up to 3 hours a week, and only on weekends and festivals. Although teenagers have low spending power and they only make little impact on game revenue, teenagers are difficult to enjoy playing games under the restriction policy, it will have a negative impact on building players community and user stickiness, eventually reduce the game's lifespan and potential revenue. In term of the game license approval policy, relevant Chinese authorities are stricter with game license approvals. In recent years, the approval of game license has been stopped twice, it affects the business development and revenue plans of game companies. Although relevant department re-approve game licenses and there are signs of normalization, the relevant departments tend to approve the game licenses from small-sized companies. Pioneers like Tencent and NetEase only got their first game license on Sep 13. Investors need to pay attention to the situation of game license approval, if NetEase's game license get approved regularly, it may become a catalyst for the stock price to rise.

Valuation and recommendation

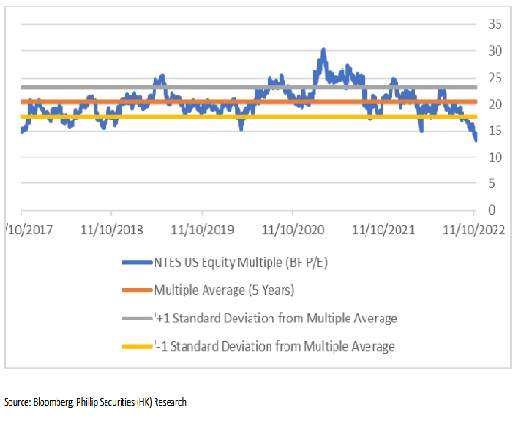

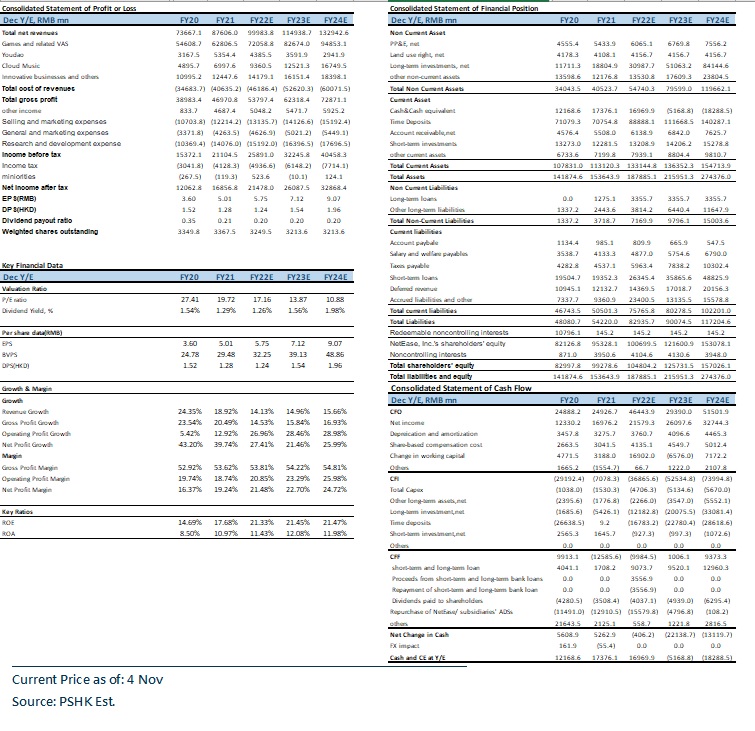

We believe that the Chinese gaming market is currently at the end of the restructuring period. In order to adapt the changes of China policies and reduce policy risks, Chinese game companies are accelerating their development in overseas markets, including the acquisition of overseas game studios, etc. This act will lead the whole industry operating costs increase. However, we believe that NetEase, as one of the leading game companies in China and even in the world, owns many popular games that can continue to be monetized. At present, several games have successfully entered overseas markets such as Japan. Compared with average game companies in China, NetEase has rich resources and experience in developing overseas markets, which is beneficial for NetEase to develop overseas markets. In addition, NetEase is the only company in China that has in-depth cooperation with Blizzard Entertainment. NetEase not only represent Blizzard Entertainment's game in China, but also jointly launched global popular game, Diablo: immortal. This is the unique advantage of NetEase in long-term development of overseas business. We expect NetEase net profit growth are 27.41%, 21.46% and 25.99% in FY2022-2024 respectively. Net profit per share attributable to shareholders are RMB 5.75, 7.12 and 9.07 in FY2022-2024 respectively. Corresponding P/E ratio are 17.16/13.87/10.88x and NetEase's five years average P/E is around 20.49. We believe that new games will boost the revenue growth, giving NetEase 18x PE in 2023 and a target price of 138.41 HKD (calculated at the exchange rate of RMB to HKD 1.08), with a `buy` rating. (Current price as of November 4)

Financial

Click Here for PDF format...