|

LUYE PHARMA(2186)

Analysis:

LUYE PHARMA (2186) is principally engaged in the development, production, marketing and sale of pharmaceutical products in four key therapeutic areas, namely oncology, central nervous syste, cardiovascular system, alimentary tract and metabolism. The Group has a portfolio of over 30 products, covering over 80 countries and regions around the world, including large pharmaceutical markets — China, the U.S., Europe and Japan, as well as fast growing emerging markets. Its class 1 innovative drug Toludesvenlafaxine Hydrochloride Extended-Release Tablets (Trade name: Ruoxinlin) developed by the Group has been approved by the National Medical Products Administration (NMPA) of the PRC for treating Major Depressive Disorder. Separately, Denosumab Injection (Boyoubei) developed by a subsidiary of the Company, namely Shandong Boan Biotechnology has also been approved by the NMPA for the treatment of postmenopausal women with osteoporosis at high risk for fracture. In addition to China, Boyoubei is being developed in Europe and the U.S., with a plan to be marketed in the global markets. (I do not hold the above stock)

Strategy:

Buy-in Price: $2.25, Target Price: $2.50, Cut Loss Price: $2.15

|

JD(9618)

Analysis:

JD.com is a leading supply chain-based technology and service company in China. For the first six months ended 2022, the group's revenue amounted to RMB 507.3 billion, representing an increase of 11.0%. Net product revenues increase of 9% and net service revenues increase of 23.9%. Cost of revenues amounted to RMB 437.9 billion, representing an increase of 10.5%. Operating income amounted to RMB 6.17 billion, representing an increase of 214.43%. Net profit for the period amounted to RMB 510 million, representing a decrease of 87.62%. The drop in net profit for the period was mainly due to the sharp drop in other income or expense. JD.com performed brilliantly on the 11/11 Online Shopping Festival, with a significant increase in the YoY turnover of many products. In addition, the relaxation of China Covid-19 prevention policies will benefit the company's sales and cost control. We expect the company's share price will rise further.

Strategy:

Buy-in Price: $192.5, Target Price: $214, Cut Loss Price: $180

|

|

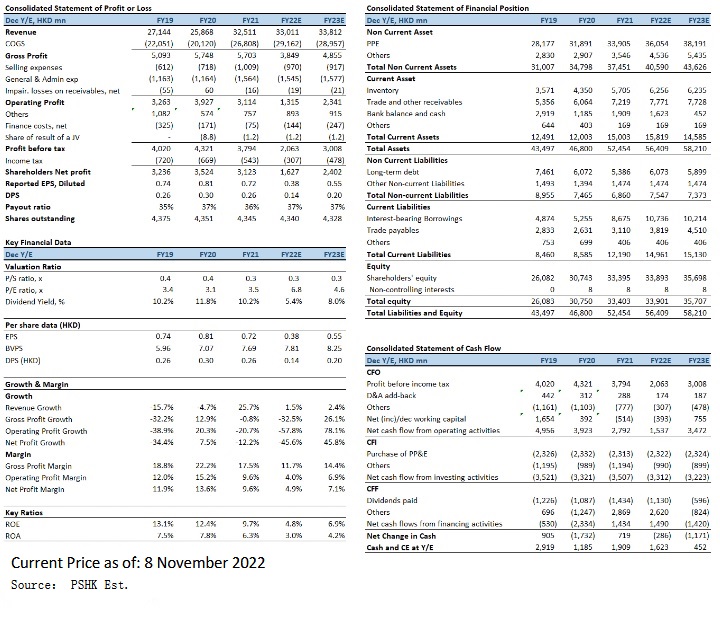

Lee & Man Paper Manufacturing (2314.HK) - 1H2022 results in line with consensus

Company Profile Established in 1994, Lee & Man Paper Manufacturing (“LMP”) was listed on the Main Board of the Hong Kong Stock Exchange on September 2003. LMP manufactures linerboards of various grades and corrugating medium of different specifications used for different industrial packaging purposes. Over the years, in addition to boosting production scale, LMP has been relentless in pushing to form a vertically integrated operation that covers pulp making and recovered paper collection so as to assure it has stable raw material supply. LMP currently has 5 paper mills, 3 tissue mills and 1 pulp factory in China. They are distributed in Zhongtang Town and Hongmei Town of Dongguan City, Guangdong Province, Changshu City, Chongqing Yongchuan District, Ruichang City, Jiangxi Province, etc. In addition, LMP also has production bases in Vietnam, Malaysia and Indonesia. As of the end of December 2021, the Company had an annual production capacity of over 8.695 million tons(~6.88 million tons of paper, ~180,000 tons of pulp, ~640,000 tons of pulp board and ~995,000 tons of tissue paper). 1H2022 results in line with consensus LMP total revenue for the six months ended 30 June 2022 (1H2022) increased by 0.6% YoY to HK$15.3bn. Net profit attributable to shareholders decreased by 58.8% to HK$797mn, which is consistent with the results announced in July. The EPS was HK18.46 cents (1H2021: HK44.54 cents). Interim dividend of HK6.50 cents per share (1H2021: HK15 cents), decreased by 56.7% YoY. During the period, mainland paper manufacturers` profitability has been under pressure as a result of rising prices of raw materials such as wood pulp, energy, and high logistics and transportation costs, plus lockdown of cities amid the pandemic leading to weakened demand. The aggregate sales amounted decreased by 3.9% YoY to 2.96 million tons, with net profit per ton decreased by HK$358 to HK$292. The overall gross profit plunged 50.4% to $1.656bn, while the overall gross profit margin fell 11.1ppt to 10.8% due to the significant increase in raw material prices. In terms of expenses, 1H2022 distribution and selling expenses were HK$446mn, down 11.5% YoY, accounting for 2.9% of total revenue; General and administrative expenses were HK$598mn, down 17.4% YoY, accounting for 3.9% of total revenue. By segments, the packaging paper segment's profit dropped 72.4% YoY to HK$610mn, while segment's revenue rose slightly by 0.6% YoY to HK$13.051bn, accounting for 85.4% of the total revenue. The tissue paper business segment's profit increased 24.8% YoY to HK$286mn, while segment's revenue declined 0.3% to HK$2003mn, accounting for 13.2% of total revenue. The pulp segment's profit rose 19.9 times YoY to HK$60.22mn and segment's revenue rose 16.1% to HK$216mn, accounting for 1.4% of total revenue. Investment ThesisLooking ahead, China continues to tighten control over plastic packaging, giving room for using paper packaging as a substitute, while consumption behavior has changed amid the pandemic with more people shopping online, and correspondingly the demand for packaging paper has climbed. LMP continued to consolidate upstream resources and develop a vertical business model covering pulp-making and waste paper recycling, and plans to add pulp production lines at its plants in Jiangxi province and Chongqing, so as to enhance raw materials supply (the new production lines are expected to start operation in 2023). Regarding tissue paper business, LMP plans to establish a new plant in Guangxi province and expects to add new production line with annual capacity of 300,000 tons of bleached pulp by the end of next year at the earliest (total production capacity is around 1,000,000 tons). LMP is actively expanding its recycled pulp business and enhancing raw material deployment, which should be expected to mitigate the impact of rising raw material costs on profits in the long run. With the gradual easing of the pandemic in June, overall domestic consumer confidence is sluggish and we remain cautious about the degree of business recovery in the second half of the year (Q4 will be the traditional peak demand season), but the low valuation level to some extent reflects the company's weak fundamentals. LMP has its eye on the Southeast Asian market and has already established production capacity in countries such as Vietnam and Malaysia, that would enhance the revenue and production efficiency. Thus, LMP's profitability would expected some improvement in next year. We expect FY2023E-FY2024E EPS to be HK$0.38 and HK$0.55 respectively, with FY2023E PT of HKD3.70, implies a FY2023E P/E of 6.6x (~5-yrs historical average minus 1 std. deviation). Our investment rating is “Buy”. Risk factors1) Significant fluctuations in raw material prices; 2) escalating trade tensions between the U.S. and China further dampening downstream demand; 3) faster than expected increase in industry capacity leading to price wars; and 4) FX rate risk. Financial

Click Here for PDF format...

| Recommendation on 14-11-2022 | | Recommendation | Buy | | Price on Recommendation Date | $ 2.550 | | Suggested purchase price | N/A | | Target Price | $ 3.700 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2022 Phillip Securities (HK) Ltd. All Rights Reserved.

|