Company Profile

Hengan founded in 1985, is a famous manufacturer of household paper and maternal & child hygiene products. The market shares of the three leading products, namely women's sanitary napkins, baby diapers, and household tissues, is among the best in the domestic market.

1H2022 sales bucked the trend and achieved growth of over 10%

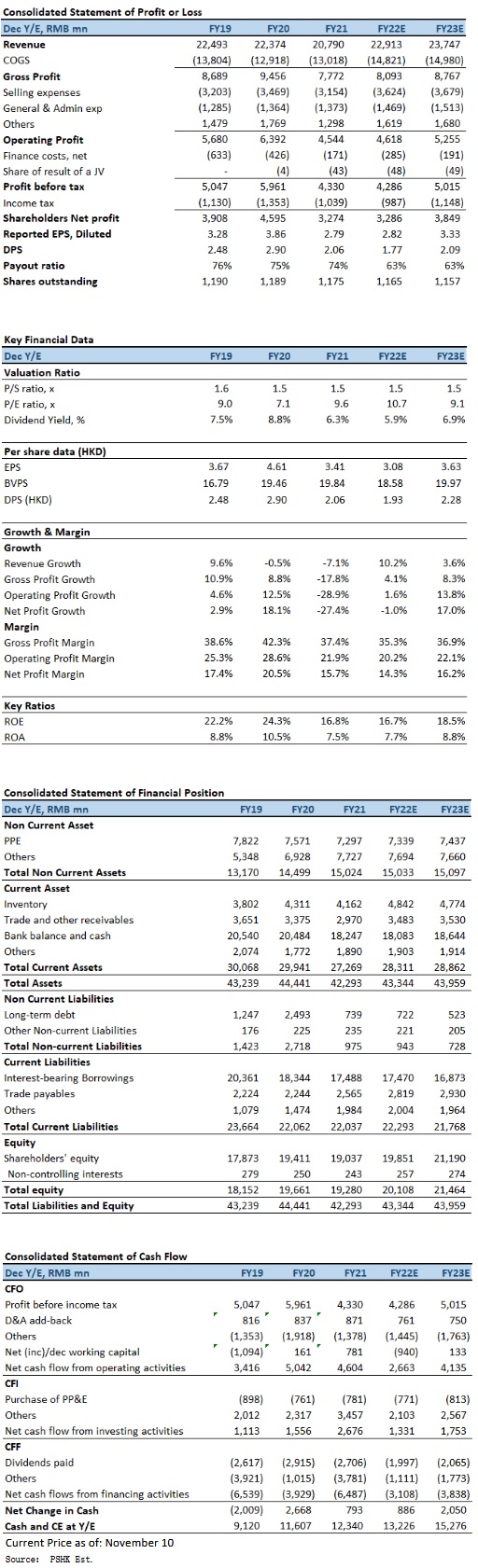

For the six months ended 30 June 2022 (1H2022), Hengan's revenue increased by about 12.3% to RMB11,200.021mn, above market expectation. During the period, operating profit fell about 25.8% to RMB1885.753mn (1H2021: RMB2540.583mn). Although the Hengan's sales bucked the trend and achieved growth of over 10%, the striking depreciation of the RMB against the US dollar and HK$ during the period resulted in a significant foreign exchange loss in the Hengan's operations (RMB367.797mn). Therefore, profit attributable to shareholders was RMB1,276.191mn (1H2021: RMB1,860.292mn), representing a decrease of 31.4% YoY. If deducting the operating foreign exchange loss, profit attributable to shareholders decreased by 10.9% YoY instead. Basic EPS was RMB1.098 (1H2021: RMB1.574), with an interim dividend decreased by 30% YoY to RMB0.70 per share (1H2021: RMB1.00).

During the period under review, rising raw material prices and operating costs have brought enormous pressure to the industry, which accelerated market consolidation of eliminating the weak and retaining the strong. The price of wood pulp, the main raw material of tissue paper, remained high during the period due to geopolitical upheavals, the epidemic and inflation. Overall gross profit slightly increased by 0.3% to RMB3,942.191mn (1H2021: RMB3,930.671mn), however, the overall gross profit margin dropped to 35.2% (1H2021: 39.4%).

By business segment, the sales of sanitary napkin business grew 3.3% to RMB3128.524mn (1H2021: RMB3029.97mn), accounting for around 27.9% (1H2021: 30.4%) of the Hengan's total revenue. However, the surge in petroleum and commodity prices has led to a price hike in petrochemical raw materials used in sanitary napkins, resulting in a YoY decrease of 4.7 percentage points in the gross profit margin of the sanitary napkin business to 65.3% (1H2021: 70.0%).

Although the coronavirus epidemic broke out in many regions, with the re-emergence of the epidemic, the national health awareness has further improved, and the demand for tissue paper continued to be strong. Meanwhile, as small and medium-sized tissue paper companies cannot withstand the soaring costs which affect their business development, Hengan has gained more market shares leveraging its strong capital strength and nationwide sales network. Thus, the revenue of Hengan's tissue paper business increased substantially by close to 25.0% to RMB5,842.612mn (1H2021: RMB4,696.522mn), accounting for 52.2% of the overall revenue (1H2021: 47.1%). However, affected by the sharp surge in wood pulp prices due to the tight supply of wood pulp and logistical disruption. High wood pulp prices exerted enormous pressure on the Hengan's gross profit in 1H2022, and the gross profit margin dropped to approximately 23.1% (1H2021: 29.2%).

The sales of the Hengan's disposable diaper business rebounded, and the revenue increased by 2.2% to RMB633.513mn (1H2021: RMB619.668mn), accounting for 5.7% of the overall revenue (1H2021: 6.2%). As significant rise in the cost of sales caused by the price increase in petrochemical raw materials for disposable diapers during the period, but the increase in the proportion of sales of higher-margin ��Q • MO�� products offset part of the impact of rising costs on the overall business profitability. Thus, the gross profit margin of the disposable diapers business only dropped slightly to about 35.3% (1H2021: 36.2%).

Regarding other income and household products, the Hengan's revenue decreased by 2.0% YoY to RMB1595.372mn (1H2021: RMB1627.754mn), accounting for 14.2% of the overall revenue (1H2021: 16.3%). In which, medical products do not account for a significant portion of the overall revenue, but medical products have higher profit margin, which effectively increased the overall gross profit margin of other businesses by 7.2 percentage points to 20.4% (1H2021: 13.2%).

E-commerce channels maintained strong momentum

E-commerce channels (including Retail Integrated and New Channel) maintained a strong development momentum and the sales during the period soared over 30.0% to RMB2710.405mn (1H2021: RMB2004.757mn), accounting for 24.2% of the overall sales (1H2021: 20.1%). In which, other new sales channels (including online-to-offline (O2O) platform, community group-buying, etc.), with sales accounting for more than 10.0% of the overall sales. The tissue paper sales in e-commerce channel increased by more than 30.0%, accounting for more than 21.0% of the sales of tissue paper. Hengan's strived to strengthen the development of e-commerce and maternity sales channels. The proportion of sales of disposable diapers through e-commerce and maternity channels increased to more than 50.0% and more than 20.0%, respectively. The turnover of overseas channel (including Wang-Zhang Group business) was RMB1072.226mn (1H2021: RMB883.319mn), accounting for 9.6% of the overall sales (1H2021: 8.9%).

Investment Thesis

Since the overall operating environment was very challenging, and under the impact of lockdown and epidemic control measures, consumer sentiment in Mainland China became more cautious in the light of the epidemic. In addition, geopolitical upheavals affected the supply chain and exacerbated the rise in inflation, and given that the price of wood pulp is currently at a high level and the future trend is still uncertain, it is expected that the Hengan's gross profit margin will continue to be under pressure in 2H2022. However, part of the related downside and earnings risk may have already priced-in. Rising raw material prices and operating costs have brought enormous pressure to the industry, which accelerated market consolidation of eliminating the weak and retaining the strong. Meanwhile, Hengan's multi-channel sales development has certain advantages, upgraded products and premium product series can offset some of the impact of the spike in raw material prices, and the national health awareness has further improved, that Hengan's business still considered defensible and resilience to buck the trend. We expect FY2022E-FY2023E EPS to be RMB2.82 and RMB3.33 respectively, with PT of HKD37.90, implies a FY2022E P/E of 12.3x (~5-yrs historical average and one standard deviation below). Our investment rating is ��Accumulate��.

Risk factors

1) The price of raw materials continues to rise; 2) market competition intensifies; 3) channel development is not as expected; and 4) Sharp fluctuations in FX.

Financial

Click Here for PDF format...