Company Profile

After nearly 20 years of organic development and inorganic acquisitions, the Company has established a "dual engine" growth strategy driven by the application of lightweight metal materials in auto parts industry and the general aviation aircraft manufacturing industry, including six major business sectors, namely, 1) aluminum alloy wheels, 2), magnesium alloy automobile die castings, 3) high-strength steel stamping parts and other metal castings, 4) environmentally friendly dacromet coatings, and 5) general aviation aircraft. The Company is leading in many sub-industry fields.

Investment Summary

Cost Pressure Was Reduced and the Results Saw a Rebound from the Trough

Wanfeng Auto Wheels, based on the results report, recorded revenue of RMB11.7 billion in the first three quarters, up 37% yoy. The underlying reasons are the sufficient orders of the Company that kept mounting yoy, and the yoy increase in prices of main materials, as well as the optimization of the price and settlement mechanism. The net profit attributable to the parent company hit RMB590 million, up 152% yoy. The main reason is the improved profitability as yoy revenue growth outpaced cost increases, and the low base effect last year. In terms of profitability indicator, the gross margin and net profit margin in the first three quarters were 18.2% and 5.1%, up 2.2 and 2.3 ppts yoy, respectively. The return on net assets rose 5.6 ppts to 10.2% from a low of 4.6% last year. Additionally, the Company performed better than expected in controlling expenses. The period expense ratio dropped to a four-year low of 10.15%, down 2.21 ppts yoy..

Automobile Business Saw a Strong Rebound

With respect to business departments, the automobile metal parts lightweight business reported revenue of RMB10.215 billion, up 39.64% yoy. The profitability witnessed an overwhelming rebound, up 44.75% and 67.44% yoy in the automobile aluminium alloy wheel business and magnesium alloy die casting business, respectively.

Aided by the development dividend of the new-energy vehicle industry, the Company continued to consolidate the supply of magnesium alloy and aluminium alloy products in overseas OEMs. Meanwhile, the Company embarked on a broad path of the aluminium/magnesium alloy lightweight business in the new-energy vehicle industry chain and cooperated with mainstream new-energy vehicle companies such as BYD, Tesla, Rivian, NIO, Xiaopeng, Lixiang, Leapmotor, etc. While the Company's customer structure continued to be optimized, the products kept being innovative. With the rapid development of mainstream new energy car-making forces, the Company's supporting supply had also increased significantly. Sales volume of aluminium alloy wheels and magnesium alloy die-casting products for new-energy vehicles rocketed yoy. Furthermore, in the general trend of automobile lightweight, the amount of magnesium used in single vehicles gradually increased. The Company will continue to promote the construction of the Asia-pacific Centre for magnesium alloy business, thus further developing the business.

Aircraft Business Saw Steady Growth with Sufficient Orders

The general aviation aircraft manufacturing department, another major business, recorded revenue of RMB1.461 billion during the period, up 21.27% yoy with a steady business picture. The Company's general aviation aircraft manufacturing business is centred on innovative aircraft manufacturing, covering the business model of "R&D - authorisation/technology transfer - complete aircraft manufacturing and sales - after-sales service". During the reporting period, the general aviation aircraft manufacturing business had sufficient orders, and the sales business continued to be optimized. With the rising market share of Diamond Aircraft, the Company's after-sales service business had steadily improved. Meanwhile, the Company continuously developed and launched new high value-added models, such as the DA50, DA62 and the electric aircraft eDA40. As the general aviation market advances in the future, the Company's Diamond Aircraft will continue to develop new application scenarios on the basis of flight school training and other application markets. Through a wild range of aircraft models, domestic scenarios such as private flights, short-haul transportation, and specialized use will be further matched and developed. The domestic general aviation market, still in the early stage of development, enjoys a huge market..

Investment Thesis: Focus on the Follow-up Results Recovery

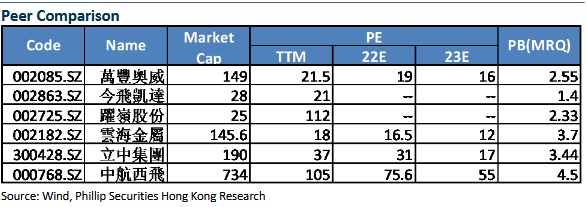

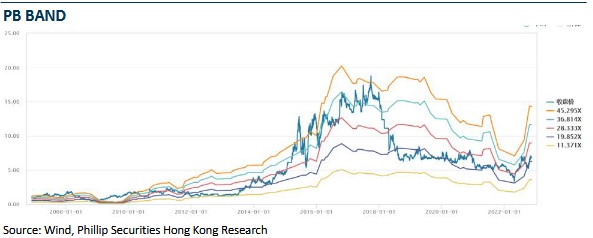

According to the latest financial data, we adjusted the EPS forecast for 2022 and 2023 to RMB 0.37/0.43, respectively (It was RMB0.29/0.43, respectively). We give the Company's target price to RMB 8.5, respectively 23/19.8/15 x P/E, 3.1/2.8/2.5 x P/B for 2022/2023/2024, a "BUY" rating. (Closing price as at 15 November)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...