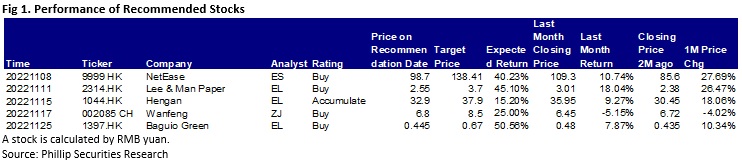

Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

TMT, Food (Elvis Kwok)

Automobile & Air (ZhangJing)

This month I released updated reports of Wanfeng (002085.CH).

Wanfeng Auto Wheels, based on the results report, recorded revenue of RMB11.7 billion in the first three quarters, up 37% yoy. The underlying reasons are the sufficient orders of the Company that kept mounting yoy, and the yoy increase in prices of main materials, as well as the optimization of the price and settlement mechanism. The net profit attributable to the parent company hit RMB590 million, up 152% yoy. The main reason is the improved profitability as yoy revenue growth outpaced cost increases, and the low base effect last year. In terms of profitability indicator, the gross margin and net profit margin in the first three quarters were 18.2% and 5.1%, up 2.2 and 2.3 ppts yoy, respectively. The return on net assets rose 5.6 ppts to 10.2% from a low of 4.6% last year. Additionally, the Company performed better than expected in controlling expenses. The period expense ratio dropped to a four-year low of 10.15%, down 2.21 ppts yoy.

With respect to business departments, the automobile metal parts lightweight business reported revenue of RMB10.215 billion, up 39.64% yoy. The profitability witnessed an overwhelming rebound, up 44.75% and 67.44% yoy in the automobile aluminium alloy wheel business and magnesium alloy die casting business, respectively. Aided by the development dividend of the new-energy vehicle industry, the Company continued to consolidate the supply of magnesium alloy and aluminium alloy products in overseas OEMs. Meanwhile, the Company embarked on a broad path of the aluminium/magnesium alloy lightweight business in the new-energy vehicle industry chain and cooperated with mainstream new-energy vehicle companies such as BYD, Tesla, Rivian, NIO, Xiaopeng, Lixiang, Leapmotor, etc. While the Company's customer structure continued to be optimized, the products kept being innovative. With the rapid development of mainstream new energy car-making forces, the Company's supporting supply had also increased significantly. Sales volume of aluminium alloy wheels and magnesium alloy die-casting products for new-energy vehicles rocketed yoy. Furthermore, in the general trend of automobile lightweight, the amount of magnesium used in single vehicles gradually increased. The Company will continue to promote the construction of the Asia-pacific Centre for magnesium alloy business, thus further developing the business.

The general aviation aircraft manufacturing department, another major business, recorded revenue of RMB1.461 billion during the period, up 21.27% yoy with a steady business picture. As the general aviation market advances in the future, the Company's Diamond Aircraft will continue to develop new application scenarios on the basis of flight school training and other application markets. Through a wild range of aircraft models, domestic scenarios such as private flights, short-haul transportation, and specialized use will be further matched and developed. The domestic general aviation market, still in the early stage of development, enjoys a huge market.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released 3 reports of Lee & Man Paper Manufacturing(2314.HK), Hengan(1044.HK) & Baguio Green(1397.HK).

LMP total revenue for the six months ended 30 June 2022 (1H2022) increased by 0.6% YoY to HK$15.3bn. Net profit attributable to shareholders decreased by 58.8% to HK$797mn, which is consistent with the results announced in July. The EPS was HK18.46 cents (1H2021: HK44.54 cents). Interim dividend of HK6.50 cents per share (1H2021: HK15 cents), decreased by 56.7% YoY.

During the period, mainland paper manufacturers` profitability has been under pressure as a result of rising prices of raw materials such as wood pulp, energy, and high logistics and transportation costs, plus lockdown of cities amid the pandemic leading to weakened demand. The aggregate sales amounted decreased by 3.9% YoY to 2.96 million tons, with net profit per ton decreased by HK$358 to HK$292. The overall gross profit plunged 50.4% to $1.656bn, while the overall gross profit margin fell 11.1ppt to 10.8% due to the significant increase in raw material prices. In terms of expenses, 1H2022 distribution and selling expenses were HK$446mn, down 11.5% YoY, accounting for 2.9% of total revenue; General and administrative expenses were HK$598mn, down 17.4% YoY, accounting for 3.9% of total revenue.

By segments, the packaging paper segment's profit dropped 72.4% YoY to HK$610mn, while segment's revenue rose slightly by 0.6% YoY to HK$13.051bn, accounting for 85.4% of the total revenue. The tissue paper business segment's profit increased 24.8% YoY to HK$286mn, while segment's revenue declined 0.3% to HK$2003mn, accounting for 13.2% of total revenue. The pulp segment's profit rose 19.9 times YoY to HK$60.22mn and segment's revenue rose 16.1% to HK$216mn, accounting for 1.4% of total revenue.

Looking ahead, China continues to tighten control over plastic packaging, giving room for using paper packaging as a substitute, while consumption behavior has changed amid the pandemic with more people shopping online, and correspondingly the demand for packaging paper has climbed. LMP continued to consolidate upstream resources and develop a vertical business model covering pulp-making and waste paper recycling, and plans to add pulp production lines at its plants in Jiangxi province and Chongqing, so as to enhance raw materials supply (the new production lines are expected to start operation in 2023). Regarding tissue paper business, LMP plans to establish a new plant in Guangxi province and expects to add new production line with annual capacity of 300,000 tons of bleached pulp by the end of next year at the earliest (total production capacity is around 1,000,000 tons). LMP is actively expanding its recycled pulp business and enhancing raw material deployment, which should be expected to mitigate the impact of rising raw material costs on profits in the long run. With the gradual easing of the pandemic in June, overall domestic consumer confidence is sluggish and we remain cautious about the degree of business recovery in the second half of the year (Q4 will be the traditional peak demand season), but the low valuation level to some extent reflects the company's weak fundamentals.

TMT, Food (Elvis Kwok)

This month I released one report, NetEase (9999.HK).

NetEase (9999.HK) is a leading internet and technology company in China. Its main business includes gaming and related value-added services. The company develop and operate a variety of popular and enduring mobile and PC games in China. Besides, NetEase's other businesses include: (2) its subsidiaries Youdao (NYSE: DAO), mainly provide technology-based intelligent learning services and products. (3) its subsidiaries NetEase Cloud Music (9899.HK), mainly provide online music service and rich music community experience. (4) its innovative businesses and others, for example the self-operated lifestyle brand NetEase Yanxuan.

NetEase (9999.HK) has announced the operating data from Mar to June 2022. NetEase (9999.HK) revenues amounted to RMB 23,159.1 million, representing an increase of 12.8% YoY, but a decrease of 1.7% QoQ. Gross profit amounted to RMB 12941.5 million, representing an increase of 15.7% YoY, and an increase of 0.82% QoQ.

Game business features

NetEase owns many popular and profitable games, it can be divided into two markets, China gaming market and overseas gaming market (some popular games are successful in both markets).

In China gaming market

The series of Westward Journey include Fantasy Westward Journey Online, etc. In 2004, the PC version was officially operated for a fee and the mobile version was launched in 2015. As the “Evergreen Tree” of NetEase, Westward Journey has brought NetEase a stable and substantial income. On the mobile version, according to the data survey agency Sensor Tower (the data does not include third-party Android platforms in China and other places, the same below), Fantasy Westward Journey online ranked 7th in global mobile game revenue and ranked 3rd in China in July. It is a pity that the theme of “Westward Journey” has not been able to enter the overseas market for many years, and it only developed in China.

In overseas gaming market

Naraka: Bladepoint is a martial arts-style action-adventure battle royale game. It only has a PC version for the time being, and the mobile version is still in the development stage. the global sales of Naraka: Bladepoint exceeded 10 million In June 2022, becoming the first domestic buyout game with global sales exceeding 10 million, and 50% of them came from overseas markets. Besides, Diablo: Immortal is a massive online multiplayer action role-playing game jointly launched by NetEase and the global game giant Blizzard Entertainment on June 2, 2022. The Chinese server was released on July 25, and it was launched on both PC and mobile platforms.

The series of Diablo launched by Blizzard in December 1996, and the series has sold more than 24 million worldwide. It is deeply concerned and loved by players around the world. According to Sensor Tower, after Diablo: Immortal released, the mobile version of this game ranked 8th July globally. Since the China server was launched on July 25, the data did not fully reflect the explosiveness and profitability of the game. In addition, the mobile version of this game took only 8 weeks to reach USD 100 million in revenue, making it the second fastest mobile game in the world, only two weeks longer than Pokemon Go.

Positive factors

1. Developing overseas gaming market to drive revenue growth

In recent years, NetEase has actively explored the overseas gaming market. The CEO Ding Lei said that his company 80% of R&D resources are invested in China currently, the overseas market only takes over 10%, but it will expand to 40% to 50% in the future. In Japan market, Onmyoji, Knives Out and Identity V, etc. have successively entered the Japanese mobile game market, NetEase builds their reputation and image among Japanese players. Investors can expect more games will be popular and profitable in Japan in the future. In addition, the Diablo: Immortal jointly launched by NetEase and Blizzard swept the world, however the interim report did not reflect the profit that created by Diablo: Immortal in time. Investors can expect this game to be a catalyst for NetEase's revenue and stock price, but investors need to keep observing the game sustainability.

2. Expert in games localization to increase game competitiveness and longevity

NetEase is good at localizing games to integrate and enter the local market. For example, when the Identity V entered the Japanese market, it did not attract much attention. Later, it attracted Japanese players to try it through the cooperation with Junji Ito, a well-known Japanese horror cartoonist, and then became famous. NetEase's strategy attracts players by cooperating with other famous cultural works. It can achieve the purpose of increasing the competitiveness and longevity of the game, and it also proves that this strategy can bring freshness to players and attract new players.

3. New games are expected to improve profitability

Besides the popular game Diablo Immortal, the trendy casual competitive game Egg Go launched in May also caused a boom in China. According to Sensor Tower, the game was downloaded 2 million in China in August, and it was most downloaded game by NetEase in August. Investors can expect this game to monetize and increase profitability while stabilizing player enthusiasm. In addition, NetEase is preparing to launch mobile version of popular PC games like Naraka: Bladepoint, Justice and Ghost World Chronicle. It also expected to boost the company's revenue from mobile gaming platforms.

Click Here for PDF format...