Overview

XD.Inc (2400.HK) is a game developer, operator and publisher in China, its main business is game operating and information services. Gaming operating include online games and premium games, its revenue mainly come from the sales of virtual items of online games and revenue generated from premium games by third parties and self-owned distribution platforms. Information service's revenue mainly comes from the income generated when the player interactive community and game recommendation platform TapTap provide online promotion services. As of June 30, 2022, the company current titles portfolio included 20 online games and 22 premium games.

A review of Q2 2022 Results

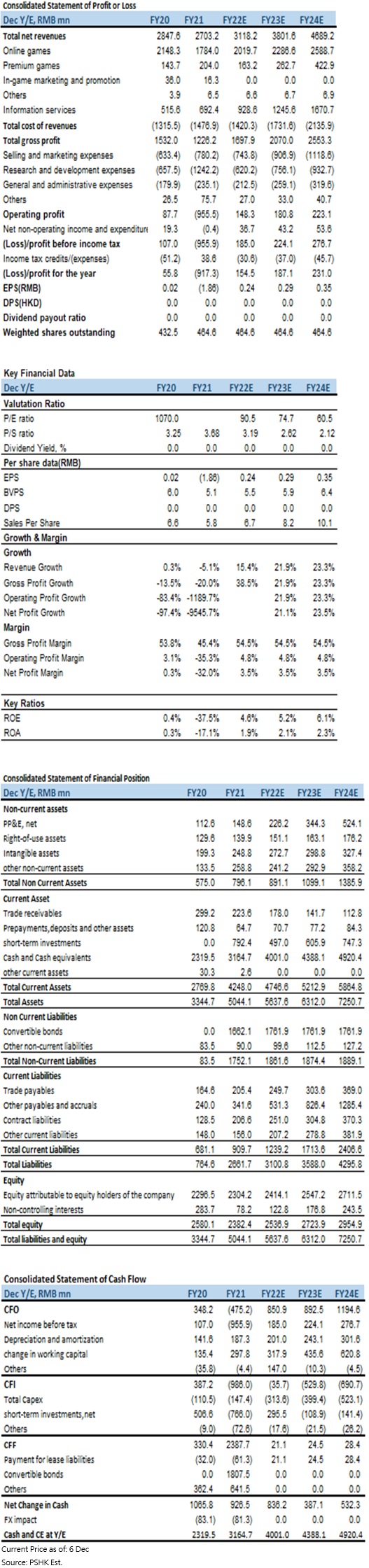

XD.Inc (2400.HK) has announced the interim report ended June 30 2022. The company's revenue amounted to RMB 1594.0 million, representing an increase of 15.6% YoY. Gross profit amounted to RMB 782.9 million, representing an increase of 15.7%. Gross profit margin was 49.1%, roughly flat YoY. The loss for the period was RMB 381.4 million, representing an increase of 18.3% YoY.

Gaming operating:

Online games net revenue amounted to RMB 1042.1 million, representing an increase 10.9% YoY, primarily due to increases in revenue from Sausage Man, and was partially offset by the decreases of revenue from certain existing games under maturity stage, such as Ragnarok M and Ulala.

Premium games net revenue amounted to RMB 72.6 million, representing a decrease of 18% YoY, primarily due to decreases in revenue from certain existing premium games.

Cost of revenues for game business amounted to RMB 674.3 million, representing an increase of 6%. Besides, gross profit margin was 40.1%, representing an increase of 1.1% YoY, primarily due to an increase of RMB 106.7 million in sharing of proceeds to game developers, which was mainly attributable to the increase of revenue from Sausage Man.

Information services:

Information services net revenue amounted to RMB 467.8 million, representing an increase of 39.3% YoY, primarily due to the growth of the average app MAUs of TapTap PRC, which increased by 45.5% to RMB 41.7 million. Besides, the company also started to generate subscription revenue from TapTap Cloud Gaming service in the first half 2022, though not much. As for the international version of TapTap, it is not monetized.

Cost of revenues for information service business amounted to RMB 136.9 million, representing an increase of 107.7% YoY. Besides, gross profit margin was 70.7%, representing a decrease of 9.7% YoY, primarily due to the growths in the average mobile app MAUs and gamers` activities in TapTap PRC, and the exploration and expansion of a few new businesses such as TDS, TapTap Cloud Gaming and international operations, lead bandwidth and servers` custody fee and employee benefits expenses of TapTap's operation staff.

Game business features

Many of the company's popular games are listed in many regions around the world, not limited to the mainland market. In terms of revenue contribution in the first half of 2022, the company's top five titles are Sausage Man, Ragnarok M, Ulala, Lan Yan Qing Meng and Shen Xian Dao(HD).

Online games business

For the online game business, the average MAUs fell by 2.2% YoY, and average MPUs grew by 88.7% YoY. The MAUs drop because old games like Ragnarok M's MAUs fell YoY, the decline was partially offset by an increase in average MAUs for Sausage Man. In addition, the average MPUs grew because Sausage Man's payment rate significant increase YoY.

1. XD.Inc most popular game is Sausage Man, it is a tactical competitive game, the gameplay is mainly based on battle royale with shooting, which is similar to PUBG M. The game launched in China in April 2018, the game still maintains vigorous vitality and potential for further growth. In the first half of 2022, the number of active users and payment rate of the game hit new highs repeatedly, making its turnover performance significantly increase YoY. In addition, the game was launched in Japan, Hong Kong, Macao, Taiwan, and South Korea in the second quarter of this year, initially establishing a user base in overseas markets, and the number of global downloads exceeded 300 million. According to the data survey agency Sensor Tower (the data does not include third-party Android platforms in China or other places, the same below), the game had 300k downloads and $900k USD in revenue on the mainland in October this year, and 90k downloads and $200k USD revenue on the overseas in October this year. Moreover, the cumulative downloads of the game on TapTap PRC are approximately 188 million, and the cumulative downloads of the TapTap International are approximately 9.4 million.

2. Ragnarok M is a MMORPG, it launched in China in January 2017, and has since been launched in many countries and regions around the world. The game is currently in a maturity stage (the number of game users and revenue has reached a high point and gradually declined), and the revenue has declined to a certain extent YoY. According to Sensor Tower, the game had 7k downloads and $600k USD in revenue in October this year.

3. Ulala is a team placement mobile game set in the Stone Age, it launched in Taiwan in May 2019, and then launched in many countries and regions around the world. The game is currently in a maturity stage and the revenue has declined to a certain extent YoY. According to Sensor Tower, the game had 10k downloads and $500k USD in revenue this October.

4. Shen Xian Dao(HD) is a horizontal turn-based game with the theme of Xianxia. It launched in March 2016; it mainly operates in Mainland China. According to Sensor Tower, the game had less than 5k downloads in October this year and earned $400k USD.

5. Torchlight: Infinite is an action RPG; the gameplay is similar to the global popular game series “Diablo”. The game launched in October 2022; it is a relatively popular new game under XD.Inc. The interim results did not include the income of this game. Besides, the game is currently only available on Asian servers, European servers, and American servers, and has not obtained a game license in China. According to Sensor Tower, the game had 600k downloads and $1 million USD in revenue in October this year, which is the most downloads and most revenues game in October this year. In addition, TapTap International is the exclusive distribution platform for this game on the Android. The cumulative downloads of the game on the TapTap International are about 360k. For a game that has only been launched for a month and still has growth potential, the number of downloads and revenue of the game are doing well. Moreover, David Breivik joined the development team as a consultant. He is one of the founders of Blizzard North (formerly a studio under Blizzard Entertainment) that produced the global popular game series “Diablo”. Investors can expect him to use his expertise and understanding of this type of game to help the game grow even better. Also, if the game gets the game license and launch in China, we believe it will benefit the company's revenue growth.

6. T3 Arena is a 3v3 multi-hero shooting game, launched in May 2022, and it is one of the popular games under XD.Inc. The interim report did not fully account for the revenue of this game. After the game was launched in May this year, it was recommended by the Apple Store in 171 countries and regions and won the top spot in the free list of 11 Apple Stores. Since the game has not obtained a game license in China, it is currently mainly developed in overseas markets, such as the United States, Japan and South Korea. According to Sensor Tower, the game had 500k downloads and $500k USD in revenue this October. In addition, TapTap International is the exclusive distribution platform for this game on the Android, and its accumulated downloads are about 1.5 million. If the game gets a game license in China, we expect it will benefit the company's revenue growth.

7. Flash Party is an action fighting game, the gameplay is similar to Super Smash Bros owned by Japanese game giant Nintendo. The game launched in February 2022, it mainly developed in Japan market and launched in China in April. When the game was first launched in Japan, it won the top spot in the free list of the Japanese Apple Store for 12 consecutive days. According to Sensor Tower, the game had 50k downloads and $30k USD in revenue for the China market with 30k downloads and $30k USD for the international market in October. In addition, TapTap International is the exclusive distribution platform for Flash Party, and the accumulated downloads of this game in this platform are about 1.43 million. However, the overall data reflects that the popularity of the game is fading faster.

Premium games business

The company's premium games are in the transition period of preparing for the launch of new key games, and the overall revenue has declined. The company launched Otaku's Adventure and Evoland 2 in the first half of 2022 performed mediocre. On the other hand, Terraria, Human: Fall Flat and Sands of Salzaar performed relatively well.

8. Terraria is a 2D sandbox simulation game developed by Re-Logic in 2011. Sandbox simulation games generally require players to take survival as the primary goal, and then explore and build the world. The game is famous for its high degree of freedom. XD Inc is representing the mobile version in China. The China server launched on September 28 ,2021 and the cumulate downloads of the TapTap PRC are about 2.97 million. According to Sensor Tower, the game had 30k downloads and $50k USD in revenue in October of this year.

9. Human: Fall Flat is a multiplayer electronic puzzle games, developed by No Brakes Games, XD.Inc is representing the mobile version in China. The game was launched on December 17, 2020. On the day of release, it recorded 100k downloads in 20 minutes, 500k in 12 hours, and nearly one million downloads on Apple and Android platform a day. The game has accumulated about 2.7 million downloads on the TapTap PRC. According to Sensor Tower, the game had 20k downloads and $70k USD in revenue in October this year. This game is very entertaining, and it is very suitable for stream. It has also caused an upsurge in the world, but it is a pity that XD.Inc is only representing the game in China, the revenue is limited in China and the revenue needs to be shared with the developer.

10. Sands of Salzaar is an open-world action role-playing game, represented by XD.Inc and developed by HanJia Squirrel Studio, which focuses on martial arts and is popular among domestic players. There are both mobile and PC versions of the game, and the sales volume on all platforms exceeds 1.5 million. According to Sensor Tower, the game had 5k downloads and $20k USD in revenue in October of this year.

Information services business

The company owns TapTap, a well-known mobile game platform in China, and has focused on developing TapTap International in recent years to enter overseas markets. For the six months ended June 30, 2022, the average MAUs of the TapTap PRC were approximately 41.7 million, representing an increase of 45.5% YoY. The number of game downloads was 402.3 million, representing an increase of 62.2% YoY The number of new posts was 4.3 million posts, representing an increase of 43.9%. Benefiting from a series of upgrades of TapTap's architecture and in-app experiences since 2021 and in-depth engagement of machine learning technology, the efficiency of TapTap's game distribution and ads system had been improved significantly.

The average MAUs of TapTap International were approximately 9 million, representing a decrease of 31.9% YoY. It is mainly due to the impact of individual popular games and the overseas epidemic that TapTap International grow rapidly in 2021, while the user data has declined this year. The company preliminarily built up a team focusing on the international market and dedicated to the development and operation of versions specifically for certain key overseas markets. The team targets to build up the community ambiance and increase the user penetration rate of the target markets.

TapTap mainly provide three services, including online marketing service, developer service (TDS) and Cloud Gaming service.

In term of online promotion services, the platform includes download channels, game information, reviews and recommendations for a variety of domestic and overseas mobile games, and also provides discussion forums for users to communicate to earn advertising revenue.

In term of developer service (TDS), it mainly provides developers with a variety function to reduce the difficulty and cost of developing mobile games. It also allows developers to communicate directly with players to understand players` taste, then promote and publicize new games during the game development stage. For example, the platform has data analysis tools that can help developers better understand user orientation and deploy advertisements. In addition, the platform has built-in anti-addiction systems such as real-name system, so game developers do not need to create additional systems to comply with China's regulations. Currently, this business adopts a free or cost-based pricing model for third-party developers.

In term of Cloud Gaming service, users can play a series of mobile games provided by TapTap through a monthly subscription service, but the current income is not significant. This business mainly takes care of low-end mobile phone users in China. The technical feature of this business require XD.Inc to prepare a large number of equipment and servers for players to connect. When players use this service, the server will run the game for the player and send it to the player's mobile phone in real time for the player to operate, so the game will not be stored in the user's mobile phone. Also, it does not need to use too much mobile phone performance when playing. So, it is suitable for some players whose mobile phone have poor performance or lack storage. For example, miHoYo's Genshin Impact requires a mobile phone with better performance and large storage to run the game smoothly. In addition, players can try various games without downloads.

Positive factors

1. TapTap creates a unique advantage

TapTap is a well-known mobile game forum in China. It has been established for about 5 years. Compared with similar platforms in China such as WeGame under Tencent, it was established earlier. It has good user stickiness and first-mover advantage. Until now, TapTap has a large number of users, and the number continues to grow, bringing good advertising revenue to the company, and the development is optimistic. In addition, TapTap enables XD Inc's games to be better disseminated through its own platform, which can effectively reduce game promotion costs, and the exclusive launch of XD Inc's games on the platform also makes players stick to the platform, so TapTap and XD's games are mutually beneficial. However, investors need to pay attention to the development of the TapTap International. The TapTap International is different from the TapTap PRC and needs to face competition from international game platforms, such as IGN, an internationally renowned multimedia review platform, etc. Compared with the TapTap International, these international platforms have a very good reputation and high popularity. In comparison, TapTap International has no advantage in competition, so XD.Inc needs to put more in the TapTap International for marketing and promotion. However, if the TapTap International is stabilized in overseas markets, then user stickiness is cultivated and the number of users resumes growth, it will be beneficial for XD.Inc and other Chinese game companies to promote their games through the TapTap International, then they will be easier to enter overseas markets.

2. Stable through the downturn of popular games

XD Inc.'s popular games such as Ragnarok M, Ulala and Shen Xian Dao(HD) have entered to maturity stage, and the popularity of the newly launched Flash Party has also declined relatively quick. Meanwhile, premium games business is in the transition period of preparing for the launch of new key games. Among the games, only Sausage Man performed well in the interim report. Investors may worry about the slowdown in overall gaming business revenue. However, T3 Arena and Torchlight: Infinite have been launched recently and performed well in overseas markets. It is expected to bring new growth momentum to XD Inc's online game business, and if it can obtain game license in China, we believe that both games will be loved by Chinese players, and the profit potential is huge. As for premium games, due to the lack of new games that perform well, this part of revenue is expected to still decline in FY2022.

Risk factors

1. Cost control become difficult

The cost of new business Cloud gaming services is too high

Since the operation of the TapTap Cloud Gaming services require a large number of devices, servers and a smooth and stable network, which will consume a lot of server computing costs and bandwidth costs. In fact, XD. Inc pay tens of millions for TapTap Cloud Gaming in 11 months of free operation in 2021. Afterwards, TapTap Cloud Gaming service opened the charging model and reduced the number of free hours given to players daily to reduce losses. However, the official admitted that it is difficult to recover the cost by charging alone. In the 2022 interim results, the bandwidth and server custody fee amounted to RMB 177.5 million, representing an increase of 63.3% YoY, 21.9% of the total cost. This cost was mainly attributed to the growths in the average mobile app MAUs and gamers` activities in TapTap PRC, and the exploration and expansion of a few new businesses such as TDS, TapTap Cloud Gaming and international operations. We believe that the cost of TapTap Cloud Gaming is too high, and it is difficult to pass it on to consumers, because the target customers of TapTap Cloud Gaming are mainly domestic players who use low-end mobile phones, and these players may not have high spending power and are more sensitive to prices. In addition, to the competition from the same industry, for example, the NetEase Cloud Gaming platform also provides similar services with similar prices. We believe that there is little room for an increase in fees for this new business, and there is no way to control costs for the time being.

2. Rising cost of R&D, sales and marketing expenses

XD. Inc has a lot of experience in entering the overseas game market and it is an advantage over ordinary game companies. However, players in the United States, Japan, South Korea, and Europe are accustomed to play high-quality games, such as paying attention to gameplay and CG art styles, etc. So, XD Inc. has high requirements for the quality of games, but XD Inc. self-development ability is not good enough, for example, XD Inc.'s three popular premium games are not developed by themselves. Moreover, in the first half of 2022, the research and development of 4 small-scale or unsatisfactory game projects were successively terminated, and 233 employees engaged in game research and development were fired to reduce costs and increase efficiency. We are worried that the company cannot strike a balance between controlling costs and launching high-quality games.

XD Inc's premium game business is in the transition period of preparing for the launch of new key games, and there is no clear launch timetable for new key games. Among the three premium games newly launched in the first half of 2022, including Sands of Salzaar, Otaku's Adventure and Evoland 2, only Sands of Salzaar performed relatively well. But XD Inc. is only the proxy, revenues created by this game needs to be shared with the developer. Coupled with the gradually decline in the popularity of old premium games, it is expected that the revenue of premium games will continue to drop in 2022. Investors need to pay attention to the development and income of follow-up premium games.

3. Policy risks from China

Policy risks can be divided into two categories, include the restriction of teenager's online game time policy and the game license approval policy. In term of restriction of teenager's online game time policy, Chinese teenagers who under 18 years old are only allowed to play games for up to 3 hours a week, and only on weekends and festivals. Although teenagers have low spending power and they only make little impact on game revenue, teenagers are difficult to enjoy playing games under the restriction policy, it will have a negative impact on building players community and user stickiness, eventually reduce the game's lifespan and potential revenue.

In term of the game license approval policy, relevant Chinese authorities are stricter with game license approvals. In recent years, the approval of game license has been stopped twice, it affects the business development and revenue plans of game companies. Although relevant department re-approve game licenses and there are signs of normalization, the relevant departments tend to approve those game licenses from small-sized companies. As for XD Inc., three game licenses have been approved since relevant Chinese authorities reapproval in April, if XD Inc's game license get approved regularly, it may become a catalyst for the stock price to rise.

Valuation and recommendation

We believe that the Chinese gaming market is currently at the end of the restructuring period. In order to adapt the changes of China policies and reduce policy risks, Chinese game companies are accelerating their development in overseas markets, including the acquisition of overseas game studios, etc. This act will lead the whole industry operating costs increase. However, XD Inc. has sufficient experience in overseas game markets. Many games are popular in different regions. In addition, T3 Arena and Torchlight: Infinite which launched this year performed well in overseas markets. Besides, TapTap has a huge user base in China, and it can be mutually beneficial with its own games, giving XD.Inc a unique advantage. Moreover, recent China official media published comments that reaffirmed the economic contribution of the game industry, which is quite different from previous views. Investors can look forward to the end of the winter in the game industry, and investors can be a little more optimistic about the industry. We expect XD.Inc net profit growth are N/A, 21.1% and 23.5% in FY2022-2024 respectively. Net sales per share attributable to shareholders are RMB 6.7, 8.2 and 10.1 in FY2022-2024 respectively. Corresponding P/S ratio are 3.19/2.62/2.12x. We believe that although the launch time of key premium games is doubtful, which will negatively affect business growth, the company's newly launched online games are performing well. In addition, the user growth of the TapTap PRC continues, and the TapTap International is also expected to bring new growth momentum to the company. We give XD.Inc 3x P/S in FY2023 and a target price of $27.31 HKD. (Calculated at the exchange rate of RMB to HKD 1.11), with a "buy" rating. (Current price as of December 6)

Financial

Click Here for PDF format...