Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

TMT, Food(Elvis Kwok)

Automobile & Air (ZhangJing)

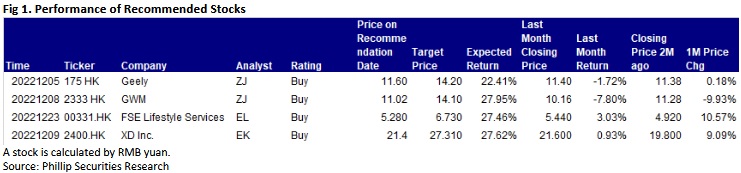

This month I released updated reports of Geely (175.HK) and Great Wall Motors (2333.HK).

According to the released sales data for October, Geely Auto reported total sales volume of 152,263 units, a significant increase of 36.4% yoy and a substantial growth of 16.65% mom. In terms of sub-brands, Geely reported sales volume of 119,874 units, a significant increase of 34% yoy and a growth of 18% mom. Among its higher-end models, the sales volume of "China Star" series (Xingyue, Xingyue L, and Xingrui) reached 30,033 units, up 32% mom. In term of the specific models, the sales volume of both Xingrui and Xingyue L was over 10 thousand units, the sales volume of the Emgrand family outstripped 20 thousand units, and that of the Bin family (Binyue and Binrui) exceeded 30 thousand units.

During October, GeelyEmgrand L Hi.P, which is equipped with the Leishen Power, and Xingyue L Hi.P, as well as the Haoyue L, a new model on the CV platform, and the Boyue L, a brand-new model on the CMA platform, joined the product lineup of Geely in succession, with reservations opened. It is worth noting that the order of Boyue L exceeded 26,000 units on October 26, the first day of the launch, and its sales volume outstripped 8,000 units in the first month of the launch, with eye-catching performance, showing the initial potential as a top-selling model.

In October, the sales volume of Lynk& Co was 16,439 units, a slight growth of 1.6% mom and a decrease of 24.27% yoy. Lynk& Co has newly launched the Lynk& Co 03, the Lynk& Co 03 EM-F, an intelligent electric hybrid model, and the Lynk& Co 09EM-P Voyage Edition. The replacement and upgrading of Lynk& Co is also in progress.The sales volume of Geometry, a battery electric vehicle brand, reached 12.6 thousand units, up 116% yoy and down 32.6% mom, mainly due to the upcoming launch of the more intelligent new models of G6 and M6. The sales volume of Ruilan, a battery replacement brand, was 5,831 units, up 28.4% mom.The sales volume of Zeekr, a high-end battery electric vehicle brand, reached 10,119 units relying on the Zeekr 001, exceeding 10 thousand units for the first time, up 22.3% mom. Since its launch, it has delivered 55.6 thousand units accumulatively, verifying the product strength in the fierce competition with new car-making forces. The Zeekr 009, a new battery electric luxury MPV with six seats, was officially released in November, cutting into the segment of domestic high-end intelligent electric MPV. It will further enrich the product matrix of Zeekr and facilitate the promotion of the strategy of high-end branding.

Recently, the Company announced its intention to spin off Zeekr for a separate listing. The valuation of Zeekr was close to RMB60 billion in the previous pre-IPO financing. If it is successfully spun off for listing, it will help Zeekr obtain more resources to seize market opportunities and realize a two-wheel ecosystem driven by industry and capital, which will also be conducive to the value revaluation of the parent company.

Great Wall Motors reported a sales volume of 100.2 thousand units in October, down 11% yoy and up 7% mom. The year-on-year decline was mainly due to the disruption of demand of major automobile consuming provinces amid the spread of the pandemic in multiple places. However, Great Wall Motors displayed outstanding performance in the overseas sales in October. A total of 21,052 units were delivered, up 50% yoy and up 12% mom, accounting for 21% of the total sale volume. In 2022, due to the disruption resulting from the pandemic, the Company's original strong product cycle has been delayed. However, with the gradual disappearance of the negative factors, the recovery of capacity utilisation and the launch of a series of new models are expected to bring elasticity to the revenue and net profit. We think that Great Wall Motors` long-term layout of new technologies and new product systems will facilitate its share rally and bring returns in the future.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released the report of FSE Lifestyle Services (331.HK).

FSE Lifestyle Services (“FSE”) are a lifestyle services conglomerate with 3 major business segments: property & facility management services, city essential services and E&M services.

In FY2022 (for the year ended 30 June 2022), FSE's recorded revenue amounting to HK$6,966.9mn, representing an increase of HK$514.2mn or 8.0%, as compared with HK$6,452.7mn in FY2021. Profit attributable to shareholders was HK$502.9mn, representing a decrease of HK$84.0mn or 14.3% as compared with HK$586.9mn in FY2021, mainly resulted from a decrease in government grants. If excluding the effects of government grants, adjusted net profit for the FY2022 of 35.2% to HK$414.7mn (i.e. after excluding government grants of HK$88.2mn from profit attributable to shareholders of the Company of HK$502.9mn for the Year) as compared to adjusted net profit of HK$306.8mn for FY2021. Basic EPS was HK$1.10, a decrease of 14.7% YoY. The total dividends for 2022 was HK45.0 cents (2021: HK45.0 cents) per share, the dividend payout ratio is 41.0% (calculated based on the adjusted profit), while the dividend payout ratio was 48.7%, calculated based on the adjusted profit for the year ended 30 June 2021.

The gross profit decreased by HK$142.6mn or 12.6% to HK$992.5mn from HK$1,135.1mn in FY2021, with an overall gross profit margin decreased to 14.2% from 17.6%, mainly reflecting a decrease in COVID-19 related government grants. If excluding the effects of these grants, adjusted gross profit margin increased to 13.6% from 12.8% last year, mainly caused by an improvement in the gross profit margin of the E&M services segment.

As of 30 June 2022, the property & facility management services segment has a total gross value of contract sum of HK$2,074mn with total outstanding contract sum of HK$1,162mn; the city essential services segment has a total gross value of contract sum of HK$7,643mn with a total outstanding contract sum of HK$4,415mn; the E&M services segment has a total gross value of contract sum of HK$9,009mn with a total outstanding contract sum of HK$5,085mn. The total gross value of contract sum of the above-mentioned is HK$18,730mn, and the total outstanding contracts sum of HK$10,660mn. With the sufficient reserve of outstanding contracts project, future revenue growth would be guaranteed.

After completing multiple acquisitions in the past, including property and facility management services, the overall business scale of FSE has been significantly expanded. Further to the strong synergies generated among business units within the group, it has also maximized cost-effectiveness and operational efficiency at all times. With the increasing expectation of the corporate clients and property investors, there is a growing demand of enhanced services and one-stop solutions in professional property and facility management services. FSE's compound annual growth rate (CAGR) of revenue and profit from FY2017 to FY2022 reached 14% and 24%, respectively. Upon the government policy on increasing the supplies of residential units by the coming 10 years, the increasing supply of both private and public housing units, hence, creates a growing demand and necessities of professional property management services in the territory, which is expected to bring huge market opportunities to FSE.

�TMT, Food (Elvis Kwok)

This month I released one report, XD Inc. (2400.HK).

XD.Inc (2400.HK) is a game developer, operator and publisher in China, its main business is game operating and information services. Gaming operating include online games and premium games, its revenue mainly come from the sales of virtual items of online games and revenue generated from premium games by third parties and self-owned distribution platforms. Information service's revenue mainly comes from the income generated when the player interactive community and game recommendation platform TapTap provide online promotion services.

XD.Inc (2400.HK) has announced the interim report ended June 30 2022. The company's revenue amounted to RMB 1594.0 million, representing an increase of 15.6% YoY. Gross profit amounted to RMB 782.9 million, representing an increase of 15.7%. Gross profit margin was 49.1%, roughly flat YoY. The loss for the period was RMB 381.4 million, representing an increase of 18.3% YoY.

For the online game business, the average MAUs fell by 2.2% YoY, and average MPUs grew by 88.7% YoY. The MAUs drop because old games like Ragnarok M's MAUs fell YoY, the decline was partially offset by an increase in average MAUs for Sausage Man. In addition, the average MPUs grew because Sausage Man's payment rate significant increase YoY.

For the premium game business, the company's premium games are in the transition period of preparing for the launch of new key games, and the overall revenue has declined. The company launched Otaku's Adventure and Evoland 2 in the first half of 2022 performed mediocre. On the other hand, Terraria, Human: Fall Flat and Sands of Salzaar performed relatively well.

For the information services business, the company owns TapTap, a well-known mobile game platform in China, and has focused on developing TapTap International in recent years to enter overseas markets. For the six months ended June 30, 2022, the average MAUs of the TapTap PRC were approximately 41.7 million, representing an increase of 45.5% YoY. The number of game downloads was 402.3 million, representing an increase of 62.2% YoY The number of new posts was 4.3 million posts, representing an increase of 43.9%. Benefiting from a series of upgrades of TapTap's architecture and in-app experiences since 2021 and in-depth engagement of machine learning technology, the efficiency of TapTap's game distribution and ads system had been improved significantly.

We believe that the Chinese gaming market is currently at the end of the restructuring period. In order to adapt the changes of China policies and reduce policy risks, Chinese game companies are accelerating their development in overseas markets, including the acquisition of overseas game studios, etc. This act will lead the whole industry operating costs increase. However, XD Inc. has sufficient experience in overseas game markets. Many games are popular in different regions. In addition, T3 Arena and Torchlight: Infinite which launched this year performed well in overseas markets. Besides, TapTap has a huge user base in China, and it can be mutually beneficial with its own games, giving XD.Inc a unique advantage. Moreover, recent China official media published comments that reaffirmed the economic contribution of the game industry, which is quite different from previous views. Investors can look forward to the end of the winter in the game industry, and investors can be a little more optimistic about the industry.

Click Here for PDF format...