Investment Summary

Continuing the Strong Sales Momentum, the Company Reaches the Target Ahead of Schedule

BYD sold 235 thousand vehicles in December, +150% yoy (It has recorded a triple-digit growth for 12 consecutive months), far higher than the overall increase of domestic new energy vehicles (about +47%), and + 2% mom, including 112 thousand pure electric vehicles, +132% yoy and down 2% mom, and 123 thousand plug-in hybrid electric vehicles, +176% yoy and +6% mom.

For 2022, BYD's new energy passenger vehicles reported a cumulative sales volume of 1,863 thousand units, +208.64% yoy, exceeding its annual sales target of 1,500 thousand units. On a closer look, the cumulative growth rate of pure electric vehicles was 184%, and that of plug-in hybrid electric vehicles was 247%. On the basis of the blade battery, the DM-i super hybrid technology, the e-platform 3.0 and the CTB battery body integration technology, new products constantly launched by the Company were significant in the competitive strength, showing a pattern of prosperous supply and demand in the terminal market.

The Product Structure Is Further Optimized, and the Proportion of High-end Models Increases

On a closer look at the models, 1) the sales volume of the Han family reached 30,043 units, +119% yoy and -5.5% mom, which has exceeded 30 thousand units for four consecutive months; 2) the sales volume of the Tang family was 20,165 units, +124% yoy and +1% mom; 3) the sales volume of the Song family was 70,079 units, +213% yoy and +9.3% mom; 4) the sales volume of the Qin family was 26,206 units, +1% yoy and -7% mom; 5) the sales volume of the Yuan family in December was 29,468 units, +244% yoy and flat mom; 6) the sales volume of the Destroyer 05/07 in December was 6,107/1,805 units; 7) the sales volume of the Dolphin in December was 26,074 units, +160% yoy and flat mom; 8) the sales volume of the pure electric sedan Seal in December was 15,374 units, flat mom, which has continued to rise since its launch at the end of July; 9) the sales volume of the BYD-Daimler joint venture Denza in December was 6,002 units, +1065% yoy and +74% mom, witnessing high year-on-year and month-on-month growths.

Overall, models of Han, Tang, Song, Yuan, Dolphin and Denza contributed to the main increment, driving the proportion of high-end models to increase by 0.58 ppts mom to 31.28%. The model structure was further optimized. On November 23, the Company announced that due to the subsidy cuts and the rising price of battery raw materials, it will raise the prices of its models of Dynasty, Ocean and Denza series starting from 2023, with an increase ranging from RMB2,000 to RMB6,000, respectively. Amid the current saturated orders, the Company's price increase strategy has reflected its product strength and strong brand power.

The Company recently announced that its new high-end brand "Yangwang" will be officially released in the first quarter of 2023. The first model is expected to be a hardcore off-road vehicle, which may be priced at RMB1,000 thousand. This will complement the Company's product line of luxury models and off-road vehicles.

Export Markets Have Explosive Potential

In order to obtain broader market space, BYD has increased its efforts to develop the overseas markets since this year. In addition to vehicle exports, the Company currently has six overseas plants in Japan, the United States, Brazil, Hungary, Thailand (under construction), and France (planned), respectively. The Company is developing the overseas new energy passenger vehicle market with the good product reputation that it has previously gained through the export of electric buses. In the short term, the Yuan PLUS, Dolphin and Seal will be successively released in the Oceania countries and the Asian countries such as Japan, Singapore and Thailand, and the Yuan PLUS, Han and Tang will be launched in the European countries such as Germany, Sweden, and Norway, and the Latin American countries such as Brazil and Mexico. In the medium and long term, the export models will also be expanded. We expect the overseas sales volume to continue to grow rapidly from less than 10 thousand units in 2021 to more than 500 thousand units in 2024 with the network expansion and successful cooperation with local dealers.

Investment Thesis

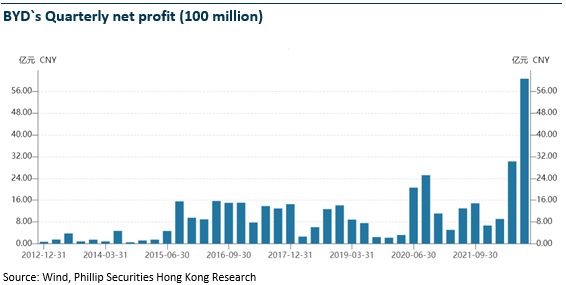

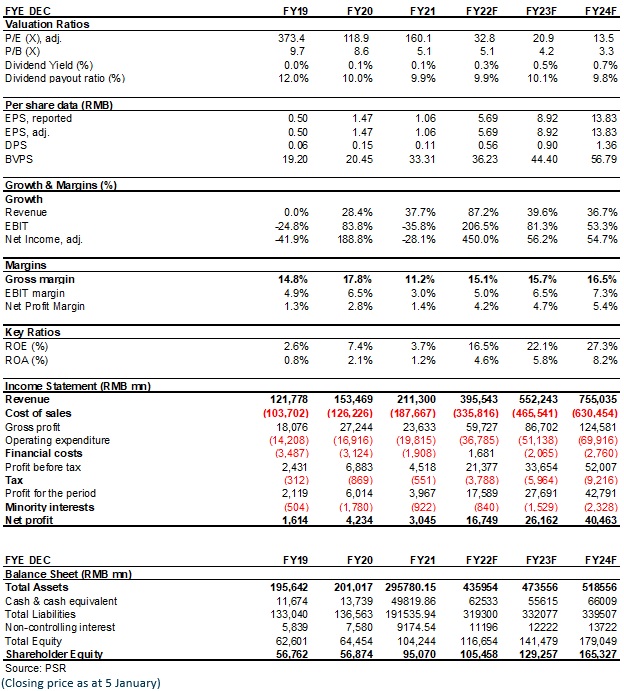

Driven by the vehicle sales surge, the Company witnessed significant improvement in the gross margin and the net profit margin and displayed strong cash flow performance, benefiting from the strengthening of scale effects and the diluted production costs and R&D expenses. In the first three quarters of 2022, the Company reported revenue of RMB267.7 billion, +84% yoy, and net profit attributable to the parent company of RMB9.3 billion, +281% yoy. In the first three quarters, the period expense ratio was 9.5%, - 0.6 ppts yoy, and the gross margin was 15.89%, +2.92 ppts yoy, of which the gross margin in Q3 was 18.96%, +5.63 ppts yoy and +4.57 ppts mom. We believe that the accelerated development of the overseas new energy passenger vehicle market, and the development potential of the new energy commercial vehicle market, the external battery supply and the energy storage business have provided a strong foundation for the Company's future growth of results. Some investors concern about the future profitability of new energy vehicles, which has not changed the expectation that the Company may play a leading role in the transformation of the automotive industry in the future.

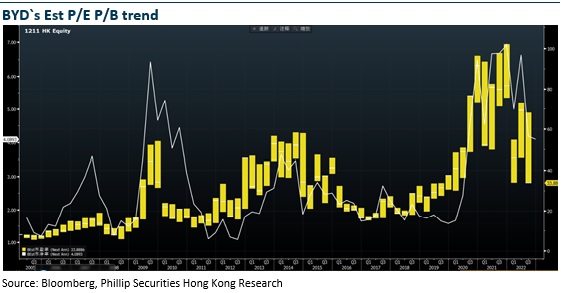

For better-than-expected FY22Q3 result, we lift the EPS forecast for 2022/2023/2024 to 5.7/8.9/13.8 yuan from 2.7/4.7/6.5. Therefore, we given the target price of 328 HK$, corresponding to 2022/2023/2024 52/33/21x P/E, BUY rating. (Closing price as at 5 January)

Risk

Sales of NEVs is not as good as expected

New business risk

Slow-down of Hand-set components business

Financials

Click Here for PDF format...