Overview

Kuaishou (1024.HK) main business includes online marketing services, live streaming and other services (including e-commerce). Online marketing business income mainly comes from short video and live broadcast advertisements, live stream business income mainly comes from paid content and the revenue sharing of users buying virtual items as gifts to anchors, other service income mainly comes from e-commerce.

A review of Q3 2022 Results

Kuaishou (1024.HK) has announced the Q3 report ended September 30 2022. The company's revenue amounted to RMB 23.1 billion, increasing 12.9% YoY. Gross profit amounted to RMB 10.7 billion, increasing 25.8%. Gross profit margin was 46.3%, increasing 4.8 percentage point YoY. Operating loss was RMB 2.6 billion, loss narrowed by 64.7% YoY. The loss for the period was RMB 2.7 billion, loss narrowed by 61.7% YoY. Adjusted net loss amounted to RMB 671.9 million, loss narrowed by 85.4% YoY. Adjusted EBITDA amounted to RMB 1.02 billion, out of the red YoY.

Revenue by Business Type

Revenue from online marketing services amounted to RMB 11.6 billion, increasing 6.2% YoY, primarily attributable to the growth in the number of advertisers and the increased advertising spending from the advertisers, especially from e-commerce merchants.

Revenue from live streaming business amounted to RMB 8.9 billion, increasing 15.8% YoY, as a result of 29.3% YoY growth in average MPUs, which was supported by the consistent refinements of company live streaming operations and the continuously evolving collaboration strategy with talent agencies including corresponding increase in the number of active streamers managed by those talent agencies.

Revenue from other services amounted to RMB 2.6 billion, increasing 39.4% YoY, primarily due to the growth of e-commerce business, as a result of the growth in e-commerce GMV, which was driven by an increase in the number of active merchants, number of e-commerce paying users and the improved repeat purchase rate.

Business features

The company's three main businesses are all developed around user traffic. The traffic brought by live stream and short video business attracts advertisers to place advertisements on the platform and increase e-commerce revenue, while advertising and e-commerce revenue can provide creators engaged in live stream and short video bring in more revenue and attract more creators to join Kuaishou. For example, Kuaishou guides live stream e-commerce advertisers to invest resources in short video platforms, and at the same time encourages short video advertisers to participate in live stream, bringing more marketing opportunities to advertisers. Overall, the three main businesses can add value to each other.

Short video business

Kuaishou's main competitor is Douyin, a subsidiary of ByteDance, and the competitive market is divided into the Chinese mainland market and overseas markets. Douyin and Kuaishou are significantly ahead of their peers in terms of user scale. Kuaishou's average DAUs in the Q3 reached 363 million. According to a report by the Chinese media Science and Technology Innovation Board Daily, Douyin's global DAUs reached 1 billion on October 18,2022, making it the first Chinese Internet company to be a member of the global billion DAUs club. In terms of development style, in addition to short videos posted by users, Kuaishou is more focused on developing sports-related content, such as cooperating with the American NFL professional American football game in 2020, winning the broadcast and short videos second creation copyrights of the 2021 Tokyo Olympics and the 2022 Beijing Winter Olympics, while Douyin has been focusing on developing music-related content.

In the Chinese market, according to the 2022 China Short Video Industry Insight Report by the data intelligence technology platform Mob. Both main user ages are 25-34 years old. According to the distribution of city lines, the users of Douyin in the first to second tier cities accounted for 42.4%, and the users in the third to fifth tier cities accounted for 57.6%. The users of Kuaishou in the first to second tier cities accounted for 36.1% and the users in the third to fifth tier cities accounted for 63.9%. The data shows that Kuaishou and Douyin also have a higher proportion of users in third to fifth tier cities. Compared with Douyin and Kuaishou, Douyin has a higher proportion of users in first to second tier cities.

Traffic distribution

Douyin's traffic distribution mainly relies on system algorithm recommendations, adopts a centralized (platform plays an important role) traffic distribution model, and tends to recommend content to users that they like to watch. For example, after a short video is released, the algorithm will have a series of criteria, including the number of views and likes, etc., to evaluate whether the short video is popular. If the short video is popular, it will be recommended to more users to watch. Viewers tend to create high-quality short videos to get more traffic. On the contrary, Kuaishou's traffic distribution is mainly to recommend the content they care about to users and adopts a decentralized (the platform is less important) traffic distribution model. For example, after a creator releases a short video, the following users will be notified first. This mechanism allows the creator to build a relationship with fans and create a community culture, and the traffic distribution is relatively equal, but it will reduce the incentive for creators create high-quality short videos.

Overseas market

Kuaishou lags far behind Douyin. According to data survey agency Sensor Tower, Douyin overseas version TikTok has become the world's most downloaded app on both platforms for four consecutive years since 2018. In the first quarter of 2021, the cumulative downloads reached 3.5 billion, beating applications such as Facebook, Instagram and Whatsapp under Meta. In addition, Douyin and TikTok had a revenue of more than USD 315 million in September 2022, an annual increase of 1.7 times, and they continue to be the top non-game global mobile application revenue list. In addition, it will rakn second in the global mobile application(non-game) download ranking in November 2022, with nearly 55 million downloads, which is basically the same as the same period last year. Kuaishou launched overseas versions Kwai and SnackVideo, which are mainly developed in Latin America (Brazil), the Middle East and Southeast Asia (Indonesia). Compared with Douyin's success in the global market, Kuaishou is still struggling in some overseas markets. We believe that the main reason why Kuaishou develops these regions is because the language system in these regions is unique and the user base is large. Since, TikTok is very popular in Europe and the United States, so Kuaishou focuses on developing countries with different languages and cultures to avoid Douyin. However, TikTok intends to compete directly with Kuaishou in different regional markets. For example, TikTok will launch more activities in markets where Kuaishou intends to develop to attract users and business opportunities. According to Sensor Tower, in November 2022, China is the market with the largest downloads of Douyin, accounting for 12.3%, followed by Indonesia, accounting for 8.5% and the United States accounting for 8.2%. This reflects that TikTok is focusing on the development of the Indonesian market and directly competes with Kuaishou's SnackVideo. TikTok is better than Kuaishou in terms of brand effect and traffic. Therefore, for Kuaishou, regions such as Brazil and Indonesia are still markets with great potential but fierce competition. In term of data, the operating loss of Kuaishou's overseas division in the third quarter of 2022 was RMB 1.69 billion, loss narrowed by 41.4% YoY. The narrowing of losses was mainly due to the rapid growth of overseas revenue and the company's continuous improvement in the efficiency of marketing expenditures under the global strategy driven by return on investment (ROI).

Iive streaming business

Kuaishou Live is a comprehensive live stream platform that mainly develops game live stream. However, the platform also has other themes such as beauty makeup and science popularization. The themes are quite diverse and suitable for all ages to watch. The main competitors of Kuaishou include Douyu, Huya and other traditional game live stream platforms. Traditional game live stream platforms mainly rely on the anchor to entertain viewers and attract users, while the income of the anchor mianly depends on the “rewards” from audiences after share with the platform and the high-priced signing fees of the live broadcast platform in order to retain popular anchors. It can be seen that the source of income is quite single. Different from traditional game live stream platforms, Kuaishou already has a certain amount of traffic due to its short video business, so it does not need to rely too much on popular anchors. On the contrary, Kuaishou can bring traffic to contracted anchors. For example, Kuaishou launched the “Blue Ocean Project". As long as the guild meets certain conditions, such as the number of turnover and the number of broadcast anchors, etc., it can obtain the qualification of a partnership guild in the city where it is located, and enjoy the platform's hundreds of millions of traffic support, additional sharing incentives, and exclusive traffic slots. In addition, Kuaishou's anchor monetization methods are more than traditional game live stream platforms. Not only does it have revenue from viewers` rewards, but also income from advertising and e-commerce. For popular anchors, the income potential is greater and can attract popular anchors to settle in. In the third quarter, the number of active guild anchors in Kuaishou increased by more than 200% YoY.

E-commerce business

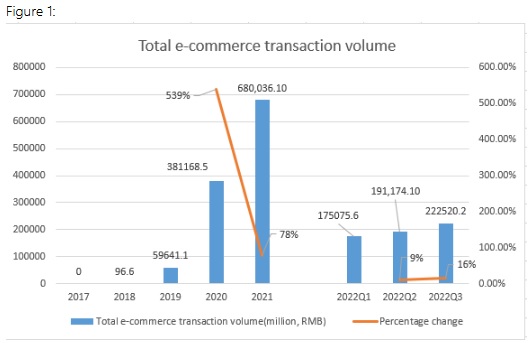

Kuaishou's e-commerce business has been in operation since August 2018 and has grown rapidly with the “content e-commerce” model in live e-commerce. For “traditional e-commerce” merchants, the platform is just a sales channel. They attract customers through sales volume and discounts, and all aspects of sales, customer service communication and payment are completed on the platform. For “content e-commerce”, in addition to discounts and other factors, merchants or anchors will also introduce products, try them out and answer audience questions through live stream, so that audiences can better understand the products. As can be seen from Figure 1, Kuaishou's total e-commerce commodity transactions in the third quarter were RMB 222.52 billion, increasing of 16% from the previous quarter. The total transaction volume in the first three quarters was RMB 588.77 billion. It has reached 87% of the total transaction volume for the whole year of 2021. In the fourth quarter, there are large-scale promotional activities such as Double 11 and Double 12, which is expected to drive a YoY increase in e-commerce revenue. The data shows that the explosive period of Kuaishou e-commerce business has passed, but the growth is still at a relatively fast level. In addition, Kuaishou enhances consumers` trust in the platform and merchants by strengthening the service and management of merchants and the protection mechanism of users` rights and interests, thereby increasing the repeat purchase rate of customers. Currently, Kuaishou's biggest competitors in live e-commerce are Douyin and Taobao. According to the report of Qianzhan Industry Research Institute, in 2020, the market share of China's live streaming e-commerce industry is dominated by Douyin, Taobao, and Kuaishou, with Douyin accounting for 38.9%, Taobao accounting for 31.1%, and Kuaishou accounting for 29.7%. In 2021, the market share of China's e-commerce industry was about 52% for Taobao, about 20% for JD.com, about 15% for Pinduoduo, about 5% for Douyin and about 4% for Kuaishou. We believe that the new sales model of “content e-commerce” can arouse the public's desire to shop more than traditional e-commerce, so we expect that “content e-commerce” will continue to seize the market share of traditional e-commerce.

User data

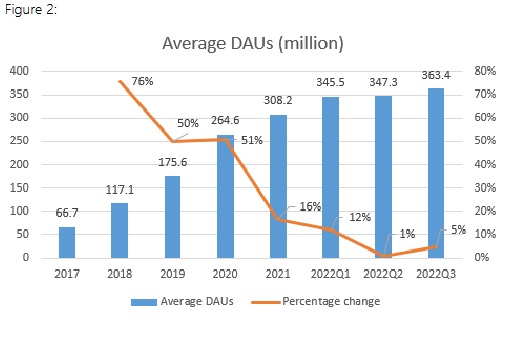

Kuaishou's three main businesses all develop around user traffic, so how to retain users and increase user traffic is the company's top concern. In terms of average daily active users, it can be seen from Figure 2 that the company's average daily active users have continued to rise since 2017. But in recent years began to saturate, the growth rate has repeatedly declined. The average DAUs in the third quarter of this year were 363.4 million, an increase of 5% QoQ, and only increase of 1 %QoQ in second quarter. The low-single-digit growth for two consecutive quarters reflects the slowdown in the growth of average daily active users.

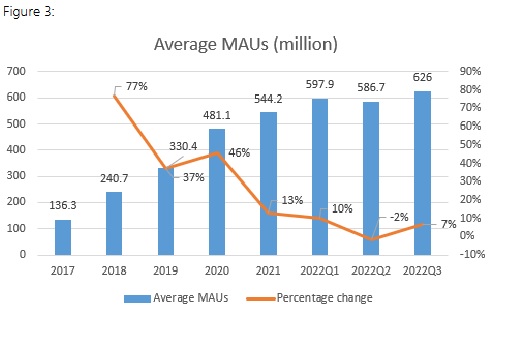

In terms of average MAUs, it can be seen from Figure 3 that the company's average MAUs have continued to rise since 2017, but in recent years it has become saturated, and the growth rate has repeatedly declined. The average MAUs in the third quarter of this year were 626 million, an increase of 7% QoQ, better than the 2% QoQ declined in the second quarter.

�

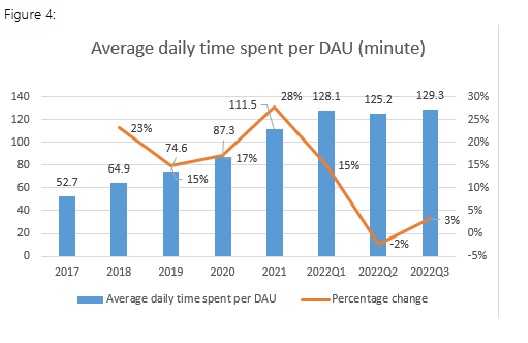

In terms of the average daily usage time of each DAU, it can be seen from Figure 4 that the company's average daily usage time of each DAU has continued to rise since 2017, but it has become saturated in recent years, and the growth rate has repeatedly declined. In the third quarter of this year, the average daily usage time of each DAU was 129.3 minutes, an increase of 3% from the previous quarter, better than the 2% QoQ declined in the second quarter.

From the above three data, it can be seen that the active users of the Kuaishou platform have begun to saturate, and the single-digit growth in the third quarter may be due to holiday factors such as summer vacation. It is expected that the number of active users of Kuaishou will maintain a low-single-digit increase in the future, and how to improve platform user stickiness, community activity, and increase the payment conversion rate of existing users will become important matters that the company needs to pay attention to. Kuaishou is currently conducting refined operations for different groups of people through algorithm models, reducing the maintenance cost of each DAU. In addition, as of the end of September 2022, the cumulative number of interrelated user pairs (a pair of users who follow each other) of Kuaishou apps has reached 23.5 billion, a substantial increase of 63.1% YoY, and users are connected and concerned about each other, which will help user retention. Besides, Kuaishou have been actively expanding content supply in various verticals and exploring more diversified themes to enhance platform video content, attract and retain users. For example, Benevolence (2 minutes per episode), a portrait of the professional lives of medical staff, and the variety reality show Let's Go! Mom (45 minutes per episode) adopted a narrative and dissemination format that combined long video, short video and live streaming.

Positive factors

China's relaxation of anti-epidemic measure boosts business activity

Facing negative factors such as high inflation, high interest rates, and expected recession in the external economy, business operations have become more conservative and have reduced real economic activities, thus affecting, for example, corporate advertising. In China, the overall economy is mainly affected by the epidemic prevention policy and domestic real estate debt. With the reduction of epidemic prevention restrictions in China, a series of policies to support domestic real estate companies and the change in the tone of the Central Economic Work Conference. We believe that the worst situation of the Chinese economy has passed, and it is expected that enterprises will slowly resume and increase normal business activities. However, enterprises need time to reassess the situation and regroup. The real economy will only improve slowly without a strong rebound. Therefore, Kuaishou advertising business will main steady growth.

Under the impact of policies, Chinese users` entertainment patterns have changed

The “2022 Progress Report on the Protection of Minors in China's Game Industry” released in November 2022 pointed out that 65% of minors will use the time saved to watch short videos after the game time is limited. Although the spending power of minors is limited, it is positive for the continuity, activity, user hours and user stickiness of the platform, which is beneficial to the long-term development of short video platforms including Kuaishou.

Reorganization of overseas markets is expected to become a growth driver

In the past few years, the company's internationalization strategy has been vacillating, and many people in charge have been replaced successively, wasting the opportunity to develop overseas markets. However, in August this year, Ma Hongbin, the former head of the commercialization business, took over as the head of the international business department, and adjusted the structure of overseas business. Focusing on the development of Brazil and Indonesia through Kwai and Snack Video may change the previous overseas market strategy. In the uncertain situation, investors need to pay attention to Kuaishou's follow-up overseas business development policy and personal changes. Although the company has long lost the opportunity, it is difficult to compete with TikTok in Key overseas markets such as Europe, the United States and Japan, and international social platforms such as Youtube, Instagram and Facebook have launched similar short video functions to seize the market, but markets such as Brazil and Indonesia still have huge potential. Even in the face of direct competition from TikTok, it is believed that the company's revenue from overseas markets will increase and become a new growth driver for the company.

Cost control performed well

In the third quarter of 2022, only the revenue sharing costs and related taxes and payment processing costs increased YoY due to the increase in related revenue, and the rest of the cost of revenues decreased YoY. In addition, sales and marketing expenses and R&D expenses both decreased by 17.1% and 16.2% YoY, respectively. Reflecting the company's success in controlling costs and reducing expenses to cope with the gloomy economic outlook and the end of the business outbreak period, the operating loss in the third quarter was RMB 2.61 billion, a loss narrowed by 64.7% YoY. In the context of internal and external economic instability, user data saturation and uncertain overseas market development, effective control and reduction of costs and expenses will benefit the company's development.

�Risk factors

Regulatory risk from China

“Internet short video content review standard rules 2021” issued by the China Internet Audiovisual Program Service Association. It has formulated as many as 100 detailed rules to supervise short videos, such as not cutting without authorization, adapting movies, online film and television dramas, etc. Restrictions on programs and clips, the relevant rules limit the creative space of creators, and affect the diversity of content on short video platforms. Also, the relevant authorities may introduce more regulatory policies in the future. However, at the Central Economic Work Conference held on December 15-16, 2022, President Xi proposed that China should focus on developing the digital economy, improve normalized regulatory standards, and support platform companies to play a leading role in leading development, creating jobs, and competing internationally. We believe that China's employment situation and economy are not optimistic due to factors such as the epidemic, domestic housing and supervision (such as policies in the education sector) in recent years. If the China government want to effectively boost employment and the economy, it is necessary to introduce strong policies to support the development of enterprises. At the same time, the impact of regulations on enterprises will be reduced, which will benefit the platform economy including Kuaishou.

Tencent dividend risk

In recent years, Tencent has successively paid out dividends by distributing the shares of JD.com and Meituan to shareholders in the form of physical objects. Tencent is also a major shareholder of Kuaishou, holding about 11.84% of Kuaishou's shares. If Tencent distribute the shares of Kuaishou to shareholders, shareholders may sell the Kuaishou shares obtained from the dividend due to different factors, such as wanting to receive cash dividends or not wanting to hold Kuaishou in terms of asset allocation, etc., which may affect Kuaishou's stock price in short-term. Investors should pay attention to related risks.

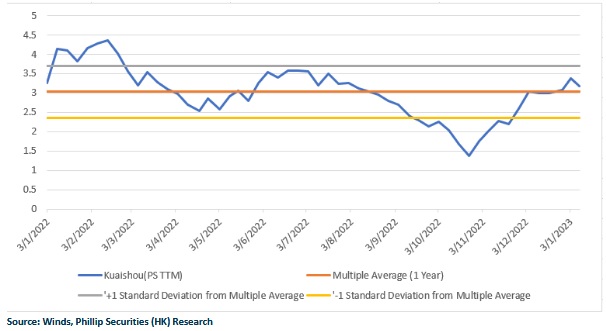

Valuation and recommendation

We believe that the company's business model of using the user turnover brought by short videos to help the development of live stream and e-commerce business is very effective. Although the DAUs and average daily suage time of short videos in the mainland have begun to saturate, due to the above-mentioned policy changes, it is expected that the revenue of the advertising business in the future will improve with the gradual recovery of various industries. In term of live stream business, the live stream industry is quite saturated and full of competitors. Although Kuaishou has unique advantages compared with traditional live stream platforms, it can seize the market share of traditional live stream platforms, such as having a huge user flow and providing e-commerce and other monetization for streamers. It can attract streamers or media companies to cooperate with Kuaishou, but this business model is not irreproducible. For example, Douyin can use the same business model to compete with Kuaishou. Overall, we believe that the e-commerce business and overseas business will become the biggest growth drivers of Kuaishou in the future. Also, the company has performed well in controlling costs and expenses. However, the competition in the overseas market is fierce, and the management of the overseas business has been changed many times, which brings uncertainties. Investors need to continue to pay attention to the development of Kuaishou's overseas market, including whether the cost of publicity will be too much, the average daily usage time of overseas users and user growth data. We expect Kuaishou's net sales amount to RMB 91.4 billion, 105.9 billion and 125.6 billion in FY2022-2024 respectively, CAGR is 11.15%. Corresponding P/S ratio are 3.50/3.02/2.55x. We give Kuaishou 3.2x P/S in FY2023 and a target price of $91.3 HKD. (Calculated at the exchange rate of RMB to HKD 1.16), with a “buy” rating. (Current price as of January 13)

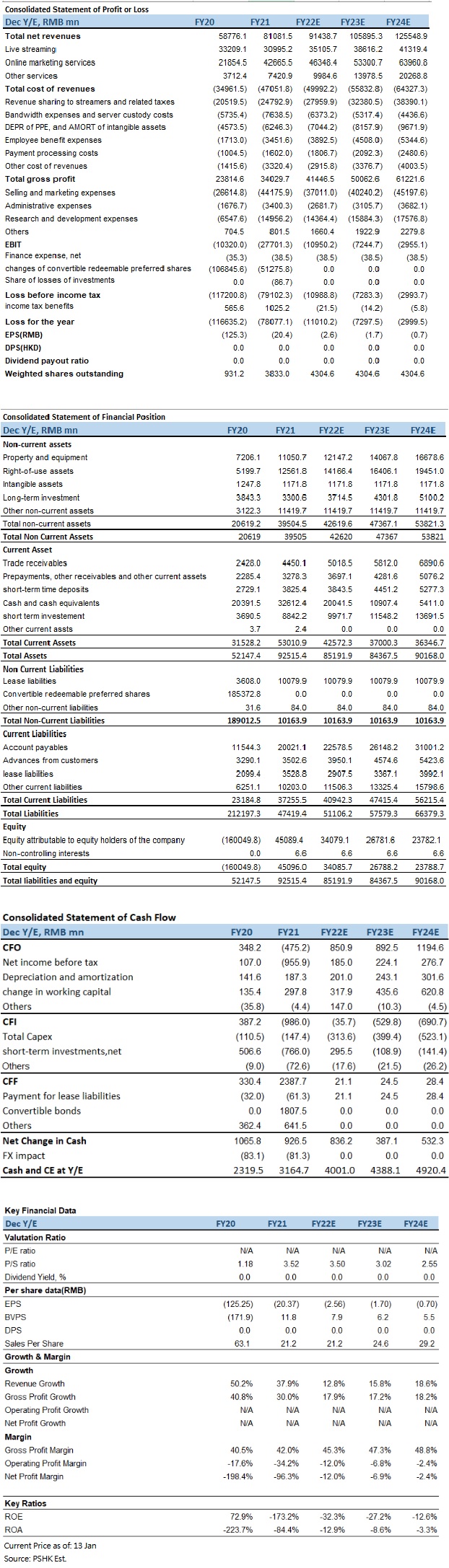

Financial

Click Here for PDF format...