Overview

Bilibili (9626.HK) is an online entertainment platform for young generations. Its main businesses include mobile games, value-added services, advertising, e-commerce and others. The main income of mobile games is the company's distribution of mobile games for third-party game developers on its platform. Users can download and play with Bilibili accounts for free, while users purchase virtual items in the games to get a better gaming experience, allowing the company to earn revenue from it. The main income of value-added services is the subscription fee from premium membership. Premium members can obtain exclusive rights to original or licensed content, the sale of virtual gifts in live channels and the sale of paid content and virtual items on the company's video, audio and comic platforms. Advertising revenue mainly comes from various forms of advertising services, including advertisements that appear on the launch page or top of mobile applications, banner brand advertisements at the top of website homepages, and performance advertisements that appear mainly in the form of organic feeds next to online video feeds. E-commerce and other major revenues come from the company's online sales of ACG (animation, comics and video games) related products and offline performance and event ticket sales.

A review of Q3 2022 Results

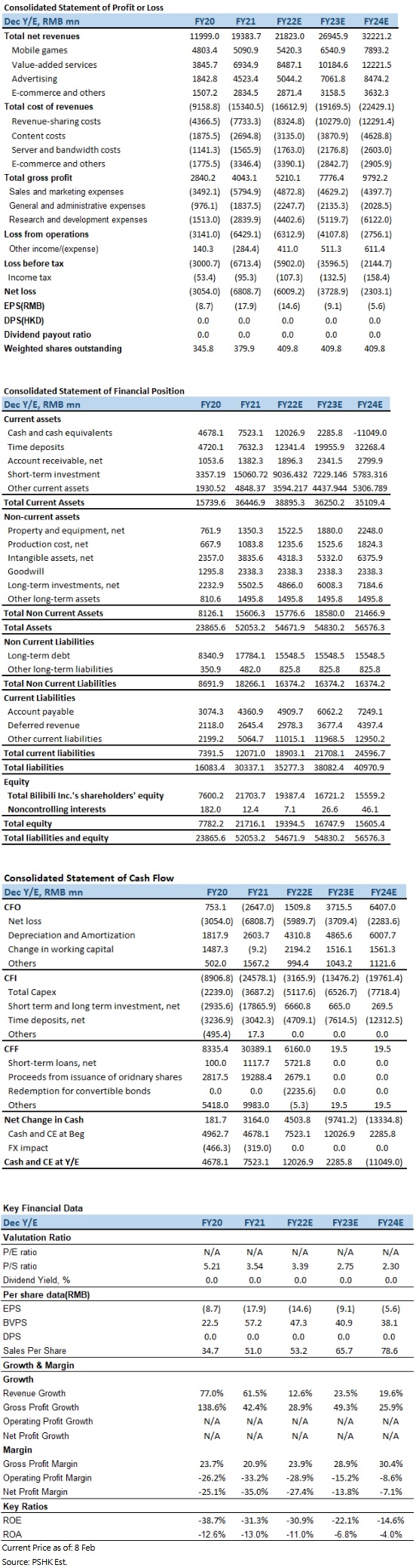

Bilibili (9626.HK) has announced the Q3 report ended September 30, 2022. The company's revenue amounted to RMB 5.8 billion, increasing 11.1% YoY. Cost of revenue amounted to RMB 4.7 billion, increasing 13.1% YoY. Gross profit amounted to RMB 1.1 billion, increasing 3.5% YoY. Gross profit margin was 18.2%, decreasing 1.4 percentage point YoY. Operating loss was RMB 1.9 billion, loss slightly narrowed by 1.6% YoY. The loss for the period was RMB 1.7 billion, loss narrowed by 36.1% YoY. Adjusted net loss amounted to RMB 1.8 billion, loss expanded by 8.8% YoY.

Revenue by Business Type

Mobile game revenue were RMB 1.5 billion, increasing 5.7% YoY. The increase in revenue was primarily attributable to the newly launched mobile games.

Value-added revenue were RMB 2.2 billion, increasing 15.8%, mainly attributable to the company's enhanced monetization efforts, led by an increased number of paying users for the company's value-added services, including the premium membership program, live broadcasting services and other value-added services.

Advertising revenue were RMB 1.4 billion, increasing 15.6% YoY, primarily attributable to further recognition of Bilibili's brand name in China's online advertising market, as well as BiliBili's improved advertising efficiency.

E-commerce and others were RMB 757.8 million, increasing 3.2 YoY.

Business features

The company is a comprehensive video community that provides a large amount of rich content to meet the diverse interests of young people, and users and content creators can interact with each other. The content categories include life, games, entertainment, animation, knowledge and many other fields. The company also supports a wide range of video content consumption scenarios, centered on professional user-generated video (PUGV), supplemented by live broadcast, professional organization-generated video (OGV), etc.

User data and characteristics

The users of the platform are mainly people of the Z+ generation, which refers to people born in the middle and late 1990s to the early 2010s. According to the iResearch report, among the MAUs of the platform in 2020, users aged 35 and below accounted for more than 86%. Formal users of the platform need to pass a membership examination consisting of 100 multiple-choice questions to become a formal member, and the formal membership that is difficult to obtain will make users value and cherish it more, and thus have higher participation and loyalty, including actively using various social and interactive functions provided on the platform, such as sending bullet chats (referring to the real-time subtitle comment function that originated in Japan and prevailed in China), comments and private messages, to improve the user stickiness of the platform. As of December 31, 2021, the company had approximately 145.3 million official members, increasing 41.6 YoY. In addition, in recent years, the average daily time spent by active users on the company's mobile applications has remained at more than 80 minutes and will reach a record high of 96 minutes in the third quarter of 2022, reflecting the continued rise in popularity of the platform.

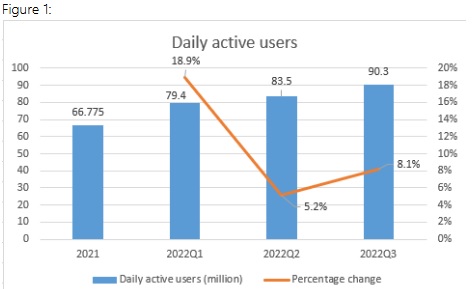

In terms of DAUs, it can be seen from Figure 1 that the average DAUs have been rising steadily, reaching 90.3 million in the third quarter of 2022, increasing 8.1% QoQ and increased of 5.2% QoQ in the second quarter.

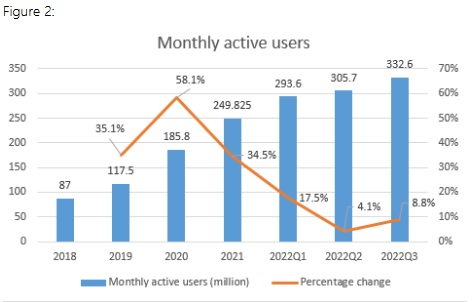

In terms of average monthly active users, it can be seen from Figure 2 that the average monthly active users have been rising steadily, but the growth rat has continued to decline. In the third quarter of 2022, it reachs 332.6 million people, increasing 8.8% QoQ, and increased of 4.1% QoQ in the second quarter. The single-digit growth of the two data for two consecutive quarters reflects the slowdown in the growth of average active users, and the reason for the higher growth in the third quarter than in the second quarter may be due to the seasonal factor of summer vacation.

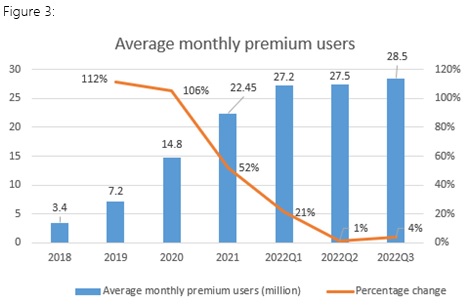

In terms of average monthly premium users, it can be seen from Figure 3 that the average monthly premium users have been rising steadily, but the growth rate has continued to decline since 2020. In the third quarter of 2022, it will reach 28.5 million people, increasing 3.6% QoQ, while in the second quarter it only increased by 1.1% QoQ. The two consecutive quarters of low-single-digit growth reflect that the average monthly premium user is close to the peak.

Video content

95% of the video views on the company's platform comes Professional User-Generated Video(PUGV) and vertical video( Story Mode). Vertical video is a popular form of video transmission in recent years. It is suitable for mobile phone users to watch and caters to the current trend of information and time fragmentation. It is convenient for users to watch videos anytime and anywhere. In term of data, in the third quarter of 2022, the total user time of the platform increased by 37% YoY, and the average daily video playback volume increased by 64% YoY. Among them, at the financial report meeting in Mach 2022, Chen Rui, CEO of Bilibili, said that the DAU penetration rate of Story Mode has exceeded 20%. Investors can expect that as Story Mode is realized, it can drive advertising revenue to increase.

In terms of video creation, a good cycle has been formed between the three elements of content creators, creation and fans. More and higher-quality videos will help users retain. When the content creators create high-quality videos and is loved by fans, the positive reaction and increase in the number of fans will encourage those content creators to create more high-quality videos and attract more people to try to create videos. In terms of data, the number of monthly active content creators on the company's platform in the third quarter was 3.8 million, increasing 40.7% YoY. The average number of submissions per month was 15.6 million, increasing 54.5 YoY. The number of content creators with more than 10,000 fans increased by 48% YoY.

Mobile games

As of December 31, 2021, the company has operated 59 exclusive mobile games and hundreds of jointly operated mobile games. From 2018 to 2021, mobile games accounted for 71.1%, 53.1%, 40% and 26.3% of the company's total revenue respectively, while the top three mobile games contributed 61%, 36%, 24% and 10.7% of the company's net turnover respectively. Mobile game revenue continues to rise while the two figures continue to fall. On the one hand, it reflects the successful commercialization of other businesses of the company, and revenue no longer depends on a single business. On the other hand, it reflects that the number of exclusive licensed games of the company has increased, and the dependence on popular exclusive licensed mobile games has decreased. Currently, the company's top three exclusive mobile games are Fate/Grand Order (FGO), Guardian Tales and Azur Lane.

Fate/Grand Order is a turn-based card mobile game developed by Japanese game production company Delightworks and launched in July 2015, Bilibili began to exclusively represent the game in China in September 2016. This game is a work derived from the “Fate” series of the Japanese game publisher Type-Moon. Type-Moon launched the R-18 text adventure game Fate/Stay Night in 2004. Later, because of its unique worldview and wonderful plot, related animations and movies were launched, and many fans have been accumulated around the world. Fate/Grand Order is still one of the most popular games on Bilibili after its launch in China. According to data from mobile market information tools quoted by the game media Mobilegamer.biz, the total global revenue of Fate/Grand Order in 2022 were approximately USD 500 million, ranked No.13 globally. In addition, according to the data research agency Sensor Tower (the data does not include third-party Android platforms in China or other places, the same below), the revenue of Fate/Grand Order in China in December 2022 were around USD 3 million with about 20K downloads. Besides, the cumulative downloads of the game on the TapTap platform were approximately 4.5 million. The overall data shows that the popularity of this game, which has been launched for about 7 years, is still very good.

Guardian Tales is a pixel-style adventure role-playing game launched by Korean game developer Kong Studios in February 2020, and Bilibili exclusively represented the game in China since April 2021. According to Sensor Tower, the revenue of this game in December 2022 were around USD 400K, with around 10k downloads, and the cumulative downloads of the game on the TapTap platform were around 1.7 million.

Azur Lane is a simulation ship development game produced by Shanghai Manjiu Network Technology and Xiamen Yongshi Network Technology, released by Bilibili in May 2017. Players mainly develop a fleet and carry out various missions and battles, and the warships in the game refer to “ship girls” (anthropomorphic warships, usually female characters). According to Sensor Tower, the revenue of this game in December 2022 were around USD 4 million with about 30k downloads, and the cumulative downloads of the game on the TapTap platform were around 4.3 million. The data shows that the popularity of this game, which has been launched for about 6 years, has been maintained very well.

Princess Connect Re:Dive is a fantasy-style role-playing mobile game launched by Japanese game developer Cygames in February 2018, and Bilibili exclusively distributed the game in China since April 2020. Players mainly collect and develop various female characters for various battles. This game used to be one of the first three popular games on Bilibili, but the popularity of the game has declined rapidly. According to Sensor Tower, the revenue of this game in December 2022 were USD 100k with about 10k downloads and the cumulative downloads of the game on the TapTap platform were around 2 million.

Positive factors

The company deeply cultivates ACG content to grasp the market trend

Since its inception, the company's development direction has been focusing on ACG (animation, comics and video games), including the founder and the president XU Yi and the chairman Chen Rui, are all senior ACG enthusiasts, so that the company has a very in-depth understanding of ACG culture and trends, and can also understand the current trend of ACG culture from user discussions or the number of occurrences of a certain topic through the platform. When there is a phenomenon-level popular ACG, Bilibili can often seize the opportunity to obtain the exclusive licensed right of the work in China.

Re-approval of imported game licenses are good for the company's game revenue

On December 28, 2022, the National Press and Publication Administration approved the version numbers of 84 domestic online games and 44 imported games. This is the first time since June 2021 that imported game licenses has been approved, and there are many high-quality games among them. With the normalization of the approval of imported game licenses, it will benefit Bilibili and other companies that rely on agents to import games. In addition, due to the cooperation between Bilibili and Japanese game developer Cygames in the agency of Princess Connect Re:Dive, we believe that if the license of Cygames` another popular game Umamusume is approved, Bilibili will represent this game in China. The game caused a global boom in the first month after its launch in March 2021, surpassing MiHoYo's Genshin Impact to become the No.1 game in the world in terms of global revenue in that month. According to the game media Mobilegamer.biz, Umamusume amounted a total global revenue of about USD 550 million in 2022, ranked No.12 in the global mobile game, and this data was achieved without revenue in China, reflecting that the game is still very popular in the world and has growth potential.

Chen Rui directly manages the game department and focuses on the game business

Bilibili's mobile game business has always relied heavily on exclusive licensed games, and its ability to independently develop games is weak. The suspension of the approval of imported game licenses has a greater impact on the company, and this incident of stopping the approval of the licenses also exposed the weakness of the company's poor ability to independently develop games. Although the re-approval of imported game licenses is very beneficial to the company, the approval of imported game licenses is usually issued every few months to a year. The approval speed is slower than local games, and the possibility of stopping the approval of game licenses in the future cannot be ruled out. In addition, two of the company's three highest-grossing exclusive licensed games have been launched for more than six years, and it is necessary to develop new popular games to become the company's new growth driver. According to the company's internal emails quoted by multiple media, the chairman Chen Rui will directly listen to the report of the game business, and then further strengthen the game business and implement the company's game business strategy of “self-developed with high quality and global distribution”, reflecting that the company also understands its own weaknesses and start making changes. However, the cost of developing high-quality and popular games is relatively high, and the company lacks successful experience. Investors should pay attention to the development of the company's game business in the future.

The unique culture of the platform constitutes a strong moat

There are only two comprehensive ACG platforms in China and Bilibili is one of them, but its competitor AcFun lags far behind Bilibili in term of number of users and other aspects. The company's core competitiveness comes from the circle formed by people who love ACG culture to communicate with each other and generate cultural resonance, so the platform still retains a fairly high formal membership threshold. To a certain extent, ensuring the quality of members will not affect the circle of existing platforms, and this circle is Bilibili's unique moat. High user stickiness makes it difficult for other platforms to copy or replace. In addition, with the continuous emergence of new phenomenon-level ACG works, more and more people pay attention to ACG works, such as the game Elden Ring that swept various awards in 2022 and the animation Demon Slayer: Kimetsu No Yaiba was popular all over the world in 2021. Coupled with the rise of domestic ACG works, the market scale continues to expand, which is conducive to the long-term development of Bilibili. According to iResearch's 2021 China Secondary Industry Research Report, the number of pan-two-dimensional users (meaning that they have consumed some two-dimensional products but are not as enthusiastic about two-dimensional products as the core group) reached 420 million people in 2020, and it is expected to reach 500 million people in 2023, with a compound annual growth rate of 4.46%. Besides, the combined market size of the two-dimensional content market and the two-dimensional peripheral derivative market reached 100 billion in 2020, and it is expected to reach 221.9 billion in 2023, with a compound annual growth rate of 22.05%.

Risk factors

Lack of overseas experience, R&D costs rise

The company's businesses mainly revolve around the development of the ACG cultural circle in China, and it is difficult to expand its business overseas. As for whether self-developed games can go overseas in the future, the company's ability to self-develop games has always been relatively weak, and the possibility of developing games that are popular with global players is low. Since the game license has been suspended twice in recent years and under the influence of the game restriction policy, the game industry has lost a sense of security in the Chinese game market. The large and capable game leaders in the mainland have deployed overseas to find new growth drivers. In addition, the game industry expects that the approval of domestic game licenses will be tightened for a long time, and it is necessary to seize the opportunity of each license approval and focus on the development of high-quality games. For example, Tencent and NetEase have acquired several overseas game studios in order to expand overseas markets and strengthen the development of high-quality games to engage in an arms race in games. However, Bilibili has always been good at introducing overseas games to the mainland rather than developing games and lacks the experience of self-developed games going overseas. This is exactly the opposite of the current environment of the mainland game industry. If Bilibili, which has weak self-development capabilities, needs to keep up with the changes in the general environment of the mainland game industry, the cost of developing games or acquiring game studios will increase significantly. In fact, the company's total R&D cost in the first nine months of 2022 amounted to 3.3 billion, which has surpassed last year's R&D cost by 15.2%, reflecting the trend of high-quality domestic games that has greatly increased the company's R&D costs.

Chinese game market revenue declined in 2022

According to the game industry report released by Gamma Data on January 13, 2023, the actual sales revenue of the Chinese game market in 2022 amounted to 265.88 billion, decreasing 10.3% YoY. The number of players was 660 million, slightly decreasing 0.33% YoY. The actual sales revenue of self-developed games in the domestic market amounted to 222.38 billion, decreasing 13.1% YoY. The actual sales revenue of self-developed games in overseas markets amounted to USD 17.35 billion, decreasing 3.7% YoY. The data shows that due to the suspension of the game license, the mainland game market lacked the stimulation of new popular games in 2022. In the case of a slight decline in the number of players, domestic players will reduce spending in existing games, resulting in a double-digit decline in related revenue. The low-single-digit decline in the revenue of domestic games in overseas markets is mainly affected by two global factors. According to another 2022 global game market report released by the research organization Newzoo, the reason for the decline in global mobile game revenue is that the average time spent by global mobile game players on games has decreased significantly compared to the past two years, and the money spent on mobile games has also decreased accordingly. Moreover, the global economy is affected by high inflation, and many people tighten consumption and reduce expenditure. However, Bilibili lacks the ability to seize overseas market, and its game business is more affected by policies change in the mainland. Investors should pay attention to related risks.

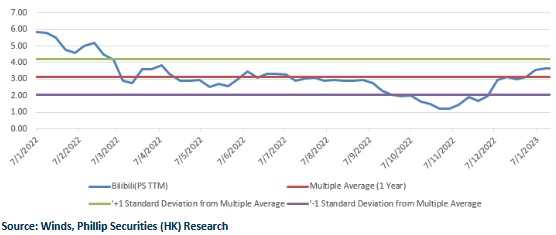

Valuation and recommendation

The company is the largest comprehensive ACG platform in China, representing the Chinese ACG circle, and we believe that the ACG cultural circle is Bilibili's unique moat, and high user stickiness makes it difficult for other platforms to replicate and replace. With the development of foreign and domestic ACG, the growth of pan-two-dimensional users will benefit the company's development. Besides, more than 86% of the active users on the company's platform are users aged 35 and under. The user group is more receptive to multiculturalism and new things, enabling the company to develop other multiculturalism. For example, the rap program New Rap Generation has a good reputation. We believe that the company's future growth drivers lie in three aspects, namely, as the young user group grows, their spending power increases, the development of multiculturalism drives the increase in platform traffic, the increase in commercial advertising revenue, and the continued development of the ACG circle to enjoy the development of the industry dividend. As for the game business, although the re-approval of imported games is great news for the company, it is expected to drive the company's game business to return to normal growth, in the long run, domestic game companies need to self-develop their games with high-quality and seize overseas market will increase the company's operating costs. In particular, these three items are weaknesses that Bilibili has not been able to solve for a long time, investors need to pay attention to the positioning and changes of the company's game business after the company's chairman Chen Rui directly listens to the report on the game business, and whether it can launch popular games in the future. Self-developed games will be the key to the company's game business. The company expects revenue in the fourth quarter of 2022 to be 6 - 6.2 billion, increasing 3.87% to 7.3% YoY. We expect Bilibili's net sales amount to RMB 21.82 billion, 26.95 billion and 32.22 billion in FY2022-2024 respectively, CAGR is 13.9%. Corresponding P/S ratio are 3.39/2.75/2.3x. While the company's average P/S in the past year was around 3.1, we give Bilibili 3.5x P/S in FY2023 and a target price of $266.74 HKD. (Calculated at the exchange rate of RMB to HKD 1.16), with a “buy” rating. (Current price as of February 8)

Financial

Click Here for PDF format...