Perfect Medical Health Management (“Perfect Medical”) is a comprehensive medical beauty and medical healthcare service provider, through integrating and developing its “Medical + Beauty” operational model, offering customers safe and effective medical services. Perfect Medical has a presence throughout Hong Kong, China, Australia, Singapore and Macau. The company principally engages in the provision of providing one-stop “Medical + Beauty” services and provides a full range of services, including “Medical (Pain Management)”, “hair growth treatment”, “Gynaecological medical service”, “men's beauty and weight management”, “Medical Beauty services” and etc.

Negative impact by the Pandemic, 1HFY2023 results under pressure

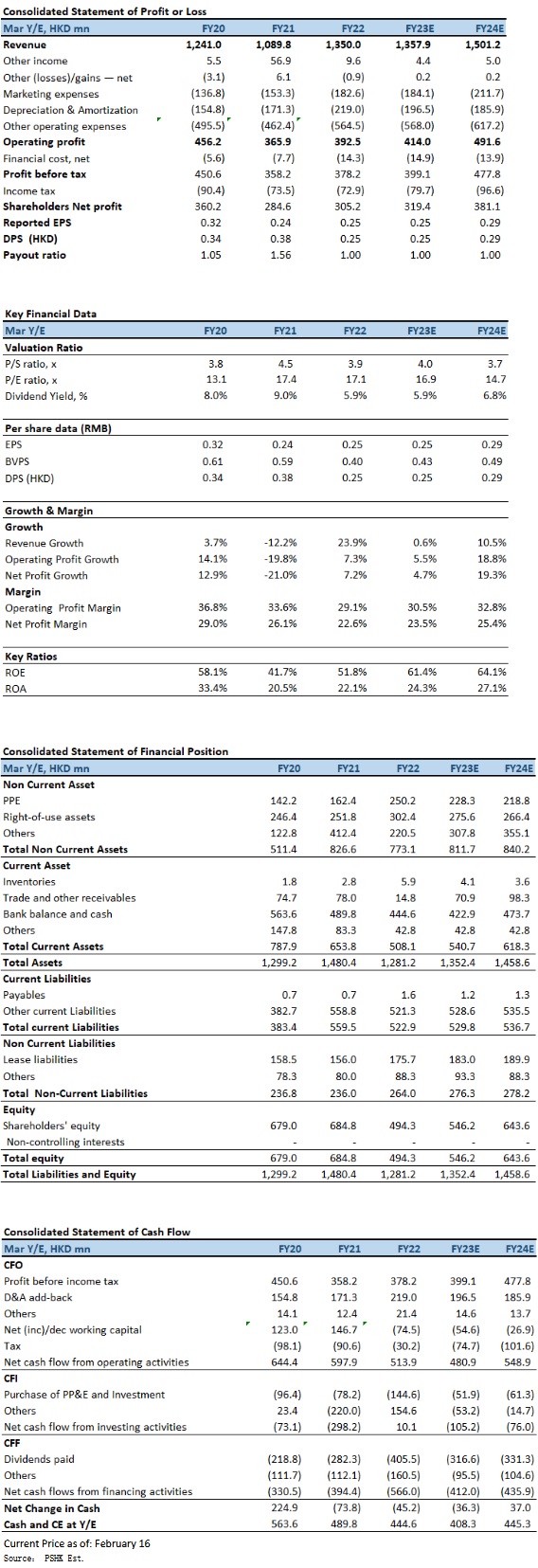

In 1HFY2023 (for the six months ended 30 September 2022), Perfect Medical's revenue decreased by 16.6% to HK$668.3mn, impacted by Covid-19 pandemic. EBITDA decreased by 25.5% to HK$229.7mn, representing the EBITDA margin of 34.4% for the period (1HFY2022: 38.4%). Profit attributable to equity holders was HK$150.7mn, dropped 30.4% YoY, representing a net profit margin of 22.5% for the period, down 4.5 percentage points YoY. Basic earnings per share was HK12.1 cents. Interim dividend of HK13.0 cents, the dividend payout ratio is 107.4%.

For the period under review, with the 5th wave of Pandemic had lingering effect in Hong Kong, together with the adverse market sentiment due to the global and local economic downturn, the overall consumption sentiment had deteriorated. The company's performance has been impacted by the slower consumption trend in Hong Kong and the return of the Pandemic in China. The softening of the company's revenue had led to a drop in net profit during the period; and mainly impacted by the Pandemic, the company had business suspension of 20 days in Hong Kong, 39 days in Macau, as well as business disruption for an average of 14 days, 23 days, 63 days and 19 days across Guangzhou, Shenzhen, Shanghai and Beijing respectively. the employee benefit expenses decreased by 3.8% to HK$230.6mn. The marketing expenses decreased substantially by 26.1% to HK$77.7mn. The rental lease related expenses increased by 11.0% at HK$87.1mn, in line with the expansion in service areas. The operating profit decreased by 31.9% and reached HK$187.0mn, representing an operating profit margin of 28.0%, down 6.3 percentage points YoY.

By regions, revenue from Hong Kong operation decreased by 21.5% to HK$492.4 million. Following the ease of the Pandemic, second quarter in Hong Kong marked a 52.1% growth in revenue QoQ. As of 30 September 2022, the company has an established network of service centres in Hong Kong covering a total of 189,000 square feet. In view of the increasing demand in the New Territories, Perfect Medical has opened an additional service centre in Yuen Long during the period to capture additional demand in the surrounding areas. Currently, revenue from Hong Kong operation accounted for 73.7% (1HFY2022: 78.3%) of the company's revenue.

Revenue from regions outside Hong Kong increased by 1.0% to HK$175.9mn (1HFY2022: HK$174.1mn), impacted substantially by the periodic suspension of business in China and Macau but compensated by the encouraging performance in both Singapore and Australia. Revenue from regions outside Hong Kong accounted for 26.3% (1HFY2022: 21.7%) of the company's revenue. As of 30 September 2022, Perfect Medical has an extensive network in China, Macau, Sydney, Melbourne and Singapore, covering a gross service area of approximately 118,000 square feet.

Investment Thesis

In China, the wide-spreading pandemic in April to May 2022 and the resurgence in several provinces and cities in September 2022 has severely disrupted the economic development in all aspects. Periodic lockdown in selected areas and the advocacy of “zero-Covid-19” policy have substantially reduced the traffic flow in shopping malls, which directly impacted on the customers visit and consumption. The company's domestic business will inevitably be affected. However, as for the aesthetic medical industry, the non-invasive aesthetic services continued to receive strong demand in China. With the benefit of a much lower penetration rate relative to other international countries, a relatively higher repeat purchase rate nature and the improving living standard in China, the high-end aesthetic medical industry is expected to grow healthily. Currently, Perfect Medical focuses on the first tier cities including Beijing, Shanghai, Guangzhou and Shenzhen, and opened three shops in strategic locations in Hong Kong, Guangzhou and Beijing during the period to strengthen the presence. In fact, as China and Hong Kong gradually resume normal life and resume normal customs clearance, and the potential influx of tourists into Hong Kong in coming years, which is expected to be conducive to the recovery of the company's business. We expect FY2023E-FY2024E EPS to be HK$0.25 and HK$0.29 respectively, with PT of HK$4.91, implies a FY2023E P/E of 19.6x (in line with industry average). Our investment rating is “Accumulate”.

Risk factors

1) Market competition intensifies; 2) Soaring in operating cost; and 3) Unexpected slowdown in service demand; 4) Tighten regulatory policies related to medical aesthetics.

�Financial

Click Here for PDF format...