The principal activities of EC Healthcare is the provision of medical and healthcare services in Hong Kong, Macau and the Mainland China. Company adopt a multi-specialist brand strategy with over 40 brands spanning across service segment of medical, aesthetic medical and beauty and wellness (represent aesthetics medical, traditional beauty, haircare and ancillary wellness services and the sale of skincare, healthcare and beauty products). As at 30 September 2022, EC Healthcare had a total of 154 service points comprising 134 in Hong Kong, 4 in Macau and 16 in Mainland China with the total aggregate g.f.a increased by 24.1% YoY to 557,000 sq. ft. Out of the net increase of 108,000 sq. ft. during the period, 69.1% came from medical business and 22.8% came from aesthetic medical and beauty and wellness services business, respectively.

Negative impact by the Pandemic, 1HFY2023 net profit margin under pressure

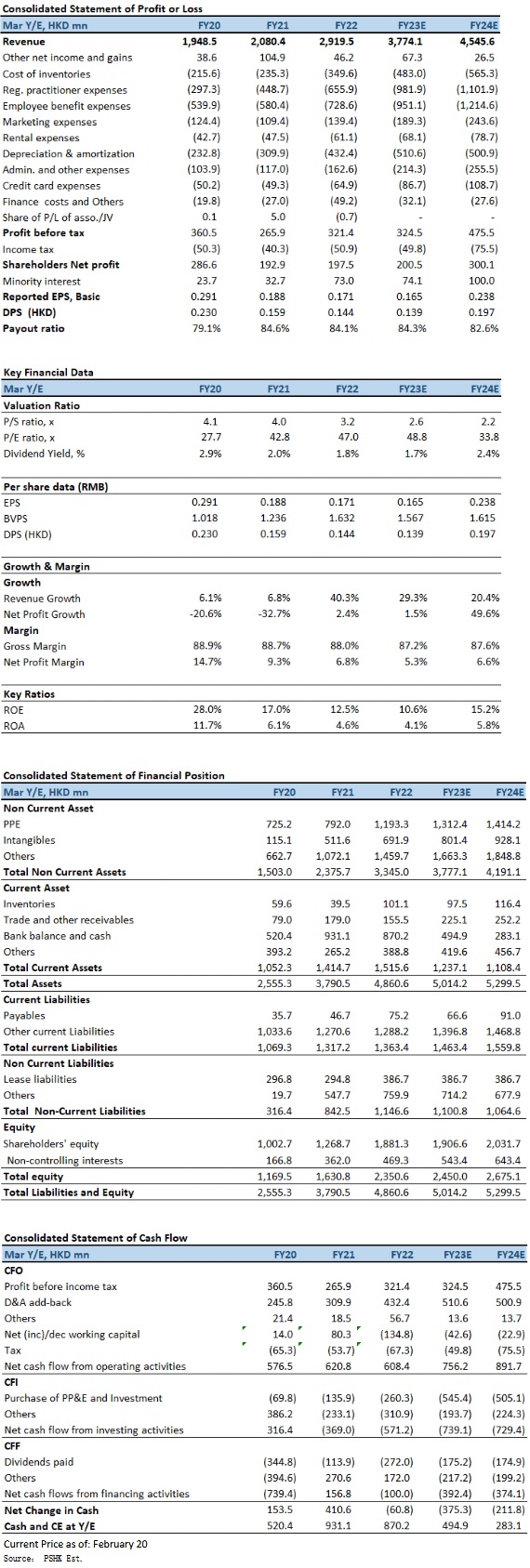

In 1HFY2023 (for the six months ended 30 September 2022), the company had revenue of HK$1,893.2mn, up 31.1% YoY. The net profit attributable to equity holders decreased by 50.0% YoY to HK$80.0 million. Basic earnings per share was HK$6.8 cents (1HFY2022: HK$14.2 cents). Interim dividend of HK$5.8 cents, the dividend payout ratio is 85.%.

For the period under review, company continues to gain market share in the healthcare services industry through both organic expansion and M&A growth. Revenue from the medical services segment rose by 47.5% YoY to HK$1,174.8mn, boosting its revenue contribution to 62.1%, of which organic expansion and M&A accounted for 90.8% and 9.2% respectively. However, revenue contributed by aesthetic medical and beauty and wellness services decreased by 2.0% YoY to HK$607.4mn, accounted for 32.1% of the total revenue. Revenue from Hong Kong recorded a slight decline of 5.4% YoY to HK$460.7mn due to 20 days of Compulsory Closure in April 2022. Revenue from Mainland China increased by 12.6% YoY to HK$89.8mn despite an average of 26 days, 10 days and 122 days of business disruption in Shenzhen, Guangzhou and Shanghai, respectively. Revenue from Macau increased slightly by 7.7% YoY to HK$56.8mn due to an average of 31 days of Compulsory Closure. Revenue from other services increased by 301.9% to HK$111.0 million, representing 5.8% of the total revenue, primarily attributable to the M&A expansion into the veterinary sector.

Increasingly intense competitive landscape, rising cost structure resulting from inflation, temporary low operation leverage of newly established service points from the previous financial year and increase in depreciation and amortisation expenses incurred from the newly acquired medical assets, EBITDA decreased by 16.6% YoY to HK$269.9mn. Due to the business disruption in Mainland China from COVID-19 and the Compulsory Closure of beauty and wellness businesses in Hong Kong and Macau, net profit margin fell by 8.0 percentage points to 5.6%.

According to the recent sales volume update announcement made by EC Healthcare, for the period from 1 October 2022 to 31 December 2022 (3QFY2023), overall Sales Volume of no less than HK$1,000mn for the Quarter, representing an increase of no less than 8% as compared with the same period last year. The Company expects an increase in Sales Volume of medical services of no less than 39% as compared with the same period last year; a decrease in Sales Volume of aesthetic medical and beauty and wellness services located in Hong Kong and Macau of no more than 17%; a decrease in Sales Volume of aesthetic medical and beauty and wellness services located in Mainland China of no more than 50%. The management stated that the decrease in aesthetic medical and beauty and wellness services was mainly due to weaker local consumer spending due to increase in outbound traveling amid the lifting of inbound quarantine restrictions; and the omicron outbreak in Mainland China.

Investment Thesis

On December 28, 2022, Hong Kong Chief Executive Lee Ka-chao announced that all social distancing measures, vaccine passes and mandatory nucleic acid testing for entry will be canceled starting on the 29 Dec. People arriving from the Mainland, Macau, Taiwan and overseas are not required to undergo mandatory nucleic acid testing upon or after arrival in Hong Kong. It is estimated that in addition to the gradual boost in local consumption sentiment in Hong Kong, the implementation of customs clearance between Hong Kong and mainland China and the recovery of potential demand for mainland tourists will bring substantial help to the company's operations. However, most of the underlying positive factors are already priced in. We expect FY2023E-FY2024E EPS to be HK$16.5 cents and HK$21.6 cents respectively, with PT of HK$6.73, implies a FY2024E P/E of 31.2x (in line with industry average). Our investment rating is “Reduce”.

Risk factors

1) Market competition intensifies; 2) Soaring in operating cost; and 3) Unexpected slowdown in service demand; 4) Tighten regulatory policies related to medical aesthetics.

Financial

Click Here for PDF format...