Company Profile

Currently, GAC's major segments cover R&D, vehicle (automobiles and motorcycles), parts, commerce services, financial services, and mobile travel service, developing a complete cycle of the automotive industry chain. By adhering to the strategy of "joint ventures + self-owned brands", the Company owns six major brands including GAC Honda, GAC Toyota, GAC Motor, GAC Aion, and GAC Mitsubishi, as well as many best-selling models. GAC currently has a market share of 9.54% in China.

Investment Summary

22's Annual Sales Volume Outperforming by +13.5% Yoy; 23Jan's Sales in-line by -38%

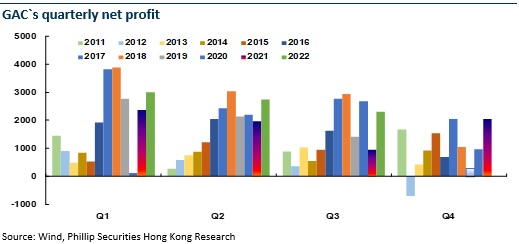

GAC's total sales volume reached 2,433.8 thousand units in 2022, up 13.5% yoy, above the industry growth rate of 9.5%, with a target completion rate of 100%. Specifically, the cumulative sale volume of new energy vehicles reached 309.5 thousand units, up 116.7% yoy.

On a closer look at brands, mainly benefiting from the excellent performance of the pure electric vehicle brand GAC Aion (up 125.7% yoy), self-owned brands displayed strong performance, with the sale volume growing by 42.6% yoy to 634 thousand units, of which new energy vehicles accounted for 43%, providing strong support for the Company's new-energy development strategy. Among the joint venture brands, GAC Toyota's sales volume rose sharply to 1,005 thousand units, up 21% yoy, exceeding 1,000 thousand units for the first time; GAC Honda, which was largely affected by the chip shortage, performed poorly, with the sales volume dropping slightly by 4.9% yoy to 742 thousand units; due to aging models, GAC Mitsubishi's sales volume was under pressure, falling substantially by 49% yoy to 33.6 thousand units for the whole year.

Due to the reduction in working days due to the early Spring Festival holiday, the aggravation of consumers` wait-and-see mentality after the expiration of the purchase subsidy at the end of last year, and the overdraft effect last year, GAC's total sales volume was 147 thousand units in January 2023, down 38.1% yoy, basically keeping pace with the broad market. The sales volume of GAC Honda, GAC Toyota, GAC Motor, GAC Aion, and GAC Mitsubishi decreased by 51%, 24%, 36%, 49%, and 69% yoy, respectively.

With a Conservative Target for 2023, the Company Will Accelerate the Launch of New Models

The Company's management expected to report a total revenue of RMB514.45 billion in 2022, up approximately 19.7% yoy, and a total profit and tax of RMB65.19 billion (by the statistical standard), up approximately 13.2% yoy. The management has given conservative guidance for sales target for 2023, aiming for a 10% yoy increase in sales volume to approximately 2,677 thousand units, continuing to grow faster than the industry average.

In terms of new models, GAC Toyota released the fifth-generation Toyota hybrid system (THS) at the Guangzhou Auto Show last year. On this basis, it plans to release and upgrade 12 products of dual-engine hybrid system in 2023 to realize the intelligent electric hybrid system of all models on the TNGA platform; its pure electric brand bZ series will have at least one new model introduced in 2023 and approximately four new models introduced in the three years by 2025.

As for GAC Honda, the Vezel, Haoying upgrade, and Honda Vezel e: HEV were launched successively during the fourth quarter of last year, and the Accord upgrade is expected to be launched in early 2023. GAC Honda e: NP1 pure electric SUV was launched in 2022. The pace of one new electric vehicle model per year will be maintained from 2023 to 2026, and the new pure electric vehicle plant will be put into operation in 2024.

There Are Still Plenty of Focus on Self-owned Brands

In line with the "XEV + ICV" dual-core driven development strategy, GAC Trumpchi plans to launch M6 upgrade, GS3 upgrade and two additional PHEV models in 2023. The new Trumpchi GS3 Shadow Speed, launched at the end of last year, is based on the Global Platform Modular Architecture (GPMA) and aims at the national market for cost-effective SUVs sold at RMB100 thousand. GAC Aion plans to launch a new B-level sedan based on the AEP3.0 platform in H1 and H2 of 2023. Its high-end brand Hyper released the second model, HyperGT, which is expected to drive the brand to develop the market for sedans sold at RMB300 thousand. In addition, the first model of the cooperation between GAC and Huawei will be mass-produced by the end of 2023. Recently, GAC Aion has completed the A-round financing. The listing process is steadily advancing, and the valuation of more than RMB100 billion shows the market confidence in its future development.

Investment Thesis

Looking ahead, after the supply chain restoration, the joint venture brands GAC Honda and GAC Toyota are accelerating the electrification layout, and the profitability is expected to improve; amid the trend of continuous increase in the penetration rate of new energy vehicles in China, self-owned brands are expected to benefit from the scale effects and continue to open up the space for growth.

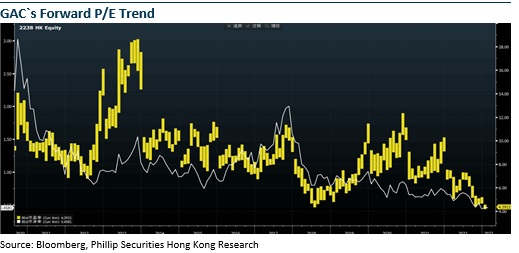

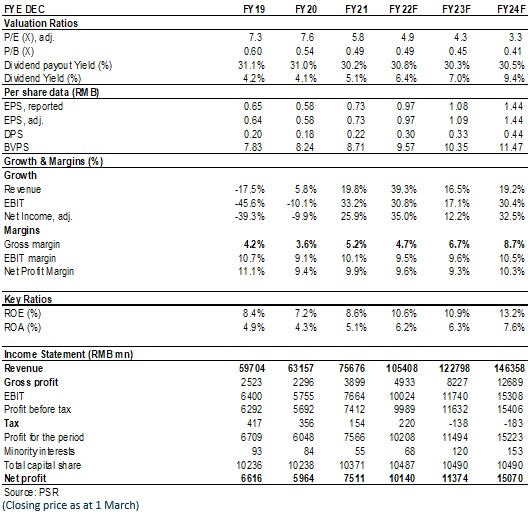

We revised the Company's 2022/2023 and introduced 2024 earnings EPS forecast to 0.97/1.08/1.44 yuan. We maintain the "Buy" rating with the target price to HKD 9.1, equivalent to 8.4/7.5/5.7x P/E and 0.85/0.79/0.71x P/B ratio in 2022/2023/2024. (Closing price as at 1 March)

Financials

Click Here for PDF format...