|

GOLDEN THROAT(6896)

Analysis:

GOLDEN THROAT (6896) is principally engaged in the manufacture and sales of throat lozenges. Its flagship product, Golden Throat Lozenges (OTC), is a type of lozenge mainly designed to relieve symptoms of sore and dry throat and hoarse voice caused by acute pharyngitis. Golden Throat Lozenges (OTC) was approved as over-the-counter medicine by the NMPA, as such they can be purchased by the public in pharmacies without requiring the prescription of a qualified medical professional. Besides being sold domestically, Golden Throat Lozenges (OTC) is also exported to the United States, Canada, Russia, the European Union, Australia, Southeast Asia, Middle East, Mexico, Mongolia and Africa, across five continents of the world. According to its positive profit alert, the Group expects an increase in profit of approximately 50% for the year ended 31 December 2022 as compared to the corresponding period in 2021. The increase in profit was mainly due to the significant increase in the Group`s annual sales in 2022. Based on the profit alert, its historical P/E is only around 5.4 times and dividend yield exceeds 10%. (I do not hold the above stock)

Strategy:

Buy-in Price: $2.28, Target Price: $2.55, Cut Loss Price: $2.13

|

HAI TIAN(603288)

Analysis:

The company is a leading condiment enterprise in China. Its main products include soy sauce, sauce, oyster sauce, cooking wine, vinegar and sauce, chicken essence, chicken powder, beancurd and other major series of more than 300 specifications, with an annual output value of more than 10 billion yuan, of which soy sauce accounts for the largest proportion, reaching 56.74%. Based on the competitive advantages of scale, R&D, channel, brand strength, etc., the soy sauce market share of the company has reached about 18%. The soy sauce industry in China is currently in the period of structural upgrading, and the industry CR3 is only 33%, so there is much room for improvement. Affected by the repeated depression of the catering industry due to the epidemic, the operating income in the first three quarters was 19.094 billion yuan, up 6.11% year on year, and the net profit attributable to the parent company was 4.667 billion yuan, down 0.86% year on year. However, short-term events do not change the company's long-term competitive advantage.

Strategy:

Buy-in Price: RMB74.00, Target Price: RMB87.00, Cut Loss Price: RMB66.00

|

|

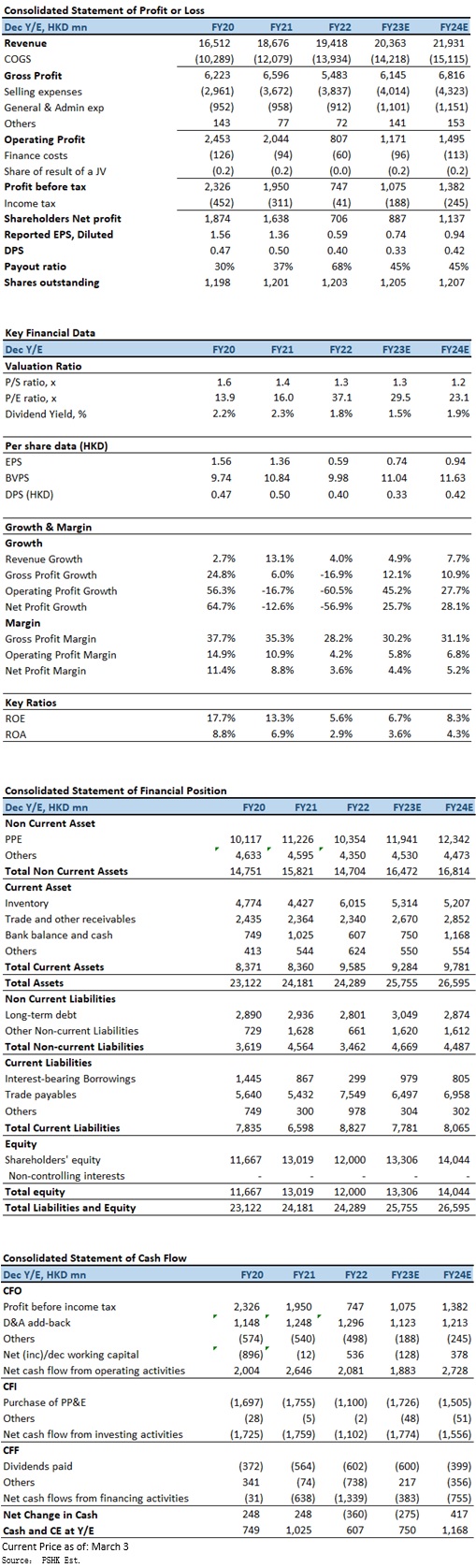

Vinda International (3331.HK) - The costs pressure is significant, sales performance remains resilience

Vinda is a leading hygiene company in Asia, with core business segments including tissue, incontinence care, feminine care, baby care and professional hygiene solution under key brands Vinda, Tempo, Tork, TENA, Dr. P, Libresse, Libero and Drypers. The cost of raw material rises and fx fluctuations, the profit margin is under pressure FY2022, total revenue increased by 4.0% (growth at constant exchange rates: 8.1%) to HK$19,418 million. Net profit declined by 56.9% to HK$706 million while the net profit margin dipped by 5.2ppts from the previous year to 3.6%. Basic earnings per share was 58.7 HK cents (FY2021: 136.5 HK cents), with a final dividend of 30 HK cents per share. Together with the interim dividend, the total dividend per share for the Year will be 40 HK cents (FY2021: 50HK cents). In 4Q2022, the quarterly revenue was HK$5,364 million, a decrease of 2.2% YoY (growth at constant exchange rates: 6.4%); the net profit was HK$19 million, a decrease of 95.2% YoY, mainly affected by Covid-19 and continuous rise of material costs. The company's profit margin was negatively impacted by continuous rise of material costs and currency fluctuation. FY2022, gross profit was down by 16.9% to HK$5,483 million, while gross profit margin down by 7.1 ppts to 28.2%. EBITDA was down by 36.1% to HK$2,104 million and the EBITDA margin declined by 6.8 ppts to 10.8%, due to lower gross margin in the year. Total foreign exchange loss amounted to HK$65.2 million (FY2021: HK$27.5 million gain). However, total sales & administrative costs as a percentage of revenue edged down by 0.4 ppt to 24.5%. In terms of business segments, revenue from tissue category amounted to HK$16,103 million, which delivered a yoy increase of 3.9% or an organic sales growth of 7.8%, representing 83% of the total revenue (FY2021: 83%). Although better pricing, better mix, and better efficiencies during the year partially offset significant increase in input cost, gross margin and segment result margin of the tissue segment dropped by 7.9 ppts and 7.2 ppts to 27.5% and 5.2%, respectively. Revenue from the personal care category increased by 4.4% to HK$3,314 million, which delivered an organic sales growth1 of 9.6% and representing 17% of the company's total revenue (FY2021: 17%) with gross margin and segment result margin of 31.7% and 2.0%, respectively. Traditional channels, key accounts managed supermarkets and hypermarkets, B2B corporate customers and e-commerce platforms accounted for 24%, 21%, 11% and 44% of revenue by sales channels, respectively. The changing consumer behavior from offline to online accelerated further and e-commerce has been the dominant sales channel with an organic growth of 16.7% year-on-year. In terms of capacity planning, the annualized designed capacity of the tissue manufacturing facilities was 1,390,000 tons at the end of the Year, including the capacity expansion of tissue production in South and East China which was to fulfil the growing market demand. In addition, Zhejiang's new plant has been put into operation in the second half of 2022, and will further improve the papermaking capacity in 2023. In terms of personal care equipment, the new headquarters of Southeast Asia in Malaysia, equipped with production facilities, warehousing and distribution equipment and modern R & D centers, it has been operated according to the plan (the first phase was put into operation in December 2022). The remaining domestic personal care facilities are located in East China, Central China and Taiwan. The macroeconomic fluctuations last year led to an unprecedented increase in the cost of raw materials. Observing the recent changes in the market, after the Spring Festival holiday, the price of wood pulp has begun to be reduced. However, in terms of supply, the import volume of piles of piles in 2022 decreased yoy. This has made the domestic supply tightening still exists, resulting the price of wood pulp may support in the high level.

Company valuation4Q2022 results may be the bottom, and the overall sales performance is still resilience. FY2023 expected to have a more obvious recovery. However, in the short term, it still depends on the price of raw materials (the price of wood pulp is still at a high level). Thus, we expect FY2023E-FY2024E EPS to HK$73.6 cents (vs HKD$1.32 in Aug-2023 report) and HKD$94.1 cent respectively, with TP HKD$14.10, implies a FY2023E P/E of 19.1x, in line with its 5-years average +1SD. Our investment rating is “Sell”. Risk factors1) wood pulp prices drop slower than expected; 2) Large fluctuations in RMB; 3) Economic recovery momentum slower than expected, consumer confidence weakens further; and 4) Industry competition is intense than expected. �Financial

Click Here for PDF format...

| Recommendation on 13-3-2023 | | Recommendation | Sell | | Price on Recommendation Date | $ 21.750 | | Suggested purchase price | N/A | | Target Price | $ 14.100 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|