Vinda is a leading hygiene company in Asia, with core business segments including tissue, incontinence care, feminine care, baby care and professional hygiene solution under key brands Vinda, Tempo, Tork, TENA, Dr. P, Libresse, Libero and Drypers.

The cost of raw material rises and fx fluctuations, the profit margin is under pressure

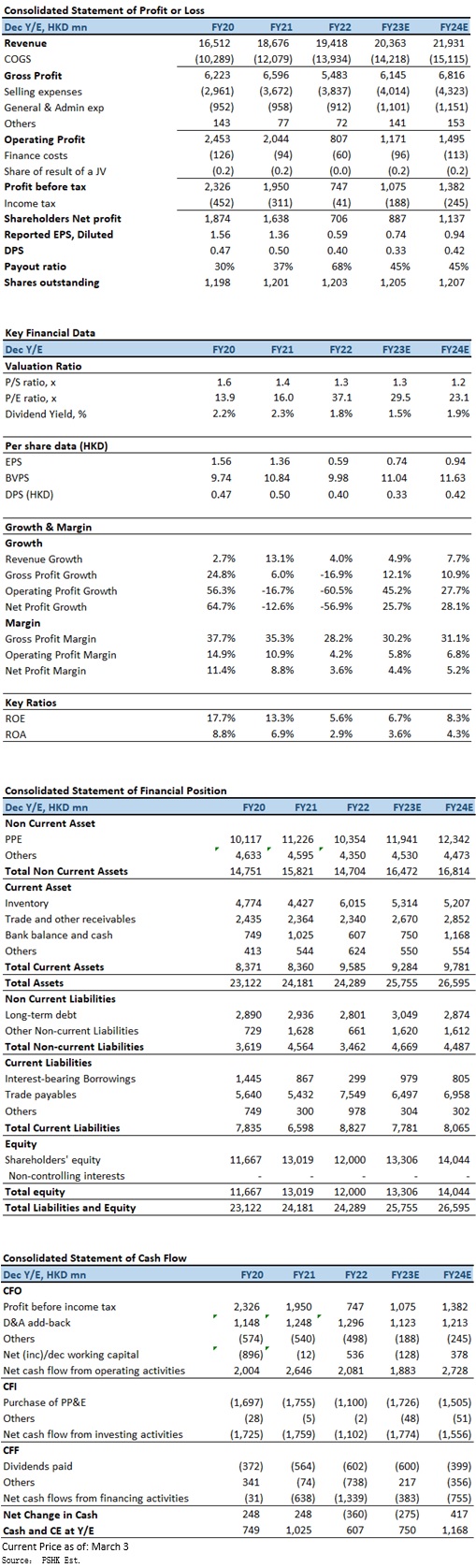

FY2022, total revenue increased by 4.0% (growth at constant exchange rates: 8.1%) to HK$19,418 million. Net profit declined by 56.9% to HK$706 million while the net profit margin dipped by 5.2ppts from the previous year to 3.6%. Basic earnings per share was 58.7 HK cents (FY2021: 136.5 HK cents), with a final dividend of 30 HK cents per share. Together with the interim dividend, the total dividend per share for the Year will be 40 HK cents (FY2021: 50HK cents).

In 4Q2022, the quarterly revenue was HK$5,364 million, a decrease of 2.2% YoY (growth at constant exchange rates: 6.4%); the net profit was HK$19 million, a decrease of 95.2% YoY, mainly affected by Covid-19 and continuous rise of material costs.

The company's profit margin was negatively impacted by continuous rise of material costs and currency fluctuation. FY2022, gross profit was down by 16.9% to HK$5,483 million, while gross profit margin down by 7.1 ppts to 28.2%. EBITDA was down by 36.1% to HK$2,104 million and the EBITDA margin declined by 6.8 ppts to 10.8%, due to lower gross margin in the year. Total foreign exchange loss amounted to HK$65.2 million (FY2021: HK$27.5 million gain). However, total sales & administrative costs as a percentage of revenue edged down by 0.4 ppt to 24.5%.

In terms of business segments, revenue from tissue category amounted to HK$16,103 million, which delivered a yoy increase of 3.9% or an organic sales growth of 7.8%, representing 83% of the total revenue (FY2021: 83%). Although better pricing, better mix, and better efficiencies during the year partially offset significant increase in input cost, gross margin and segment result margin of the tissue segment dropped by 7.9 ppts and 7.2 ppts to 27.5% and 5.2%, respectively. Revenue from the personal care category increased by 4.4% to HK$3,314 million, which delivered an organic sales growth1 of 9.6% and representing 17% of the company's total revenue (FY2021: 17%) with gross margin and segment result margin of 31.7% and 2.0%, respectively. Traditional channels, key accounts managed supermarkets and hypermarkets, B2B corporate customers and e-commerce platforms accounted for 24%, 21%, 11% and 44% of revenue by sales channels, respectively. The changing consumer behavior from offline to online accelerated further and e-commerce has been the dominant sales channel with an organic growth of 16.7% year-on-year.

In terms of capacity planning, the annualized designed capacity of the tissue manufacturing facilities was 1,390,000 tons at the end of the Year, including the capacity expansion of tissue production in South and East China which was to fulfil the growing market demand. In addition, Zhejiang's new plant has been put into operation in the second half of 2022, and will further improve the papermaking capacity in 2023. In terms of personal care equipment, the new headquarters of Southeast Asia in Malaysia, equipped with production facilities, warehousing and distribution equipment and modern R & D centers, it has been operated according to the plan (the first phase was put into operation in December 2022). The remaining domestic personal care facilities are located in East China, Central China and Taiwan.

The macroeconomic fluctuations last year led to an unprecedented increase in the cost of raw materials. Observing the recent changes in the market, after the Spring Festival holiday, the price of wood pulp has begun to be reduced. However, in terms of supply, the import volume of piles of piles in 2022 decreased yoy. This has made the domestic supply tightening still exists, resulting the price of wood pulp may support in the high level.

Company valuation

4Q2022 results may be the bottom, and the overall sales performance is still resilience. FY2023 expected to have a more obvious recovery. However, in the short term, it still depends on the price of raw materials (the price of wood pulp is still at a high level). Thus, we expect FY2023E-FY2024E EPS to HK$73.6 cents (vs HKD$1.32 in Aug-2023 report) and HKD$94.1 cent respectively, with TP HKD$14.10, implies a FY2023E P/E of 19.1x, in line with its 5-years average +1SD. Our investment rating is “Sell”.

Risk factors

1) wood pulp prices drop slower than expected; 2) Large fluctuations in RMB; 3) Economic recovery momentum slower than expected, consumer confidence weakens further; and 4) Industry competition is intense than expected.

Financial

Click Here for PDF format...