Company Profile

Spring Airlines (hereinafter referred to as the "Company") is the leader of low-cost airlines in China, founded in 2004 and based in Shanghai. It adopts a single aircraft model (i.e., the Airbus A320 family) and only offers the economy class. The Company raises its passenger load factor (P L/F) mainly by attracting travellers through its parent company, Shanghai Spring International Travel Service Ltd. (Shanghai Spring Tour), offering charter flights through its subsidiaries, and providing special fares. Meanwhile, it enhances the aircraft utilisation rate to obtain a remarkable cost advantage by optimising the route structure, prolonging flight time, and accelerating turnover.

Investment Summary

The Company Announces a Profit Warning, Resulting in an Increased Loss in Q4

Recently, the Company has disclosed its result forecast for 2022: It is expected that its net loss attributable to the parent company throughout the year will stand at RMB2.35 billion to RMB2.6 billion. In contrast, it achieved the marginal profit of RMB40 million in 2021. The loss in 2022Q4 will be RMB610 million to 860 million, which will be 24%-75% more than the figure of RMB492 million in 2022Q3 and RMB490 million to RMB740 million more than the figure of RMB120 million in 2022Q4. The main reasons lie in the strengthened pandemic control in October and November. Additionally, despite China's opening up in December, infected cases rose dramatically, inhibiting travel and posing business difficulties for the Company in the entire fourth quarter. The aircraft utilisation rate in Q4 was 4.4 hours in Q4, only higher than that in Q2. The P L/F was 74.3%.

The pandemic's influence on the civil aviation industry in 2022 exceeded expectations in both depth and continuity. Shanghai, where the main base of the Company is located, suffered from a long-term lockdown in Q2, severely impacting the Company's main business of air transport. Both daily flights and the daily utilisation rate of aircraft registered made a record low since its establishment. The Company's main business indicators fell significantly throughout 2022. Specifically, the daily utilisation rate of aircraft declined by approximately 34% yoy. The passenger traffic turnover down 34% yoy. The P L/F was 74.65%, which down 8.22ppts yoy and down 16.2ppts from 2019. The domestic and international P L/Fs were 74.8% and 57.6%, respectively.

Furthermore, increased oil prices (the import price of jet fuel up 73% in the year) and the depreciated RMB (the RMB at the end of 2022 depreciated by 9.2% from the end of 2021) also ramped up the Company's cost pressure and loss of the main business. The net profit attributable to shareholders in the first three quarters of 2022 were -RMB437million, -RMB808 million, and -RMB492 million, respectively, as previous financial statements of the Company showed.

In terms of capacity allocation, the Company adopted a conservative attitude, due to the pandemic. Throughout the year, the available passenger capacity down 26.8% yoy, down 30.55% from 2019. As at the end of 2022, the Company owned 116 aircraft, up 2.65% yoy. Spring Airlines, throughout 2022, introduced four aircraft and withdrew one, so the net increase was three, which fell greatly from the plan of introducing nine and withdrawing three aircraft at the beginning of the year. A part of the introduction plan will be postponed to 2023 or later.

Recovery is Accelerating Steadily, Performance Improvement Is Promising

Thanks to the opening up at the end of 2022, the overstocked aviation market in China has been tapped well. Meanwhile, international market demand is slowly recovering along with the lift of strict entry and exit control. According to the Ministry of Transport, civil aviation transported 1.72 million passengers during the 2023 Spring Festival travel rush, which went up by 39.8% yoy from 2022 and recovered to around 85% of the level in the same period in 2019. The traffic of the hot tourist routes to cities, such as Thailand、 Hainan, has taken the lead in recovering. Overall speaking, the volume of tourist passengers has recovered better than that of business ones.

The cumulative number of flights and passenger volume of Spring Airlines in the 2023 Spring Festival travel rush resumed to 90% and 85% of the levels in 2019, respectively. The domestic P L/F during the 10-day Spring Festival vacation was nearly 90%, while the international figure recovered to 75%. The Company's number of flights has recovered to 100% of the level in 2019 since February. However, the aircraft utilization rate is only around 70% of the level in 2019. At present, the recovery of the air passenger flow is also limited by software conditions, such as pilots and ground support. It is expected that domestic routes will recover faster than international ones. Due to the removal of bottlenecks, coupled with further demand recovery, aviation recovery is promising to expedite. The recent international oil prices and RMB exchange rates are favourable for aviation enterprises. The resilience of performance recovery of aviation companies is worth expecting. The Company boasts prominent competitiveness in sight-seeing travel and low-cost business trip, and will outperform its peers in profitability recovery.

Investment Thesis

In the past two years, Spring Airlines has exceeded the industry average in terms of capacity expansion. By virtue of its excellent cost control and operating capacity, it has snatched market shares despite headwinds. Looking ahead, through the business model of low-cost aviation, the Company is expected to keep developing the mass aviation market, and will become growingly competitive.

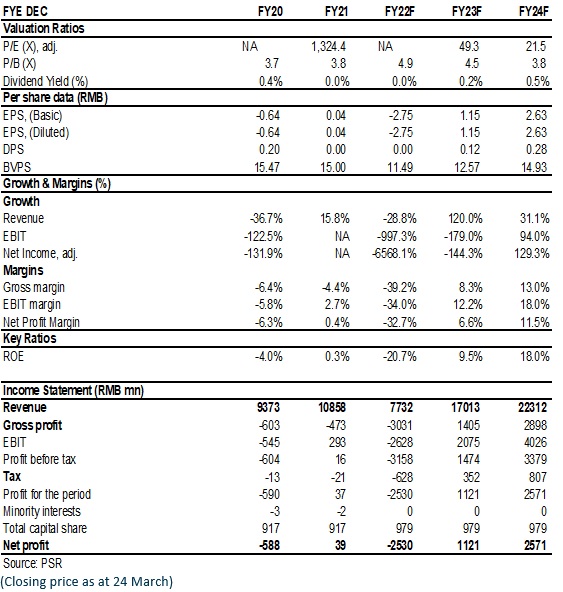

We revised the estimate for net profit for 2022/2023 and introduce forecast for 2024, respectively, with the corresponding EPS being RMB -2.75/1.15/2.63 yuan. We lift the Company's target price to RMB 68.2, respectively 24 x P/E, for 2024, a "BUY" rating. (Closing price as at 24 March)

Risk

Business cycle risk

Risk of jet fuel price fluctuation

Public health outbreak risk

Exchange rate fluctuation risk

Financials

Click Here for PDF format...