Overview

NetEase (9999.HK) is a leading internet and technology company in China. Its main business includes gaming and related value-added services. The company develop and operate a variety of popular and enduring mobile and PC games in China. Besides, NetEase's other businesses include: (2) its subsidiaries Youdao (NYSE: DAO), mainly provide technology-based intelligent learning services and products. (3) its subsidiaries NetEase Cloud Music (9899.HK), mainly provide online music service and rich music community experience. (4) its innovative businesses and others, for example the self-operated lifestyle brand NetEase Yanxuan.

A review of Q4 2022 Results

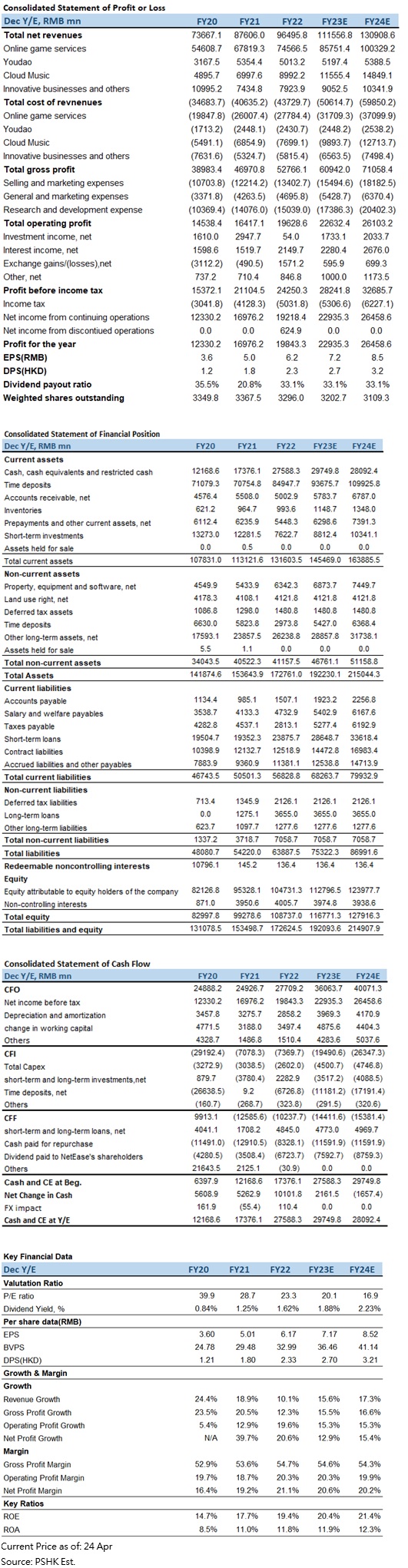

NetEase – S (9999.HK) has announced the Q4 report ended December 31, 2022. The company's revenue amounted to RMB 25354.1 million, increasing 4% YoY and increasing 3.8% QoQ. Gross profit amounted to RMB 13244.4 million, increasing 2.5% YoY but decreasing 3.6% QoQ. Gross profit margin was 52.2%, decreasing 0.8 percentage point YoY. Operating profit was RMB 4433.4 million, decreasing 6.5% YoY. Non-GAAP net profit attributable to shareholders of the company from continuing operations amounted to RMB 4811.4 million, decreasing 27.1% YoY.

Revenue by Business Type

Games and related value-added services` revenue amounted to RMB 19085.7 million, increasing 1.6% YoY and increasing 2.1% QoQ. Net revenues from the operation of online games accounted for approximately 91.8% of the segment's total net revenues for the fourth quarter of 2022, compared with 92.9% and 92.6% for the preceding quarter and the fourth quarter of 2021, respectively. Net revenues from mobile games accounted for approximately 66.4% of net revenues from the operation of online games for the fourth quarter of 2022, compared with 68.6% and 68.3% for the preceding quarter and the fourth quarter of 2021, respectively. In addition, the Games and related value-added services` gross profit margin was 59.1%, decreasing 1.8 percentage point YoY and decreasing 5.9 percentage point QoQ. The YoY and QoQ decreases were primarily attributable to the one-off recognition of royalty fees related to certain licensed games.

Yuodao's revenue amounted to RMB 1454.0 million, increasing 9.0% YoY and increasing 3.7% QoQ. The Yuodao's gross profit margin was 53.3%, increasing 2.6 percentage point YoY but decreasing 0.9 percentage point QoQ. The slight QoQ decrease was mainly due to higher revenue contribution from sales of smart devices, which carry a lower gross profit margin than learning services. The YoY increase was mainly due to improved gross margin from the sale of smart devices.

Cloud Music's revenue amounted to RMB 2376.3 million, increasing 25.8% YoY and increasing 0.8% QoQ. The Cloud Music's gross profit margin was 17.8%, increasing 13.7 percentage point YoY and increasing 3.6 percentage point QoQ. The YoY and QoQ improvements were mainly due to increased net revenues from its online music services and its social entertainment services, as well as continuously improved cost control measures.

Innovative businesses and others` revenue amounted to RMB 2438.2 million, increasing 3.4% YoY and increasing 23.9% QoQ. The Innovative businesses and others`gross profit margin were 31.5%, increasing 1 percentage point YoY and increasing 6 percentage point QoQ. The YoY and QoQ increases in innovative businesses and others` gross profit were primarily due to increased gross profit contribution from Yanxuan. In addition, the slight YoY increase was mainly due to margin improvement from Yanxuan, which was partially offset by decreased margin from advertising services.

Gaming business

Key games and previews

Eggy Party is a trendy casual competitive game launched in May 2022. The gameplay and style are relatively relaxed and joyful. It is suitable for players of all ages to play. Because it is suitable for live streaming and playing with friends, it has very high social attributes. The popularity of the game has been rising since its launch, and it is currently the game with highest number of DAUs in NetEase's history. According to data from Sensor Tower, a data research agency, Eggy Party ranked first in the download list of the world's most popular mobile games in the App Store in December last year and January this year, becoming the most downloaded game in the world. According to the list of popular games in January 2023 released by Qimai Data recently, Eggy Party surpassed Honors of Kings and Genshin Impact to win the download list for the second time; it also rose to the top five in the revenue list. According to estimates by Qimai, the game's revenue from the iPhone channel alone reached USD 22.6 million in the past month.

In terms of the monetization ability of the game, the game mainly monetizes through players buying game coins and then purchasing Battle Pass and Capsule Toy (the fashion will be drawn in the form of a lottery). The two main monetization models are able to prolong and continuously attract players to spend, and the larger the player base, the more beneficial it is to the income of Eggy Party.

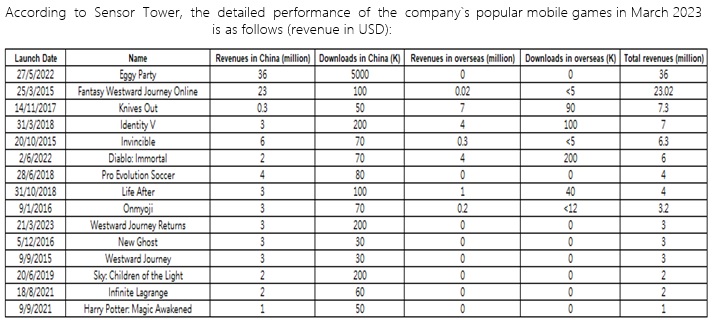

As for Diablo: Immortal, although the performance was very good at the beginning of its launch, the revenue and download of the game fell quickly. According to Sensor Tower (the data does not include third-party Android platforms in China or other places, the same below), the total domestic and overseas revenue of the game in March 2023 was USD 6 million, and the number of downloads was 270,000. The domestic data of the game is at middle to low level among NetEase's popular games. Considering that the game is an MMORPG that has been launched for less than a year and the game's brilliant performance when it was first launched, the situation is disappointing.

As for other popular games, the performance is relatively stable. It is worth noting that most of the popular games have been launched for several years. Popular overseas games such as Knives Out and Identity V have entered a mature stage, and revenue and downloads have declined as the popularity of the games has gradually declined. In addition, without Diablo Immortal, NetEase's failure to launch popular games in overseas markets in recent years is also worrying.

According to Sensor Tower, the detailed performance of the company's popular mobile games in March 2023 is as follows (revenue in USD):

In the future, NetEase is preparing to launch mobile games such as Westward Journey: Returns, Justice mobile game, Badlanders, Racing Master and Naraka: Bladepoint mobile game, as well as Harry Potter: Margic Awakened for the international markets. Many of these games are worthy of investors` attention.

Westward Journey: Returns is a lightweight idle mobile game. The game requires players to spend less time every day, which is suitable for the current environment where players` time is fragmented. Moreover, its IP “Westward Journey”is an evergreen tree of NetEase, which has brought stable income to NetEase for many years. Currently, Westward Journey: Returns has obtained the license and will open the public beta on March 2. According to the Sensor Tower, the revenue of the game in March 2023 amounted to USD 3 million, and the download amounted to 200,000. We believe that the performance of a that has been launch for less than a month is quite good, and there is still potential for further growth in revenue.

Justice is divided into a PC version and a mobile version, both of which are martial arts-themed MMORPG games with a grand open world. In terms of the PC version, the game was very popular among players in China due to its rich game elements and exquisite painting style in the early days of its launch. It has been four years since the game was launched. According to Chinese media reports, the game's fourth anniversary event earlier this year attracted 600,000 returning players. Moreover, since Blizzard Entertainment and NetEase terminated the partnership in China, the servers of Blizzard Entertainment's games, such as World of Warcraft were shut down. A large number of players who are used to playing open world MMORPGs have no similar game options in China. At this time, NetEase instructed the Justice operating team to cooperate with the World of Warcraft operating team. Referencing to the gameplay content of World of Warcraft and the game habits of players, etc., a special server called Warcraft Veteran was launched in Justice PC version. The various changes of the server have made the server highly praised in China, and nearly one million players joined it after the server opened. We believe the anniversary celebration of the PC version of Justice and the effect brought by the launch of the special server are surprising, bringing back popularity and good reputation to the IP of Justice, which will also help the mobile version of Justice to launch in the future. Besides, the PC version of Justice will launch the fourth anniversary expansion pack on June 23, which is expected to bring a new wave of popularity to the game. For the mobile version of Justice, the game has improved and added new gameplay on the basis of the PC version, which is closer to the habits of mobile players. In addition, the non-player characters (NPC) in the game will use the same underlying AI technology of ChatGPT. We expect that the mobile version will bring freshness to players, rather than simply porting the PC version to mobile. According to Chinese media reports, the total cost of the mobile version of Justice reached 600 million in June last year, reflecting that NetEase attaches great importance to this game. At present, the game has obtained the license and is scheduled to be tested on June 30. The number of reservations on the official website of the game has reached about 18.33 million (as of March 7). We believe that this game may be the most important game to NetEase in this year based on factors such as its gameplay and reputation. Investors should pay high attention to the performance of the game after its launch. If it performs well, it may become a catalyst for the stock price to rise.

Badlanders is a survival shooting mobile game, and its gameplay is slightly different from Tencent's PUBG: Mobile (long-term in the top ten global mobile games) and Knives Out. It is expected that this game will not directly seize the Chinese market of PUBG: Mobile. At present, the number of reservations on the game's official website has reached about 10.84 million (as of March 7), but the time for the public beta has not yet been determined. Although there are a lot of pre-orders for the game, since the game has already been launched in Taiwan and other overseas regions in January 2022, and the performance is not satisfactory, we do not have much expectation for the performance of this game after it is launched, and we suggest investors to wait and see the overall performance of the game after it is launched in the mainland.

Naraka: Bladepoint mobile game has not yet confirmed the public beta date. We consider that the game has a very good reputation on the PC version. It is the first domestic buyout game with global sales exceeding 10 million. In addition, the martial arts-style action-adventure battle royale game is suitable for playing on mobile phone. We believe that the response of the game after its launch is good, which is worth looking forward to by investors.

Harry Potter: Margic Awakened overseas version (Europe, America, Japan and other markets) still has no exact public beta date. According to the data survey agency Wikimili, Harry Potter ranks tenth among the 50 most profitable IPs in the world in 2021, with a total revenue of about USD 32.2 billion. The data shows that IPs are very popular in the world, with potential income. NetEase's game caused a boom when it was launched in China. According to Sensor Tower, as of October 2022, the cumulative revenue of the game in the China, Hong Kong and Taiwan markets alone has reached USD 358 million, ranking second in the Harry Potter series of games. We believe that since this IP is relatively popular in markets such as Europe, America and Japan, if the game is launched in these markets, it has good revenue potential.

Overseas game business

According to mainland statistics data platform Youxituoluo, NetEase has established a total of 7 overseas game studios since 2019. In recent years, NetEase has invested in a number of game-related businesses, such as the acquisition of Quantic Dream, a well-known French game developer who has produced a number of 3A (meaning high-investment and high-quality) games in 2022, and the acquisition of Canadian game studio SkyBox Labs in January 2023. This studio has cooperated with some large game studios such as Xbox Game Studios, including world-renowned games such as Minecraft. In addition, NetEase brought many well-known game designers under its umbrella in 2022, such as Hiroyuki Kobayashi (producer of some games in the Resident Evil series (with a total global sale of more than 100 million sets), and Nagoshi Toshihiro (producer of Like a Dragon series, the series has sold more than 14 million copies worldwide). NetEase is supporting global development through the acquisition of studios and talents with excellent capabilities. Although it may take several years to produce high-quality games and may not even create revenue in the short term. In the long run, it will be of great help to NetEase's reputation and the development of overseas markets.

In addition, NetEase established an overseas game studio called Spliced in February 2023. According to internal media reports, the studio's goal is to create world-class online games with original IP. It is currently recruiting personnel with experience in 3A games and large-scale games with a scale game of more than 100 people. Team members have participated in the development of world-renowned games such as GTA and Call of Duty.

Since Activision Blizzard announced the termination of the partnership with NetEase in November last year, all Chinese servers of Activision Blizzard's games have been closed. The relevant revenue only accounted for a low single digit of NetEase's total revenue, the impact on NetEase's revenue was quite slight. Moreover, Diablo Immortal is operated in the form of an independent contract and will not be affected by the termination of cooperation. We believe that the possibility of future cooperation between NetEase and Activision Blizzard is very low. NetEase has lost the potential development opportunity to develop the world-renowned IP in the hands of Blizzard.

The mainland re-examines the value of the game industry

In recent months, the state-owned media from China has published two articles calling for not to ignore the value of science and technology behind the game industry, believing that the game industry can help other related technology industries develop and cultivate high-level scientific and technological talents in the fields of computer science and artificial intelligence, and enhance the international influence of the industry. We believe these remarks are very positive to the game industry, which means that the policy risk of the industry is gradually reducing, and at the same time improving market expectations. However, in terms of the tighten limits for young online gamers, since it involves youth development and other issues that the Chinese government attaches great importance to, we don`t think there will be any relaxation.

Youdao business overview

Since the implementation of a series of policies aimed at students` extracurricular learning, such as double reduction policy, basically eliminate most of the K12 (elementary, junior high and high school education) extracurricular fee-based learning services, and this kind of online and offline education service model for multiple students with one teacher often has low fixed costs and is in high demand in the mainland. It can bring very large revenue growth and higher gross profit margin to the company, but due to changes in mainland policies, this has seriously affected Youdao's original business layout, revenue expectations, and gross profit margin. Currently, most of Youdao's courses are free supply.

Currently, Youdao's main income comes from learning-related smart hardware, such as Youdao dictionary pens. At present, the price of Youdao Dictionary Pen English Learning Translator II (Professional Edition) is about HKD 1200 in Hong Kong. The sales target of the product is relatively affluent groups in China. We believe that the fixed cost of selling this kind of smart hardware is relatively high, the gross profit margin is not as good as that of learning services, and the number of customer groups is limited. We expect Youdao's revenue will only record a slight increase as the national disposable income rises.

�Cloud Music overview

The Cloud Music business is growing well. The company has continuously signed copyright cooperation agreements with well-known domestic and foreign music labels to enrich the music tracks in the content library and develop differentiated communities. In addition, due to the company's changes in pricing measures, in 2022, the number of MAUs increased by 3.7% to 189.4 million, while the number of monthly paying users of online music services increased by 32.2% to 38267.1 thousand. The number of monthly paying users of social entertainment services increased by 95% to 1332.3 thousand, while the monthly revenue per paying user of online music services fell slightly by 1.5% to RMB 6.6. The monthly revenue per paying user of social entertainment services fell by 27.2% to RMB 326.0. Besides, due to the expansion of business scale and the optimization of copyright cost structure, the company's gross profit margin continued improve.

NetEase Yanxuan overview

NetEase Yanxuan is a boutique e-commerce platform that targets the new middle class in the mainland (annual income over RMB 150,000 or household income over RMB 200,000). The products of NetEase Yanxuan's brands are all directly supplied by first-line brand manufacturers, and they need to pass the inspection of global authoritative inspection agencies before they can put on the shelves. However, due to the ODM form of production, the platform only participates in the design and phased acceptance process, and the key raw materials and core production processes of the product rely on third parties, making it difficult to fully control the product quality. At present, the company does not have its own logistics team, and the products are mainly delivered through SF Express. All products provide 30-day returns and 2 working days for quick refunds. Since 2020, the company announced its withdrawal from the Double 11 E-commerce War, saying that Double 11 advocated excessive consumption and digital carnival for sales, and then the platform's positioning has shifted to brand building, promoting rational consumption, and avoiding competition with other e-commerce platforms in terms of traffic and price. In addition, the company will launch a sub-brand NetEase Tiancheng in September 2022, focusing on the mid-to-high-end pet market. According to iResearch's 2021 White Paper on China's Pet Consumption Trend, the scale of China's pet industry will reach RMB 445.6 billion in 2023, with a CAGR 10.51% from 2020 to 2023, of which pet food accounts for 40% of the entire pet industry chain. In addition, the survey shows that the average domestic pet owner has 1.8 types of pets, of which dogs account for 70% and cats account for 56%, which means cats and dogs are the main types of domestic pets. We believe that as the number of pet owners increases, domestic demand for high-quality pet food will rise, and the mid-to-high-end domestic pet food market has growth potential. NetEase Tiancheng can enjoy the industry growth by developing the market. Overall, since JD.com launched the “10 billion subsidy” plan, we are worried that these traffic-dependent e-commerce platforms will have a new round of price wars and it eventually negatively affect their gross profit margin, while high-quality e-commerce companies such as NetEase Yanxuan have brand effects and are less affected by price wars. Moreover, with the advent of China's post-epidemic era, revitalizing the economy and increasing domestic demand will become the main axis of China's development in 2023. A clearer political and economic environment is expected to increase citizens` consumer confidence, and consumption upgrades will benefit the development of boutique e-commerce.

Valuation and recommendation

We believe that the Chinese game industry has entered a recovery period. The regularization of game license approval will continue to benefit game companies including NetEase, and the successive release of games with license approval will benefit the income of many game companies. As for NetEase's launch of several key games this year, it may become a catalyst for the stock price. In addition, NetEase's continuous investment in overseas excellent studios and talents will benefit NetEase in the long run. We predict that the company's net profit growth rate in FY2023-2024 will be 12.9% and 15.4% respectively. The net profit per share attributable to shareholders of the company will be RMB 7.17 and RMB 8.52 respectively in FY2023-2024 respectively. Corresponding P/E are 20.1/16.9x, and NetEase's three-year average P/E is around 30.3, we believe that the company's key new games will be launched one after another and the performance of Eggy Party will drive revenue growth, giving NetEase 22x PE in 2023 and a target price of 179.8 HKD (calculated at the exchange rate of RMB to HKD 1.14), with a “buy” rating. (Current price as of Apr 24)

�

Risk factors

The performance of new games is worse than expected or launch date is delayed / the game-related regulatory policies are tightened

Financial

Click Here for PDF format...