Company Profile

Geely is one of the leading enterprises in China's self-brand passenger vehicles manufacturers. The Company's products include six major brands: Geely, Geometry, Lynk, Zeekr, Livan, and Galaxy, covering the A0 to B-class passenger vehicles market.

Investment Summary

The High Revenue Growth Is Attributed to the Rise in Single Vehicle Prices of Zeekr

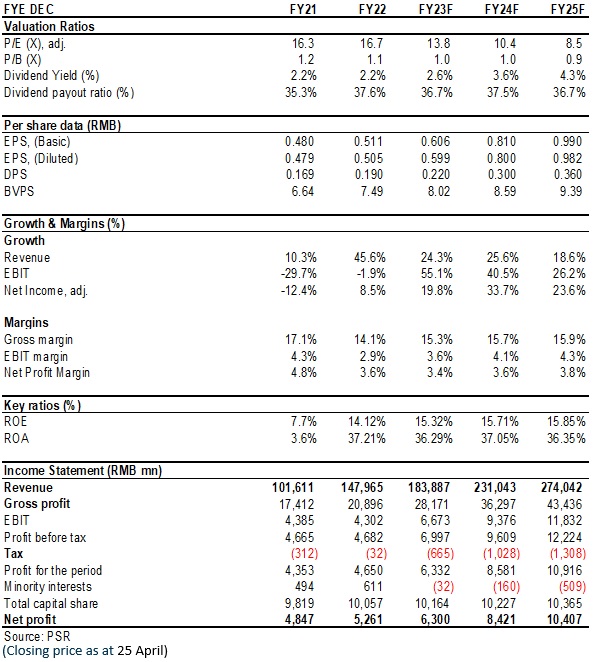

According to the recently released FR2022 result, Geely reported a gross revenue of RMB148 billion, up 45.6% yoy, exceeding market expectation of RMB132.4 billion (Bloomberg consensus). It recorded a net profit attributable to shareholders of RMB5.26 billion, up 8.5% yoy, higher than market expectation of RMB4.82 billion. The EPS was RMB0.505, slightly lower than our previous estimate of RMB0.53. The dividend per share was HK$0.21, unchanged from the previous year.

In 2022, Geely's sales volume totalled 1,430 thousand units, up 8% yoy. Specifically, the sales volume in the domestic market increased 2% to 1,230 thousand units, while the export sales volume surged 72% to 198 thousand units. Benefiting from the average sales price of Zeekr exceeding RMB336 thousand, the average sales revenue from single vehicles grew by 30% year-on-year, reaching RMB103 thousand (excluding Ruilan Auto and Lynk & Co), driving the Company's overall revenue growth to be much higher than the sales volume growth.

The Profitability Is Largely Affected by Only the New Energy Transformation Cost

Total gross margin decreased by 3 ppts to 14.1%, mainly due to rising raw material costs and higher new energy transformation cost in the initial stage. The Company's NEV sales volume increased by 300% year-on-year to 329 thousand units, and the proportion climbed by 16.7 ppts to 22.9% from 6.2% in the same period last year. The low gross profit of new energy vehicles in the initial transformation affected the overall gross margin. In 2022, Zeekr contributed to revenue of approximately RMB31.8 billion and a consolidated loss of RMB1.38 billion.In terms of expenses, the administrative expense ratio and sales expense ratio decreased by 0.8 ppts and 0.6 ppts, respectively. Due to the increased R&D investment in intelligentisation and electrification, the R&D expenses increased by 22.6% to RMB6.77 billion, of which RMB1.97 billion or 29% was expensed. Capital expenses in 2022 were RMB10.3 billion (RMB6.1 billion in 2021), exceeding the RMB9.2 billion budgeted at the beginning of the year, mainly due to higher R&D investment to accelerate the transformation to new energy and intelligentisation. The Company's capital expense budget for 2023 is RMB14 billion. With the Company's comprehensive transformation to new energy, R&D investment will continue to increase. Amid the new energy and intelligentisation, the competition in the industry will continue to intensify. It is expected that the Company's R&D expenses will continue to grow rapidly in the next few years.

The Company Launches Geely Galaxy to Restart the New Energy Strategy

In February 2023, the Company officially released Geely Galaxy, a new NEV brand for the mid-to-high-end auto market, which covers NEV products at different ends and further improves the ladder distribution of products jointly with its low-end band Geometry and high-end brand Zeekr. Geely Galaxy will launch seven new products within two years, including four intelligent PHEVs and three intelligent EVs, of which L7 and L6 will be delivered in Q2 and Q3 of 2023, and E8 will be delivered in Q4 of 2023. Geely Galaxy will build independent sales channels, adopt a combination of direct user system and an agency distribution model, and introduce new experience and service standards. We believe that Geely Galaxy is a solid move to restart the new energy strategy by the Company after continuous trial and error and adjustment in new energy vehicles, which is expected to increase Geely's share of mid-end NEVs in the market.

Looking forward to 2023, the Company will launch ten models, including three Galaxy models (L7, L6 and E8), one Geometry model (Panda Mini) and one Geely model (code name: G426); two Zeekr models (Zeekr X and a pure electric sedan); two Lynk & Co models (Lynk & Co 08 SUV and a plug-in hybrid sedan); and a Ruilan SUV (Ruilan 7). The Company has set a sales target of 1,650 thousand units, of which the sales target for Zeekr is 140 thousand units. The NEV sales volume increases from 328 thousand units to 650 thousand units, accounting for 40%.

Investment Thesis

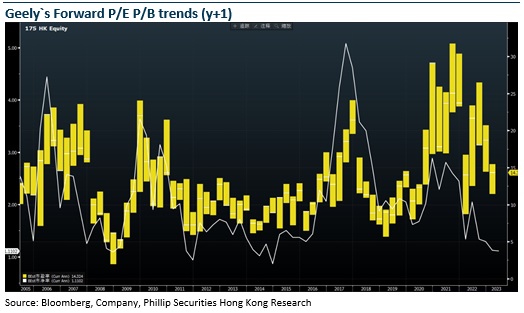

We revised our financial forecast and target price to HK$12.9, equivalent to 18.7/14/11.4x P/E ratio in2023/2024/2025, and we give the rating of Buy. (Closing price as at 25 April)

Financials

Click Here for PDF format...