Sectors:

Air & Automobiles (Zhang Jing),

TMT, Food(Elvis Kwok)

Automobile & Air (ZhangJing)

This month I released updated reports of Geely (175.HK).

According to the released FY2022 Result, Geely reported a gross revenue of RMB148 billion, up 45.6% yoy, exceeding market expectation of RMB132.4 billion (Bloomberg consensus). It recorded a net profit attributable to shareholders of RMB5.26 billion, up 8.5% yoy, higher than market expectation of RMB4.82 billion. The EPS was RMB0.505, slightly lower than our previous estimate of RMB0.53. The dividend per share was HK$0.21, unchanged from the previous year.

In 2022, Geely's sales volume totalled 1,430 thousand units, up 8% yoy. Specifically, the sales volume in the domestic market increased 2% to 1,230 thousand units, while the export sales volume surged 72% to 198 thousand units. Benefiting from the average sales price of Zeekr exceeding RMB336 thousand, the average sales revenue from single vehicles grew by 30% year-on-year, reaching RMB103 thousand (excluding Ruilan Auto and Lynk & Co), driving the Company's overall revenue growth to be much higher than the sales volume growth.

Total gross margin decreased by 3 ppts to 14.1%, mainly due to rising raw material costs and higher new energy transformation cost in the initial stage. The Company's NEV sales volume increased by 300% year-on-year to 329 thousand units, and the proportion climbed by 16.7 ppts to 22.9% from 6.2% in the same period last year. The low gross profit of new energy vehicles in the initial transformation affected the overall gross margin. In 2022, Zeekr contributed to revenue of approximately RMB31.8 billion and a consolidated loss of RMB1.38 billion.

Looking forward to 2023, the Company will launch ten models, including three Galaxy models (L7, L6 and E8), one Geometry model (Panda Mini) and one Geely model (code name: G426); two Zeekr models (Zeekr X and a pure electric sedan); two Lynk & Co models (Lynk & Co 08 SUV and a plug-in hybrid sedan); and a Ruilan SUV (Ruilan 7). The Company has set a sales target of 1,650 thousand units, of which the sales target for Zeekr is 140 thousand units. The NEV sales volume increases from 328 thousand units to 650 thousand units, accounting for 40%.

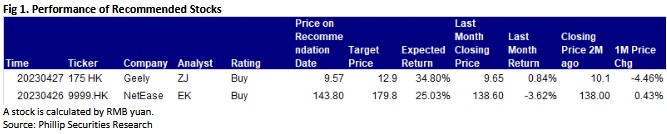

We revised our financial forecast and target price to HK$12.9, equivalent to 18.7/14/11.4x P/E ratio in2023/2024/2025, and we give the rating of Buy.

TMT, Food (Elvis Kwok)

This month I released one report, NetEase (9999.HK).

NetEase (9999.HK) is a leading internet and technology company in China. Its main business includes gaming and related value-added services. The company develop and operate a variety of popular and enduring mobile and PC games in China. Besides, NetEase's other businesses include: (2) its subsidiaries Youdao (NYSE: DAO), mainly provide technology-based intelligent learning services and products. (3) its subsidiaries NetEase Cloud Music (9899.HK), mainly provide online music service and rich music community experience. (4) its innovative businesses and others, for example the self-operated lifestyle brand NetEase Yanxuan.

A review of Q4 2022 Results

NetEase – S (9999.HK) has announced the Q4 report ended December 31, 2022. The company's revenue amounted to RMB 25354.1 million, increasing 4% YoY and increasing 3.8% QoQ. Gross profit amounted to RMB 13244.4 million, increasing 2.5% YoY but decreasing 3.6% QoQ. Gross profit margin was 52.2%, decreasing 0.8 percentage point YoY. Operating profit was RMB 4433.4 million, decreasing 6.5% YoY. Non-GAAP net profit attributable to shareholders of the company from continuing operations amounted to RMB 4811.4 million, decreasing 27.1% YoY.

Gaming business Key games and previews

Eggy Party is a trendy casual competitive game launched in May 2022. The gameplay and style are relatively relaxed and joyful. It is suitable for players of all ages to play. Because it is suitable for live streaming and playing with friends, it has very high social attributes. The popularity of the game has been rising since its launch, and it is currently the game with highest number of DAUs in NetEase's history. According to data from Sensor Tower, a data research agency, Eggy Party ranked first in the download list of the world's most popular mobile games in the App Store in December last year and January this year, becoming the most downloaded game in the world. According to the list of popular games in January 2023 released by Qimai Data recently, Eggy Party surpassed Honors of Kings and Genshin Impact to win the download list for the second time; it also rose to the top five in the revenue list. According to estimates by Qimai, the game's revenue from the iPhone channel alone reached USD 22.6 million in the past month. In the future, NetEase is preparing to launch mobile games such as Westward Journey: Returns, Justice mobile game, Badlanders, Racing Master and Naraka: Bladepoint mobile game, as well as Harry Potter: Margic Awakened for the international markets. Many of these games are worthy of investors` attention.

Valuation and recommendation

We believe that the Chinese game industry has entered a recovery period. The regularization of game license approval will continue to benefit game companies including NetEase, and the successive release of games with license approval will benefit the income of many game companies. As for NetEase's launch of several key games this year, it may become a catalyst for the stock price. In addition, NetEase's continuous investment in overseas excellent studios and talents will benefit NetEase in the long run. We predict that the company's net profit growth rate in FY2023-2024 will be 12.9% and 15.4% respectively. The net profit per share attributable to shareholders of the company will be RMB 7.17 and RMB 8.52 respectively in FY2023-2024 respectively. Corresponding P/E are 20.1/16.9x, and NetEase's three-year average P/E is around 30.3, we believe that the company's key new games will be launched one after another and the performance of Eggy Party will drive revenue growth, giving NetEase 22x PE in 2023 and a target price of 179.8 HKD (calculated at the exchange rate of RMB to HKD 1.14), with a “buy” rating. (Current price as of Apr 24)

Risk factors

The performance of new games is worse than expected or launch date is delayed / the game-related regulatory policies are tightened

Click Here for PDF format...