|

ZOOMLION(1157)

Analysis:

Within the framework of the overall strategies of “equipment manufacturing + Internet” and “industry + finance”, Zoomlion Heavy Industry Science and Technology (1157) is accelerating the development of and the overall arrangement for engineering machinery, agricultural machinery + intelligent agriculture and Zoomlion New Materials. In the area of engineering machinery products, the competitiveness of the three key products of the Company (i.e. concrete machinery, engineering cranes and construction cranes) is increasing continuously and the positions of the three key products on the market are solid. In the area of potential business opportunities, the layout of the manufacturing of its earthmovers features bases in Weinan and Changsha. The whole demonstrative intelligent plant manufacturing excavators in Changsha went into operation. The reliability and intelligent technologies of its medium and large excavators are upgraded in an all-round way. Its market share increases continuously. In the area of agricultural machinery, the Company has completed the construction of “dual headquarters” in Changsha and Wuhu, focused on the development of new products of staple food grain machinery, expanded the product catalogue and facilitated the digitalisation, intelligentisation and eco-friendliness of our products. Its wheat harvesters, grain dryers, rotary tillers and rice seedling planting throwers remain at the top of the list of domestic market share. In the area of new building materials, the Company is building an industrial chain featuring “intelligent manufacturing lines + new building materials + construction equipment + construction methods”, promoting the standardisation and modularisation of dry mortar mixers, facilitating the progress of making dry mortar mixers in China, completing the design of the standard plan of the manufacturing lines of dry mortar mixers. In the area of “industry + finance”, the Company has completed the acquisition of Road Rover. Road Rover was among early birds engaged in automotive navigation, intelligent cockpits and Internet of Vehicles in China. Road Rover was also one of the earliest partners of the Baidu Apollo project aiming to build an autonomous driving platform. The main products of Road Rover are various kinds of products related to intelligent cockpits, AI-assisted driving and Internet of Vehicles, intelligent navigation solutions and autonomous driving solutions. (I do not hold the above stock)

Strategy:

Buy-in Price: $4.55, Target Price: $5.00, Cut Loss Price: $4.35

|

AVICHINA(2357)

Analysis:

For the year ended 31 December 2022, AviChina Industry & Technology Company Limited (02357) recorded a revenue of RMB63,639 million, representing an increase of 5.54% as compared with the corresponding period of the preceding year, which was mainly attributable to the growth of revenue of aviation ancillary system and related business. The R&D expenses amounted to RMB4,442 million, representing an increase of 28.68% yoy. The R&D expenses accounted for 6.98% of the total revenue, representing an increase of 1.25 percentage points as compared with that in the corresponding period of the preceding year. The operating profit in 2022 was RMB5,190 million, representing a decrease of 1.37% yoy, which was mainly attributable to the decrease in results of AVICOPTER PLC, a subsidiary of the Company, and the increase in expenses during the year. The net profit attributable to the owners of the parent company for the year 2022 amounted to RMB2,216 million, representing a decrease of 6.46%. The main reasons are that, on the one hand, the decrease in results of AVICOPTER resulted in a year-on-year decline in its net profit attributable to the company; on the other hand, the enhanced R&D inputs by the company resulted in an increase in the R&D expenses and other expenses,the net profit attributable to the owner of the parent company decreased year-on-year. By business segment, revenue derived from the aviation entire aircraft business for 2022 was RMB20,302 million (accounted for 31.90% of the total revenue, representing a decrease of 1.91 percentage points), representing a decrease of 0.42% yoy. The above revenue includes: the revenue derived from the helicopter business, which amounted to RMB17,491 million, representing a decrease of 0.99%, and accounted for 86.15% of the total revenue of the aviation entire aircraft business; the revenue derived from the trainer aircraft business, which amounted to RMB2,517 million, representing an increase 5.71%, and accounted for 12.40% of the total revenue of the aviation entire aircraft business; the revenue derived from the general purpose aircraft business, which amounted to RMB294 million, representing a decrease of 13.78%, and accounted for 1.45% of the total revenue of the aviation entire aircraft business. The gross profit margin of the Group's aviation entire aircraft business for the year 2022 was 11.47%, representing an increase of 4.49 percentage points, which was mainly attributable to the adjustment of helicopter products structure during the year.Revenue derived from the aviation ancillary system and related business for the year 2022 was RMB36,591 million (accounted for 57.50% of the total revenue, representing an increase of 2.47 percentage points), representing an increase of 10.28%. Among the above revenue, the revenue derived from avionics business amounted to RMB25,852 million, representing an increase of 19.98%, and accounted for 70.65% of the total revenue of the aviation ancillary system and related business. The gross profit margin of the aviation ancillary system and related business for the year 2022 was 29.86%, representing a decrease of 0.88 percentage point.The revenue derived from the aviation engineering services business for the year 2022 was RMB6,746 million (accounted for 10.60% of the total revenue, representing a decrease of 0.56 percentage point), representing an increase of 0.28%. The gross profit margin of the aviation engineering services was 16.77%, representing an increase of 0.78 percentage point.In 2022, company officially entered the Tibetan plateau emergency rescue market with the successful delivery of the first AC312E helicopter to Tibet Himalaya General Airlines Co., Ltd. Tianjin Helicopter Company Limited obtained the AC312E helicopter production license, speeding up the construction of Tianjin helicopter industry base. The advanced medium-sized multi-purpose helicopter AC352 obtained the type certificate, filling the gap in China's helicopters spectrum. We made new progress in the construction of aviation emergency rescue system with the successful maiden flight of the large multi-purpose helicopter AC313Aand the completion of the helicopter rope-landing operation standard verification flight of the AC311A helicopter. The AC332 helicopter completed all design tests before the first flight. The first domestic S-300C helicopter officially delivered and successfully entered the domestic general aviation market.In 2023, although facing the challenges of global industrial chain adjustment and restructuring, and the global economy is facing downward pressure. The company stated that it will continue to take "high-quality development" as its theme, make efforts to promote scientific and technological self-reliance and self-improvement, accelerate the construction of aviation products, grasp the opportunity of the development of aviation emergency rescue equipment, increase the development and production of emergency rescue equipment, and promote the long-term development of helicopter business.

Strategy:

Buy-in Price: $4.35, Target Price: $4.60, Cut Loss Price: $4.13

|

|

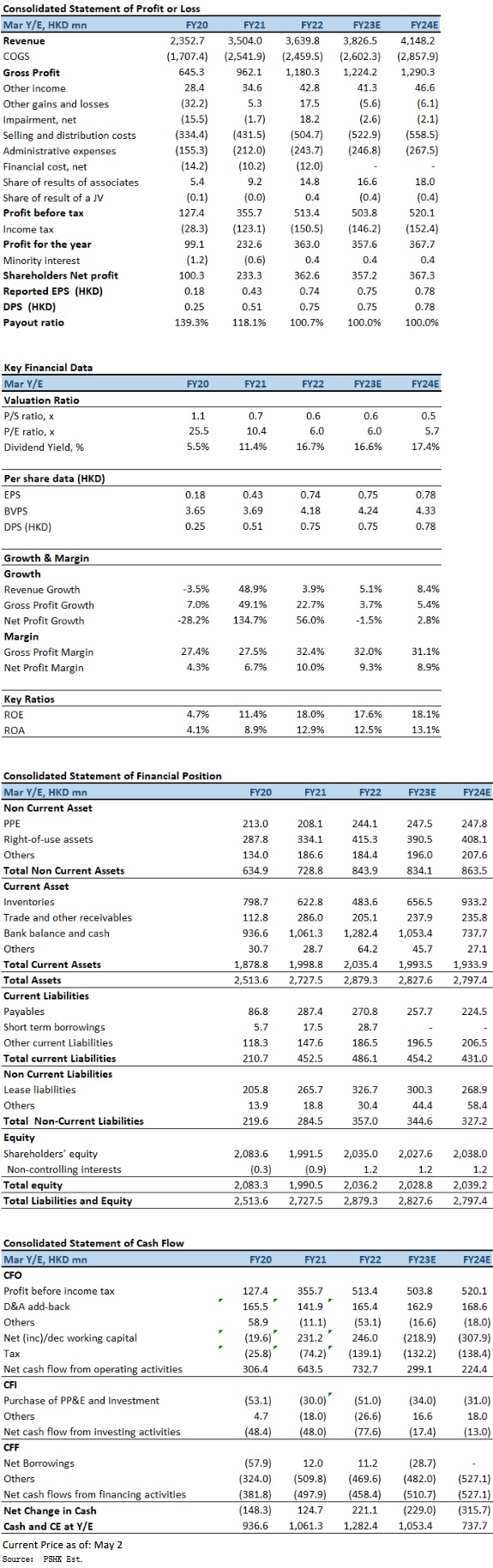

Oriental Watch Holdings Limited (398.HK) - HK operation outperformed the market, Conservative spending on high-end luxury goods become a concern

Oriental Watch Holdings Limited (Oriental Watch) that founded in 1961, has developed an extensive retail shop network in the Greater China area, and has become one of the largest watch retailers. Company carries around a hundred prestigious brands, in particular, famous Swiss brands such as Rolex, Tudor, Piaget, Vacheron Constantin, IWC, Jaeger-LeCoultre, Girard Perregaux, Longines, Omega, etc. Company operates a total of 12 shops in HK SAR and Macau SAR, including Oriental Watch Company, La Suisse Watch Company, Rolex and Tudor Boutique and Breitling Boutique. In 2004, company expanded its watch retail business to Mainland China. Since then, company has opened a number of outlets and boutiques covering various cities in Mainland, China. Subsequently, company has further expanded its businesses to Taiwan region. As at 30 September 2022, company operates 44 retail points (including associate retail stores) in the Greater China region, and 1 online store in each of the Mainland China and HK respectively. HK operation outperformed the market with revenue increased by 6.1% In 1HFY2023 (for the six months ended 30 September 2022), company's revenue decreased by 10.0% yoy to HK$1,674 million, which was mainly attributable to the decrease in revenue in the Mainland China market as a result of business interruptions due to such lockdown policy and restrictions. In line with the decrease in revenue, gross profit decreased by 6.9% to HK$537 million, with gross profit margin increased by 1.1 percentage points to 32.1%, and profit attributable to owners of the company decreased by 9.6% to HK$151 million. Basic EPS were 31.03 HK cents, down 9.2% yoy. Interim dividend of 7.8 HK cents per share (1HFY2022: 8.6 HK cents per share) and a special dividend of 23.5 HK cents per share (1HFY2022: 25.8 HK cents per share). During the Period, the company's aggregated expenses related to leases increased slightlyby 5.3% to HK$80 million, accounting for 23.1% of the overall operating expenses (1HFY2022: 22.2%). The increase was mainly due to the lease renewal of retail stores which command a relatively higher rental rate. In Hong Kong, the COVID-19 pandemic situation has been under control since the first quarter of 2022. Yet, clouded by market uncertainty, the market sentiment remained cautious with the value of total retail sales decreased by 1.3% yoy during the first nine months of the year. However, sales of jewelry, watches and clocks, and valuable gifts recorded a slight increase of 0.2% during the same period. Despite the uncertain retail market sentiment, Hong Kong operation still outperformed the market with revenue increased by 6.1% to HK$504 million for the period, accounting for 30.1% of the overall revenue, segment profit increased by 81.8% to HK$42.75 million. According to the National Bureau of Statistics, the PRC's gross domestic product (GDP) has recorded a 0.4% yoy growth and 3.9% yoy growth in the second and third quarter respectively, which grew at a softer pace compared with the same period of last year. The slowdown of economic growth was attributable to the widespread lockdown as well as the weakening market sentiment. Sales of gold, silver and jewelry also recorded a decrease of 0.8% yoy from April to September 2022. According to the Federation of the Swiss Watch Industry FH, the Swiss watch exports to the PRC during the Period decreased 13.7% yoy to CHF1,267.3 million, showcasing the country's conservative sentiment on purchasing luxury watches. Due to the economic condition as well as the temporary business suspension mentioned above, revenue from Mainland China operation decreased by 15.4% to HK$1,101 million, accounting for 65.8% of the overall revenue, segment profit decreased by 23% to HK$189.86 million. Investment ThesisLooking ahead, although China and Hong Kong have entered the road to normal after the epidemic, with the uncertainty from the increase in interest rate, and the management also expects consumers to become more conservative in consumption, especially on purchasing of high-end luxury goods. Hence, the business will be under some pressure over the upcoming periods. We expect FY2023-FY2024 EPS to be 74.62 HK cents and 78.10 HK cents respectively, with PT of HKD5.14, implies a FY2023E P/B of 1.21x (~1-yrs historical average plus 1 SD). Our investment rating is “Accumulate”. Risk factors1) Economic recovery momentum is slowing down; 2) Operating costs are higher than expected; 3) Luxury goods consumption is lower than expected. �Financial

Click Here for PDF format...

| Recommendation on 5-5-2023 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 4.490 | | Suggested purchase price | N/A | | Target Price | $ 5.140 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|