|

SINOTRUK(3808)

Analysis:

SINOTRUK (3808) is principally engaged in the manufacture and sale of heavy duty trucks, light duty trucks, buses and engines. With regard to the heavy duty trucks segment, the Group adheres to innovative development, caters to market demand, and accelerates the optimization and upgrade of products and structure adjustment, and achieves comprehensive breakthroughs in market segments. With regard to the light duty trucks segment, the Group continuously optimizes its product structure and achieves breakthroughs in key market segments. Firstly, the sales volume and market shares of vehicles of 2.0L, 2.3L, 2.5L are significantly improved, with vehicles of 2.0L and 2.5L gradually forming sales support; secondly, the Group achieves continuous breakthroughs in featured products, steadily increases sales volume of special vehicles and new energy products, and makes strong efforts in promoting products such as refrigerated trucks, wreckers, environmental sanitation vehicles and hazardous chemical transport vehicles, resulting in continuous growth of their market shares; and thirdly, the products` ranking in regional markets keeps rising. With regard to the engines segment, the Group keeps enhancing the competitiveness of existing engine products, increasing investment in new energy technologies, and constructing various advanced power parts and components platforms, to satisfy the needs of different products of finished vehicles including HDTs, LDTs and construction machine. The Group also constantly optimizes the fuel consumption of engines, increases the fuel thermal efficiency and decreases the fuel consumption per hundred kilometers through measures such as combustion system optimization and accessory electrification, striving to enhance the market competitiveness of finished vehicle products. Looking forward, as the social economy gradually returns to normal, the rebound in demand after the market being oversold and the accelerated growth of fixed asset investment will drive stable growth in demand for its products. Additionally, the natural renewal needs brought by the huge vehicle ownership and increased proportion of China VI Emission Standard vehicles and new energy vehicle ownership in terms of policies, etc. will bring new increments to industry demand. (I do not hold the above stock)

Strategy:

Buy-in Price: $13.40, Target Price: $14.80, Cut Loss Price: $12.70

|

CHINA EDU GROUP(839)

Analysis:

China Education Group (00839) is a provider of vocational education services, and is committed to developing more high-quality skilled professionals and enhancing the core competencies of vocational schools by cultivating a "dual-qualified" teaching workforce, establishing open regional academia-industry practice centers, expanding student development pathways, and innovating international exchange and cooperation mechanisms.The company revenue reached RMB2,775 million for the six months ended 28 February 2023, up 18.0% yoy. Net profit was decreased by 14.2% to RMB1,036 million. The drop in net profit was mainly attributable to the fair value gain on convertible bonds of RMB318 million recognised for the six months ended 28 February 2022 while no such gain recognised during the current reporting period. After adjusting for the foreign exchange gain/loss, share-based payments, imputed interest on deferred cash considerations, fair value change on convertible bonds, current period expenses related to conversion of independent colleges into private universities and fair value change on construction cost payables for school premises, the adjusted EBITDA was increased by 19.1% to RMB1,676 million; the adjusted net profit was increased by 16.7% to RMB1,104 million; The adjusted net profit attributable to owners of the Company was increased by 15.1% to RMB1,045 million. Revenue from higher vocational education segment increased 20.6% to RMB2,348 million. The significant increase in revenue of higher vocational education institutions was mainly driven by the growth in student enrollment and revenue per student of higher vocational education institutions. Revenue from secondary vocational education segment decreased slightly 3.0% to RMB320 million. The decrease in revenue of secondary vocational education segment was due to a decrease in the number of students enrolled. The number of new students in certain schools has declined because of the prevention measures and social restrictions of coronavirus disease 2019. Although such restrictions have been relieved, the new student enrollments of these schools have not yet instantly and completely recovered. Revenue from global education segment increased 44.6% to RMB107 million. The significant increase in revenue of global education segment was mainly driven by the increase in the number of new students after the travel bans resulted from coronavirus disease 2019 were lifted in February 2022.In April 2022, the National People's Congress passed the newly amended Vocational Education Law, which explicitly expresses that the government encourages, instructs and supports enterprises and other social forces in organising vocational schools, requires governments at all levels to incorporate the development of vocational education into national economic and social development plans, and encourages financial institutions to support the development of vocational education by providing financial services.In 2021/22, the scale of higher and vocational education in China expanded continuously. The Central Committee of the CPC and the State Council has implemented the policy of "stabilising employment" and "ensuring employment" by extending the length of education received by and improving the education level of the labour force. The vocational education college entrance examination has been implemented tentatively in various provinces, aiming to establish a comprehensive system for cultivating application-oriented talents covering secondary vocational schools, junior colleges, vocational education undergraduates, application-oriented education undergraduates and postgraduates with professional degrees. As the restrictions imposed overseas during the outbreak of pandemic gradually ease, China Education Group will seize the opportunity arising from the growth in international students market by launching new campus in Australia in due course.In the post pandemic era, based on the demand of core technology autonomy and industrial upgrading, certain frontier industries and specialties will face a large talent gap, with greater demand for application-oriented and professional higher education and secondary vocational education resources, and China Education Group as private education has a great potential.

Strategy:

Buy-in Price: $7.60, Target Price: $8.41, Cut Loss Price: $6.93

|

|

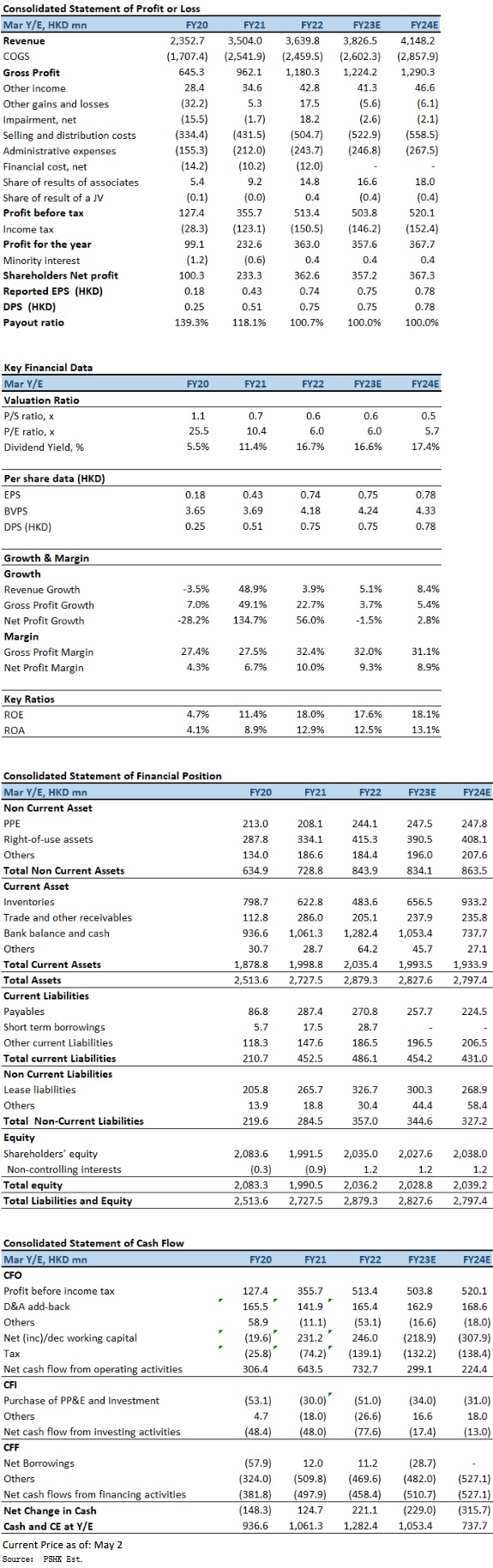

Oriental Watch Holdings Limited (398.HK) - HK operation outperformed the market, Conservative spending on high-end luxury goods become a concern

Oriental Watch Holdings Limited (Oriental Watch) that founded in 1961, has developed an extensive retail shop network in the Greater China area, and has become one of the largest watch retailers. Company carries around a hundred prestigious brands, in particular, famous Swiss brands such as Rolex, Tudor, Piaget, Vacheron Constantin, IWC, Jaeger-LeCoultre, Girard Perregaux, Longines, Omega, etc. Company operates a total of 12 shops in HK SAR and Macau SAR, including Oriental Watch Company, La Suisse Watch Company, Rolex and Tudor Boutique and Breitling Boutique. In 2004, company expanded its watch retail business to Mainland China. Since then, company has opened a number of outlets and boutiques covering various cities in Mainland, China. Subsequently, company has further expanded its businesses to Taiwan region. As at 30 September 2022, company operates 44 retail points (including associate retail stores) in the Greater China region, and 1 online store in each of the Mainland China and HK respectively. HK operation outperformed the market with revenue increased by 6.1% In 1HFY2023 (for the six months ended 30 September 2022), company's revenue decreased by 10.0% yoy to HK$1,674 million, which was mainly attributable to the decrease in revenue in the Mainland China market as a result of business interruptions due to such lockdown policy and restrictions. In line with the decrease in revenue, gross profit decreased by 6.9% to HK$537 million, with gross profit margin increased by 1.1 percentage points to 32.1%, and profit attributable to owners of the company decreased by 9.6% to HK$151 million. Basic EPS were 31.03 HK cents, down 9.2% yoy. Interim dividend of 7.8 HK cents per share (1HFY2022: 8.6 HK cents per share) and a special dividend of 23.5 HK cents per share (1HFY2022: 25.8 HK cents per share). During the Period, the company's aggregated expenses related to leases increased slightlyby 5.3% to HK$80 million, accounting for 23.1% of the overall operating expenses (1HFY2022: 22.2%). The increase was mainly due to the lease renewal of retail stores which command a relatively higher rental rate. In Hong Kong, the COVID-19 pandemic situation has been under control since the first quarter of 2022. Yet, clouded by market uncertainty, the market sentiment remained cautious with the value of total retail sales decreased by 1.3% yoy during the first nine months of the year. However, sales of jewelry, watches and clocks, and valuable gifts recorded a slight increase of 0.2% during the same period. Despite the uncertain retail market sentiment, Hong Kong operation still outperformed the market with revenue increased by 6.1% to HK$504 million for the period, accounting for 30.1% of the overall revenue, segment profit increased by 81.8% to HK$42.75 million. According to the National Bureau of Statistics, the PRC's gross domestic product (GDP) has recorded a 0.4% yoy growth and 3.9% yoy growth in the second and third quarter respectively, which grew at a softer pace compared with the same period of last year. The slowdown of economic growth was attributable to the widespread lockdown as well as the weakening market sentiment. Sales of gold, silver and jewelry also recorded a decrease of 0.8% yoy from April to September 2022. According to the Federation of the Swiss Watch Industry FH, the Swiss watch exports to the PRC during the Period decreased 13.7% yoy to CHF1,267.3 million, showcasing the country's conservative sentiment on purchasing luxury watches. Due to the economic condition as well as the temporary business suspension mentioned above, revenue from Mainland China operation decreased by 15.4% to HK$1,101 million, accounting for 65.8% of the overall revenue, segment profit decreased by 23% to HK$189.86 million. Investment ThesisLooking ahead, although China and Hong Kong have entered the road to normal after the epidemic, with the uncertainty from the increase in interest rate, and the management also expects consumers to become more conservative in consumption, especially on purchasing of high-end luxury goods. Hence, the business will be under some pressure over the upcoming periods. We expect FY2023-FY2024 EPS to be 74.62 HK cents and 78.10 HK cents respectively, with PT of HKD5.14, implies a FY2023E P/B of 1.21x (~1-yrs historical average plus 1 SD). Our investment rating is “Accumulate”. Risk factors1) Economic recovery momentum is slowing down; 2) Operating costs are higher than expected; 3) Luxury goods consumption is lower than expected. �Financial

Click Here for PDF format...

| Recommendation on 8-5-2023 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 4.490 | | Suggested purchase price | N/A | | Target Price | $ 5.140 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|