|

WEICHAI POWER(2338)

Analysis:

WEICHAI POWER (2338) is primarily engaged in the manufacturing and sale of engines, automobiles and automobile components, agricultural equipment (including agricultural machineries and agricultural vehicles) and forklift trucks, as well as the provision of intelligent logistics services (including warehousing technology and supply chain solution). In the area of power system, the Group continues to enhance its products . Its large-diameter high-speed engine products continues to make contribution with their high-quality and high-performance in markets such as data centre, ocean fishing and official vessel, resulting in rapid growth in sales volume of such products. In the area of commercial vehicle, the Group implements the leading strategy with complete vehicles and machineries, accelerates the coordination of resources and upgrade of the industrial chain structure, and continuously enhances the competitiveness of its products. In the area of agricultural equipment, the Group focuses on businesses of intelligent agricultural machinery and intelligent agriculture, continuously increases investment in technological research and development, to promote the transformation from a traditional agricultural machinery equipment manufacturer to a service provider of intelligent agricultural science and technology system. In the area of intelligent logistics, KION Group AG, an overseas controlling subsidiary of the Company, is a globally leading supplier in the area of intralogistics. KION assists factories, warehouses and distribution centres to optimise their materials flow and information flow through the design, establishment and improvement of logistics solutions in over a hundred countries and regions around the world. With regard to new business, against the backdrop of the national strategy of carbon peak and carbon neutrality, the Group has implemented the new development concept to actively offer Weichai`s solutions and opened up a new path for diversified energy transformation, focusing on electric-powered powertrain system business and exploring the new hydrogen energy track. Looking forward, under the influence of favorable factors such as macroeconomic growth and rebound of the freight market, the commercial vehicle industry is expected to gradually climb out of the bottom and see a momentum of recovery, while the sales volume of heavy trucks is expected to increase significantly. Factors such as escalated infrastructure investment, the gradual implementation of the “stabilising the real estate market” policy, and recovered demand in the export market are favorable for the development of the construction machinery industry. In the first quarter of 2023, the Group`s achieved revenue of RMB53.434 billion, representing an increase of 18.25% as compared to the same period last year. Net profit attributable to shareholders of listed company grew 68.3% to RMB1.855 billion. (I do not hold the above stock)

Strategy:

Buy-in Price: $12.80, Target Price: $14.40, Cut Loss Price: $12.00

|

INTRON TECH(1760)

Analysis:

Intro-tech is a provider of automotive electronic solutions in China, specializing in key automotive electronic components such as new energy, body control, safety, and powertrain systems. The company was established in 2001 and listed on the Hong Kong Stock Exchange in 2018. Based on the grasp of market prospects and trends, the company's business focus has expanded from traditional automotive electronic applications (body control, safety, and power transmission) to new energy business since 2009. In 2015, it also entered emerging application fields such as intelligent vehicles. The company mainly purchases chips from outside, uses its own engineering research and development, adds its own software or algorithms, and then sells them to the outside world, including BMS, VCU, MCU, And autonomous driving domain controller, intelligent gateway, LiDAR, high-precision sensor module. The company's customers include customer clusters in the automotive and industrial fields, such as well-known OEM manufacturers such as BYD, BAIC, and Changan, as well as industrial customers such as Inspur Information, Huazhong CNC, and Horizon. The company's customers are relatively scattered and have strong bargaining power with downstream manufacturers. Through specialized research and development and solution design, it effectively reduces the technical barriers for small and medium-sized automobile manufacturers. As of the end of 2021, the company had 1234 customers.According to the FY2022 result, benefiting from the rapid growth of the overall domestic new energy vehicle market, the company's operating revenue increased by 52% year-on-year to 4.8 billion yuan. The year-on-year growth rates of new energy/body systems/safety systems/power systems/intelligent driving internet connectivity/cloud servers/service provision businesses were+91%/+50%/+34%/+40%/+151%/-24%/+92%, respectively. Benefiting from the improvement of structure and ASP, the company's annual gross profit margin has increased from 19.7% in 2021 to 21.5%. Due to the scale effect caused by revenue expansion, operational efficiency has improved, and the overall expense ratio has significantly decreased. The net profit has increased by 105% year-on-year to 410 million yuan, and the net profit margin has increased from 6.3% in 2021 to 8.5%.Due to the rapid iteration of industry technology, the company has always adhered to building a technological moat through research and development investment, forming a rapid iteration capability. The company has a large number of technical R&D personnel and software engineers. As of the end of 2022, the number of R&D personnel has increased by 31% to 916, accounting for 67% of the total number of employees. R&D investment has increased by 61% year-on-year; The number of patents and software copyrights has also continued to grow, with a total of 235 patents and 187 software copyrights as of the end of 2022, an increase of 64 and 45 respectively compared to the previous year.Intro-tech established a strategic partnership with Infineon as early as 2005, and established a mutually beneficial partnership with Infineon through deep binding. Intro-tech is the largest distributor of Infineon's Greater China automotive sector, and Infineon is the largest supplier of Intro-tech, accounting for over 80% of the company's total procurement volume. In 2020, Intro-tech and Horizon reached a strategic partnership for the first time. Starting from 2021, they collaborated to launch the car grade AI chip Journey 5 and completed two solutions based on Journey 5. The company's software platform is committed to solving common functional components on one hand, and on the other hand, it focuses on compatibility across processor platforms and system functional support across applications. The company has currently completed the deployment on platforms such as Infineon, Horizon, and Xinchi, and applied it to the development of autonomous driving, internet connectivity, and some regional controller product projects, with the hope of further increasing market penetration.We expect that in the next 2-4 years, benefiting from the rapid growth of the new energy vehicle market, the company's operating revenue growth rate will maintain a high growth rate of over 30%, and net profit may record a growth rate higher than revenue.

Strategy:

Buy-in Price: $4.85, Target Price: $5.90, Cut Loss Price: $4.20

|

|

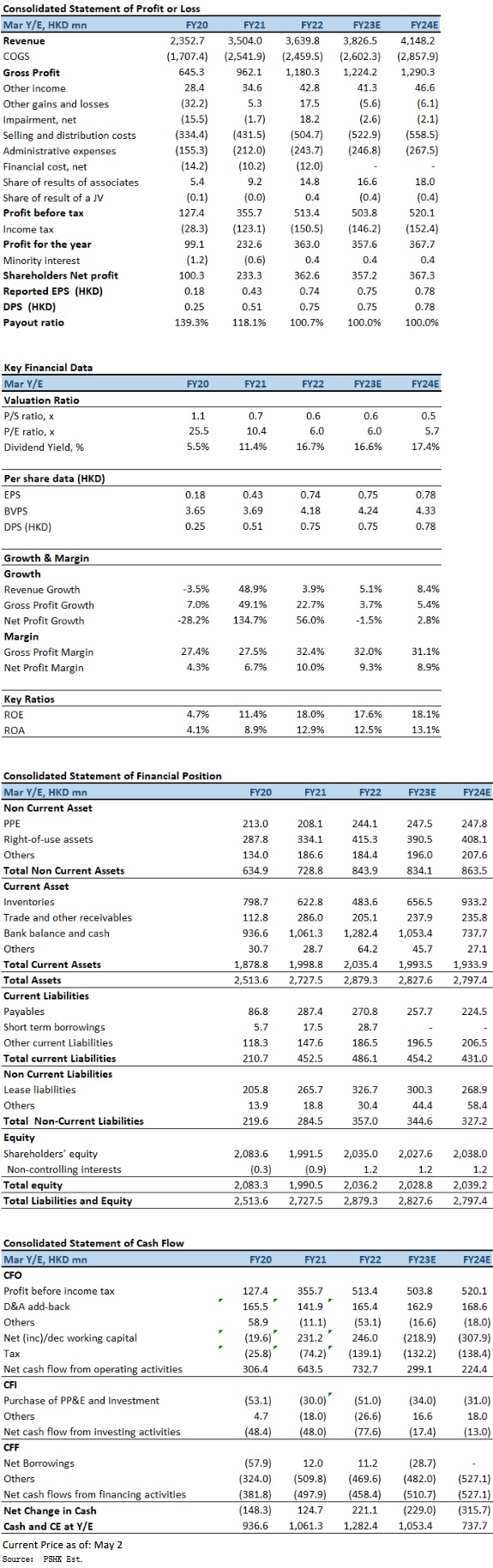

Oriental Watch Holdings Limited (398.HK) - HK operation outperformed the market, Conservative spending on high-end luxury goods become a concern

Oriental Watch Holdings Limited (Oriental Watch) that founded in 1961, has developed an extensive retail shop network in the Greater China area, and has become one of the largest watch retailers. Company carries around a hundred prestigious brands, in particular, famous Swiss brands such as Rolex, Tudor, Piaget, Vacheron Constantin, IWC, Jaeger-LeCoultre, Girard Perregaux, Longines, Omega, etc. Company operates a total of 12 shops in HK SAR and Macau SAR, including Oriental Watch Company, La Suisse Watch Company, Rolex and Tudor Boutique and Breitling Boutique. In 2004, company expanded its watch retail business to Mainland China. Since then, company has opened a number of outlets and boutiques covering various cities in Mainland, China. Subsequently, company has further expanded its businesses to Taiwan region. As at 30 September 2022, company operates 44 retail points (including associate retail stores) in the Greater China region, and 1 online store in each of the Mainland China and HK respectively. HK operation outperformed the market with revenue increased by 6.1% In 1HFY2023 (for the six months ended 30 September 2022), company's revenue decreased by 10.0% yoy to HK$1,674 million, which was mainly attributable to the decrease in revenue in the Mainland China market as a result of business interruptions due to such lockdown policy and restrictions. In line with the decrease in revenue, gross profit decreased by 6.9% to HK$537 million, with gross profit margin increased by 1.1 percentage points to 32.1%, and profit attributable to owners of the company decreased by 9.6% to HK$151 million. Basic EPS were 31.03 HK cents, down 9.2% yoy. Interim dividend of 7.8 HK cents per share (1HFY2022: 8.6 HK cents per share) and a special dividend of 23.5 HK cents per share (1HFY2022: 25.8 HK cents per share). During the Period, the company's aggregated expenses related to leases increased slightlyby 5.3% to HK$80 million, accounting for 23.1% of the overall operating expenses (1HFY2022: 22.2%). The increase was mainly due to the lease renewal of retail stores which command a relatively higher rental rate. In Hong Kong, the COVID-19 pandemic situation has been under control since the first quarter of 2022. Yet, clouded by market uncertainty, the market sentiment remained cautious with the value of total retail sales decreased by 1.3% yoy during the first nine months of the year. However, sales of jewelry, watches and clocks, and valuable gifts recorded a slight increase of 0.2% during the same period. Despite the uncertain retail market sentiment, Hong Kong operation still outperformed the market with revenue increased by 6.1% to HK$504 million for the period, accounting for 30.1% of the overall revenue, segment profit increased by 81.8% to HK$42.75 million. According to the National Bureau of Statistics, the PRC's gross domestic product (GDP) has recorded a 0.4% yoy growth and 3.9% yoy growth in the second and third quarter respectively, which grew at a softer pace compared with the same period of last year. The slowdown of economic growth was attributable to the widespread lockdown as well as the weakening market sentiment. Sales of gold, silver and jewelry also recorded a decrease of 0.8% yoy from April to September 2022. According to the Federation of the Swiss Watch Industry FH, the Swiss watch exports to the PRC during the Period decreased 13.7% yoy to CHF1,267.3 million, showcasing the country's conservative sentiment on purchasing luxury watches. Due to the economic condition as well as the temporary business suspension mentioned above, revenue from Mainland China operation decreased by 15.4% to HK$1,101 million, accounting for 65.8% of the overall revenue, segment profit decreased by 23% to HK$189.86 million. Investment ThesisLooking ahead, although China and Hong Kong have entered the road to normal after the epidemic, with the uncertainty from the increase in interest rate, and the management also expects consumers to become more conservative in consumption, especially on purchasing of high-end luxury goods. Hence, the business will be under some pressure over the upcoming periods. We expect FY2023-FY2024 EPS to be 74.62 HK cents and 78.10 HK cents respectively, with PT of HKD5.14, implies a FY2023E P/B of 1.21x (~1-yrs historical average plus 1 SD). Our investment rating is “Accumulate”. Risk factors1) Economic recovery momentum is slowing down; 2) Operating costs are higher than expected; 3) Luxury goods consumption is lower than expected. �Financial

Click Here for PDF format...

| Recommendation on 10-5-2023 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 4.490 | | Suggested purchase price | N/A | | Target Price | $ 5.140 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|