|

SINOFERT(297)

Analysis:

In the face of a complex and changing market environment, SINOFERT (297) insists on staying ahead by innovation, focusing on the implementation of key strategies such as differentiation and industry quality improvement and efficiency enhancement. At the same time, it continues to promote the strategic transformation of biofertilizer + soil health to improve the nutrient utilization rate of chemical fertilizers, reduce carbon emission and promote healthy soil development through R&D and innovation. In the first quarter of 2023, the turnover and net profit of the Group were approximately RMB6,605 million and RMB491 million, respectively. The net profit of the Group increased by approximately 19% as compared with that for the three months ended 31 March 2022, mainly due to the Group`s unwavering efforts to implement the strategic transformation of biofertilizer + soil health, which promoted the continued growth in the sales volume of differentiated product mix and led to a steady increase in the gross profit and net profit. The “No. 1 Central Document for 2023” has clearly defined the basic direction of green development of agriculture in terms of policy framework, accelerated the agricultural input reduction, promoted application of efficiency enhancement technologies and facilitated fertigation in order to drive the overall transformation of the fertilizer industry, which has brought significant opportunities for strategic transformation of the Group. (I do not hold the above stock)

Strategy:

Buy-in Price: $1.12, Target Price: $1.26, Cut Loss Price: $1.07

|

KWEICHOW MOUTAI(600519)

Analysis:

Kweichow Moutai is a landmark enterprise in the domestic Baijiu industry, which mainly produces and sells Moutai, one of the three famous liquors in the world. At the same time, it also produces and sells drinks, food and packaging materials, develops anti-counterfeiting technology, and develops information industry related products. Maotai liquor has a long history, is a typical representative of Maotai flavor Baijiu, and enjoys the reputation of "national liquor". Maotai liquor has been listed five times in the national wine evaluation event, and is a truly renowned liquor brand in China. At present, the annual production capacity of the company`s Maotai liquor has exceeded 10000 tons. The 43 °, 38 °, and 33 ° Maotai liquor have expanded the development space of the Maotai family`s low alcohol liquor. Maotai Prince liquor and Maotai Welcome liquor meet the needs of middle and low end consumers. The 15, 30, 50, and 80 year old Maotai liquor fills the gap in China`s premium liquor, vintage liquor, and aged cellar. The company`s products have formed more than 70 specification varieties in three series: low alcohol, high, medium, and low end, and premium, Fully layout the market.The brand difference of Baijiu itself is far greater than the taste difference. The brand determines the value. Consumption scenarios such as business banquets and gifts are less sensitive to the price. Therefore, the demand for Maotai liquor at the super high-end price segment has strong resilience. As the cost of Baijiu is mainly grain and packaging materials dominated by sorghum, the sales rate of leading brands is low, and the overall profitability is high (net profit rate exceeds 50%, ROE 30%); At the same time, the quota system and prepayment system have brought stable cash flow to the company.Since 1998, supported by strong brand strength, the company has further refined its channel management, focusing on flattening, direct sales, and reaching consumers. Since 2018, Maotai has increased its efforts to expand its direct sales channels, promoting continuous improvement in channel control and becoming one of the important contributions to Maotai`s performance growth. In March 2022, the launch of iMaotai`s self operated platform effectively increased the ton price through sales at guided prices. In addition, iMaotai also has functions such as omnichannel traffic entry, price stabilizer, and promotion. In recent years, continuously increasing the proportion of direct sales has become an important means for companies to recover channel profits and achieve performance growth without raising factory prices.According to the first quarter report of 2023, the company achieved a revenue of 38.76 billion yuan (yoy+20.0%) in the first quarter; Realized a net profit attributable to the parent company of 20.79 billion yuan (yoy+20.6%), exceeding market expectations. The company`s gross profit margin is 92.6% (yoy+0.2pct). The sales expense rate is 2.0% (yoy+0.3pct). The management expense rate is 5.2% (yoy 1.4 pct), and the revenue growth expense rate is diluted. The proportion of business taxes and surcharges to revenue is 14.1% (yoy+0.7pct). Overall, the net profit margin on sales of the company in Q1 was 55.5% (yoy 0.1pct), indicating a stable profitability level. The company`s 23 year revenue guidance target is a year-on-year growth of about 15%, which is highly likely to be successfully achieved. Looking forward to the future, Moutai, as the leader of Chinese Baijiu, is expected to fully benefit from the recovery of consumption in the year of consumption boosting; In the medium to long term, with the gradual expansion of production capacity and the upgrading of the series of liquor structure, the dividends of channel optimization continue to be released, and the driving force for development is sufficient. Shareholder buybacks also demonstrate the confidence of the management team.

Strategy:

Buy-in Price: RMB1706, Target Price: RMB1998, Cut Loss Price: RMB1555

|

|

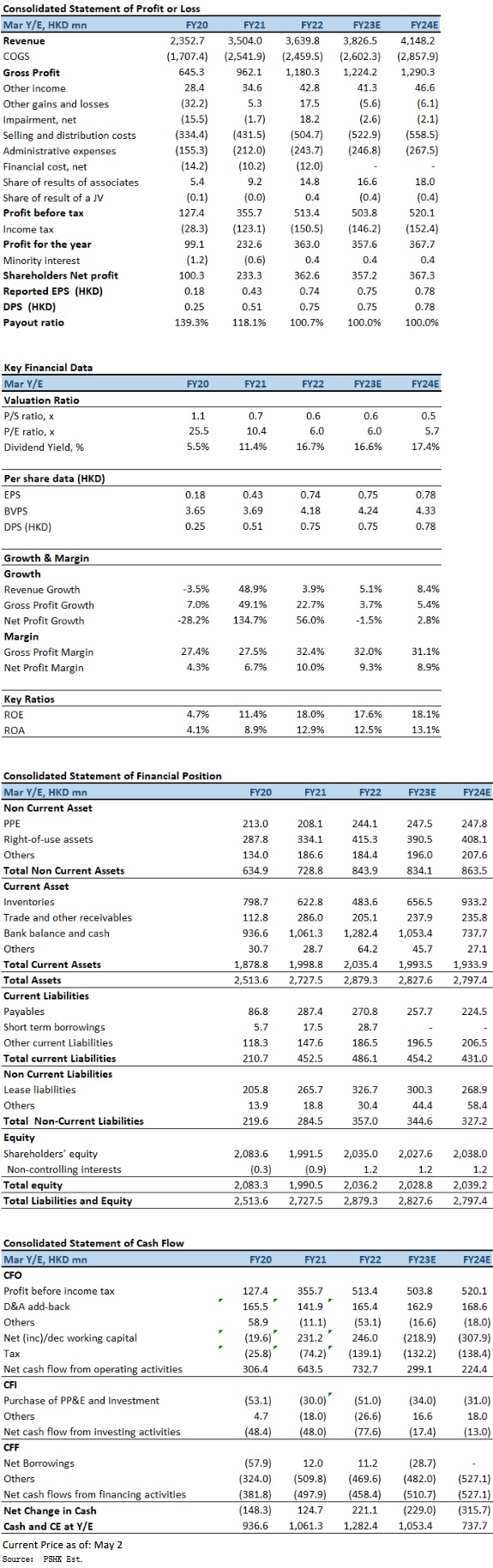

Oriental Watch Holdings Limited (398.HK) - HK operation outperformed the market, Conservative spending on high-end luxury goods become a concern

Oriental Watch Holdings Limited (Oriental Watch) that founded in 1961, has developed an extensive retail shop network in the Greater China area, and has become one of the largest watch retailers. Company carries around a hundred prestigious brands, in particular, famous Swiss brands such as Rolex, Tudor, Piaget, Vacheron Constantin, IWC, Jaeger-LeCoultre, Girard Perregaux, Longines, Omega, etc. Company operates a total of 12 shops in HK SAR and Macau SAR, including Oriental Watch Company, La Suisse Watch Company, Rolex and Tudor Boutique and Breitling Boutique. In 2004, company expanded its watch retail business to Mainland China. Since then, company has opened a number of outlets and boutiques covering various cities in Mainland, China. Subsequently, company has further expanded its businesses to Taiwan region. As at 30 September 2022, company operates 44 retail points (including associate retail stores) in the Greater China region, and 1 online store in each of the Mainland China and HK respectively. HK operation outperformed the market with revenue increased by 6.1% In 1HFY2023 (for the six months ended 30 September 2022), company's revenue decreased by 10.0% yoy to HK$1,674 million, which was mainly attributable to the decrease in revenue in the Mainland China market as a result of business interruptions due to such lockdown policy and restrictions. In line with the decrease in revenue, gross profit decreased by 6.9% to HK$537 million, with gross profit margin increased by 1.1 percentage points to 32.1%, and profit attributable to owners of the company decreased by 9.6% to HK$151 million. Basic EPS were 31.03 HK cents, down 9.2% yoy. Interim dividend of 7.8 HK cents per share (1HFY2022: 8.6 HK cents per share) and a special dividend of 23.5 HK cents per share (1HFY2022: 25.8 HK cents per share). During the Period, the company's aggregated expenses related to leases increased slightlyby 5.3% to HK$80 million, accounting for 23.1% of the overall operating expenses (1HFY2022: 22.2%). The increase was mainly due to the lease renewal of retail stores which command a relatively higher rental rate. In Hong Kong, the COVID-19 pandemic situation has been under control since the first quarter of 2022. Yet, clouded by market uncertainty, the market sentiment remained cautious with the value of total retail sales decreased by 1.3% yoy during the first nine months of the year. However, sales of jewelry, watches and clocks, and valuable gifts recorded a slight increase of 0.2% during the same period. Despite the uncertain retail market sentiment, Hong Kong operation still outperformed the market with revenue increased by 6.1% to HK$504 million for the period, accounting for 30.1% of the overall revenue, segment profit increased by 81.8% to HK$42.75 million. According to the National Bureau of Statistics, the PRC's gross domestic product (GDP) has recorded a 0.4% yoy growth and 3.9% yoy growth in the second and third quarter respectively, which grew at a softer pace compared with the same period of last year. The slowdown of economic growth was attributable to the widespread lockdown as well as the weakening market sentiment. Sales of gold, silver and jewelry also recorded a decrease of 0.8% yoy from April to September 2022. According to the Federation of the Swiss Watch Industry FH, the Swiss watch exports to the PRC during the Period decreased 13.7% yoy to CHF1,267.3 million, showcasing the country's conservative sentiment on purchasing luxury watches. Due to the economic condition as well as the temporary business suspension mentioned above, revenue from Mainland China operation decreased by 15.4% to HK$1,101 million, accounting for 65.8% of the overall revenue, segment profit decreased by 23% to HK$189.86 million. Investment ThesisLooking ahead, although China and Hong Kong have entered the road to normal after the epidemic, with the uncertainty from the increase in interest rate, and the management also expects consumers to become more conservative in consumption, especially on purchasing of high-end luxury goods. Hence, the business will be under some pressure over the upcoming periods. We expect FY2023-FY2024 EPS to be 74.62 HK cents and 78.10 HK cents respectively, with PT of HKD5.14, implies a FY2023E P/B of 1.21x (~1-yrs historical average plus 1 SD). Our investment rating is “Accumulate”. Risk factors1) Economic recovery momentum is slowing down; 2) Operating costs are higher than expected; 3) Luxury goods consumption is lower than expected. �Financial

Click Here for PDF format...

| Recommendation on 11-5-2023 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 4.490 | | Suggested purchase price | N/A | | Target Price | $ 5.140 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|