|

JD LOGISTICS(2618)

Analysis:

For three months ended March 31, 2023, JD Logistics (2618) reorded revenue of RMB36.7 billion, representing a susbstantial increase of 34.3% as compared to the same period last year. The increase in its total revenue was driven by the increase in revenue from integrated supply chain customers and the increase in revenue from other customers. Revenue from integrated supply chain customers increased by 3.1% to RMB18.5 billion. The increase in revenue from integrated supply chain customers was primarily driven by the increase in average revenue per customer (ARPC), which increased to RMB132,894 for the three months ended March 31, 2023, from RMB110,762 for the same period of 2022, representing a year-over-year increase of 20.0%. Its ARPC improvement reflected customer endorsement for its integrated supply chain solutions and logistics services along with deepening collaborations and growing customer stickiness. Revenue from other customers increased by 93.4% to RMB18.3 billion, primarily due to the increases in business volume of its express delivery and freight delivery services, as well as the consolidation of Deppon Group. As of March 31, 2023, its warehouse network covered nearly all counties and districts in China, consisting of over 1,500 self-operated warehouses and over 2,000 third-party warehouse-owner operated cloud warehouses under its Open Warehouse Platform. Its warehouse network has an aggregate GFA of more than 31 million square meters, including warehouse space managed through the Open Warehouse Platform. With different functions and capabilities, these warehouses have further elevated its supply chain services abroad. In February 2023, its Los Angeles No.3 Warehouse officially commenced operation, providing integrated supply chain logistics solutions to customers with varying needs. As of March 31, 2023, the gross floor area (GFA) of its self-operated warehouses in the United Sates exceeded 1.3 million square feet. With different functions and capabilities, these warehouses have further elevated our supply chain services abroad. (I do not hold the above stock)

Strategy:

Buy-in Price: $13.00, Target Price: $14.20, Cut Loss Price: $12.40

|

CHINA PET FOODS(002891.SZ)

Analysis:

The company started with overseas pet food OEM and has established 20 modern high-end production bases in China, the United States, New Zealand, and other places. It has formed a complete industrial chain of pet snacks, dry food, wet food, toys, and other products, forming a brand matrix with "Wanpy Naughty", "Zeal True", and "Toptrees Leading" as the core, including more than 100 independent brands. At present, independent brands have become an important growth curve. In Q1 2023, the company achieved a revenue of 706 million yuan, YoY-11.00%, and a net profit attributable to the parent company of 16 million yuan, YoY-33.06%, mainly due to factors such as overseas customer destocking. With the end of overseas order destocking, overseas business will gradually return to normal. In March 2023, based on the supply and demand gap, the company plans to build a second factory in the United States, and the expansion of production capacity is expected to bring about rapid growth in future performance.

Strategy:

Buy-in Price: RMB20.80, Target Price: RMB24.70, Cut Loss Price: RMB18.70

|

|

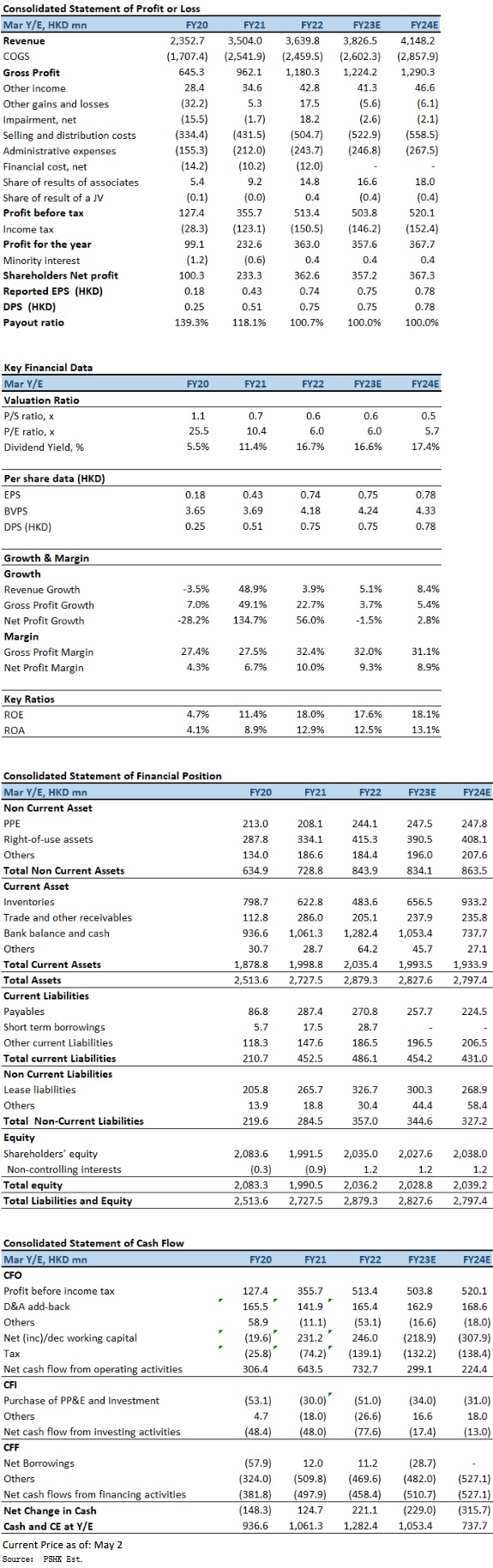

Oriental Watch Holdings Limited (398.HK) - HK operation outperformed the market, Conservative spending on high-end luxury goods become a concern

Oriental Watch Holdings Limited (Oriental Watch) that founded in 1961, has developed an extensive retail shop network in the Greater China area, and has become one of the largest watch retailers. Company carries around a hundred prestigious brands, in particular, famous Swiss brands such as Rolex, Tudor, Piaget, Vacheron Constantin, IWC, Jaeger-LeCoultre, Girard Perregaux, Longines, Omega, etc. Company operates a total of 12 shops in HK SAR and Macau SAR, including Oriental Watch Company, La Suisse Watch Company, Rolex and Tudor Boutique and Breitling Boutique. In 2004, company expanded its watch retail business to Mainland China. Since then, company has opened a number of outlets and boutiques covering various cities in Mainland, China. Subsequently, company has further expanded its businesses to Taiwan region. As at 30 September 2022, company operates 44 retail points (including associate retail stores) in the Greater China region, and 1 online store in each of the Mainland China and HK respectively. HK operation outperformed the market with revenue increased by 6.1% In 1HFY2023 (for the six months ended 30 September 2022), company's revenue decreased by 10.0% yoy to HK$1,674 million, which was mainly attributable to the decrease in revenue in the Mainland China market as a result of business interruptions due to such lockdown policy and restrictions. In line with the decrease in revenue, gross profit decreased by 6.9% to HK$537 million, with gross profit margin increased by 1.1 percentage points to 32.1%, and profit attributable to owners of the company decreased by 9.6% to HK$151 million. Basic EPS were 31.03 HK cents, down 9.2% yoy. Interim dividend of 7.8 HK cents per share (1HFY2022: 8.6 HK cents per share) and a special dividend of 23.5 HK cents per share (1HFY2022: 25.8 HK cents per share). During the Period, the company's aggregated expenses related to leases increased slightlyby 5.3% to HK$80 million, accounting for 23.1% of the overall operating expenses (1HFY2022: 22.2%). The increase was mainly due to the lease renewal of retail stores which command a relatively higher rental rate. In Hong Kong, the COVID-19 pandemic situation has been under control since the first quarter of 2022. Yet, clouded by market uncertainty, the market sentiment remained cautious with the value of total retail sales decreased by 1.3% yoy during the first nine months of the year. However, sales of jewelry, watches and clocks, and valuable gifts recorded a slight increase of 0.2% during the same period. Despite the uncertain retail market sentiment, Hong Kong operation still outperformed the market with revenue increased by 6.1% to HK$504 million for the period, accounting for 30.1% of the overall revenue, segment profit increased by 81.8% to HK$42.75 million. According to the National Bureau of Statistics, the PRC's gross domestic product (GDP) has recorded a 0.4% yoy growth and 3.9% yoy growth in the second and third quarter respectively, which grew at a softer pace compared with the same period of last year. The slowdown of economic growth was attributable to the widespread lockdown as well as the weakening market sentiment. Sales of gold, silver and jewelry also recorded a decrease of 0.8% yoy from April to September 2022. According to the Federation of the Swiss Watch Industry FH, the Swiss watch exports to the PRC during the Period decreased 13.7% yoy to CHF1,267.3 million, showcasing the country's conservative sentiment on purchasing luxury watches. Due to the economic condition as well as the temporary business suspension mentioned above, revenue from Mainland China operation decreased by 15.4% to HK$1,101 million, accounting for 65.8% of the overall revenue, segment profit decreased by 23% to HK$189.86 million. Investment ThesisLooking ahead, although China and Hong Kong have entered the road to normal after the epidemic, with the uncertainty from the increase in interest rate, and the management also expects consumers to become more conservative in consumption, especially on purchasing of high-end luxury goods. Hence, the business will be under some pressure over the upcoming periods. We expect FY2023-FY2024 EPS to be 74.62 HK cents and 78.10 HK cents respectively, with PT of HKD5.14, implies a FY2023E P/B of 1.21x (~1-yrs historical average plus 1 SD). Our investment rating is “Accumulate”. Risk factors1) Economic recovery momentum is slowing down; 2) Operating costs are higher than expected; 3) Luxury goods consumption is lower than expected. �Financial

Click Here for PDF format...

| Recommendation on 15-5-2023 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 4.490 | | Suggested purchase price | N/A | | Target Price | $ 5.140 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|