Overview

CMGE (302.HK) is a global IP game ecological company. As of December 31, 2022, the Group has a huge IP reserve, including 64 authorized Ips and 68 self-owned Ips, totaling 132 IPs. According to data from Analysys, apart from Tencent Games, the Group is the Chinese game publisher with the largest number of IP reserves, and the Chinese game publisher with the largest number of mobile IP games launched in the past two years. The Group's revenue sources mainly come from three parts, namely game distribution, game development and intellectual property (IP) licensing.

A review of 2022 Results

For the year ended 31 December 2022, the company's revenue amounted to 2.71 billion (RMB, the same below), decreasing 31.4% YoY. The cost of sales amounted to 1.6 billion, decreasing 35.5% YoY. Gross profit amounted to 1.11 billion, decreasing 24.6% YoY. Gross profit margin was 41%, a slight increase of 3.7 percentage points YoY. The loss during the period amounted to 210 million, turning from profit to loss YoY. The adjusted net loss amounted to 200 million, turning from profit to loss YoY.

Revenue by Business Type

The revenue of the game publishing business amounted to 2.11 billion, decreasing 25% YoY, accounting for 77.9% of the total revenue. The decline in revenue was mainly due to the postponement of obtaining licenses as scheduled for various games planned to be published in the first half of 2022 by the Group such as Sword and Fairy: Wen Qing, Rakshasa Street: Chosen One and Cultivation Fantasy led to the delay in the launch of these games. However, Rakshasa Street: Chosen One, an online mobile game published by the Group, was achieved a huge success in Mainland China; the Group launched The New Legend of The Condor Heroes: Iron Blood and Loyal Heart success. Publishing new games provided new publishing revenue to the Group.

The revenue of the game development business amounted to 452.6 million, decreasing 50.0% YoY, accounting for 16.7% of the total revenue. The decline in revenue primarily as a result of the decrease in the average monthly gross billing for The World of Legend – Thunder Empire and Legend of Dragon City, both developed by Wenmai Hudong, a wholly owned subsidiary of the Group, and slow-down in the growth of revenue from self-developed card and board games of the Group; and the postponement of obtaining licenses as scheduled for various games planned to be published in the first half of 2022 by the Group, such as self-developed game World of Castellan, led to the delay in the launch of these games. However, The King of Fighters: All Stars, a 3D mobile game self-developed and published by the Group and with multiple series officially licensed from SNK, has been launched in Mainland China in November 2022, it brings new game development revenue to the Group.

The revenue of the IP licensing business amounted to 147.1 million, decreasing 36.6% YoY, accounting for 5.4% of the total revenue. The decline in IP licensing revenue primarily as a result of the decrease in the Group's revenue generated from IP licensing of the Legend of Sword and Fairy.

Business features

The company's business mainly revolves around the IP of a large number of well-known cultural products and works of art that it owns, such as from popular animations, novels and movies. The company's well-known film and television IPs include licenses from Disney, Warner Bros., Universal Studios` Star Wars, Disney All-Stars, DC Comics, and Minions. Comics IP includes the famous Japanese comics “One Piece”, “Naruto”, “Dragon Ball”, etc. The film and game IP includes the famous Chinese fairy tale series “Xuan Yuan Sword” and “Sword and Fairy”.

In terms of agency game sharing, according to the company's prospectus, the company's agency game revenue is mainly shared with game developers, distribution channels and IP copyright owners (if applicable). Among them, game developers will earn around 14% to 25% of the total revenue, distribution channels will earn around 5% to 9%, and the company itself can earn around 16% to 51%.

Gaming business

The company's game publishing revenue from 2018 to 2022 accounted for 88%, 84%, 78%, 71% and 77.9% of the total revenue respectively. The data reflects that the company is gradually releasing the value of its IP and the development of its self-developed game business. Income gradually no longer depends on a single business. However, as the company was greatly affected by the suspension of the game license in the first half of 2022, the new game failed to obtain the license and go online in time to replace the existing self-developed and publishing games with declining popularity, and there was no large-scale IP authorization. Income can only rely on existing publishing games, and the overall income has dropped significantly.

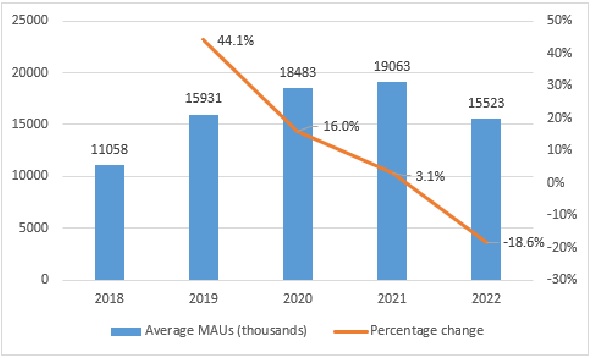

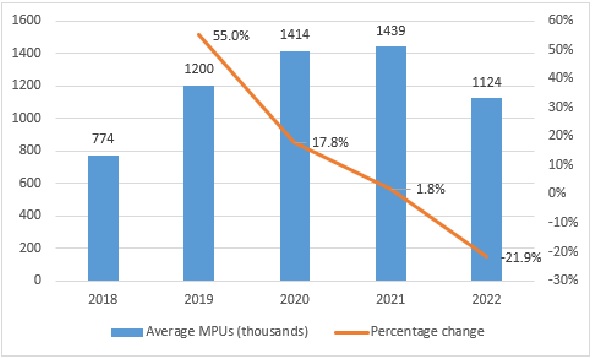

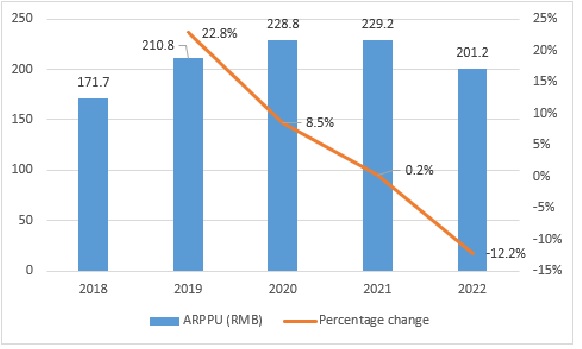

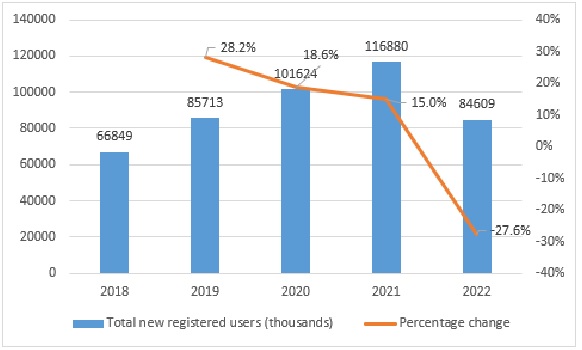

The seriousness of the suspension of game licenses is also reflected in the user data. In 2022, the average MAUs, average MPUs, ARPPU, and total number of new registered users all change from the pervious upward trend and fell by 18.6%, 21.9%, 12.2% and 27.6% YoY respectively. The following figure shows the trend of user data in recent years:

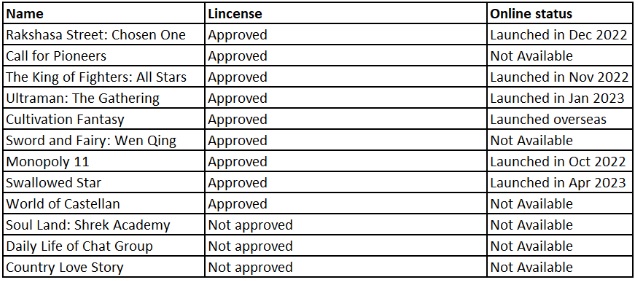

However, as the previously hoarded games that were previously unapproved due to licenses have been approved one after another, and some games have performed well, we expect the company's various businesses will gradually regain growth momentum in 2023, showing a more obvious YoY growth. Among them, the company expects that he following table shows the current situation of the company's new games:

Popular games

Rakshasa Street: Chosen One is a 3D role-playing action (ARPG) game launched in December 2022 in the style of “China Fashion” (emerging trends that include traditional Chinese style). The theme of the game comes from the popular animation IP Rakshasa Street in the mainland. The game has more than 5 million users who pre-ordered and downloaded the game in mainland China. On the first day of its launch, the number of downloads across all channels exceeded 2 million, and the turnover exceeded 100 million in the first week. It ranked No.1 on the China App Store Free List and No.4 on the Best-Selling List. According to the data survey agency Sensor Tower (the data does not include third-party Android platforms in China or other places, the same below), the game has US $500,000 in revenue and 30,000 downloads in April 2023. The overall performance of the game is good but compared with the revenue of 3 million USD and the number of downloads of 200,000 in January, the data declines faster, and the game team needs to work hard to maintain the popularity of the game.

One Piece: The Voyage is a 3D action game jointly developed by CMGE and Nuverse Game under ByteDance. It launched in May 2021. The theme of the game comes from the famous Japanese animation IP One Piece authorized by CMGE. According to Sensor Tower, the game has USD 3 million in revenue and 100,000 downloads in April 2023. The game has performed well since its launch, and it still maintains a good turnover and popularity.

Ultraman: The Gathering is a mobile game developed by Hainan Hemera, which is invested by CMGE, and authorized by Japan Tsuburaya Co., Ltd. To adapt the original authorized mobile game of the Ultraman series IP. It launched on January 13, 2023. The game received more than one million user registrations during the beta period, and the response was good. According to Sensor Tower, the game has USD 90,000 in revenue and 20,000 downloads in April 2023. The overall performance of the game is average, and the data declines rapidly.

The King of Fighter: All Stars is a large-scale IP adapted mobile phone boutique game independently developed by CMGE. It is a 3D action card game with realistic painting style. The game covers all well-known IP characters of the Japanese video game company SNK's game series, such as the King of Fighters, etc., and links a few top Japanese comic characters. After three years of preparing, it launched in November 2022 and turnover broke 50 million in the first week. However, the game has USD 90,000 in revenue and lower than 5,000 downloads. The data shows that the game is not outstanding in China, and it may miss the company's expectations. However, because the IP contained in this game is quite famous in the world (especially in Japan, Hong Kong, and Taiwan), and the company also intends to release this game in many overseas regions, the growth potential of the game still exists. Investors need to pay attention to the future overseas development of games. In fact, CMGE announced on February 10 that the game was named as SNK: All – Star Fight and officially launched in Hong, Macau, Taiwan, Singapore, and Malaysia. The number of pre-registrations has exceeded one million, and it won the first place in the downloads of game apps in the five local application markets on the day of its launch. According to Sensor Tower, overseas version of the game has USD 200,000 and 6,000 downloads in April 2023. The data shows that the performance of the game in overseas is better than that in the mainland, and we believe investors can look forward to the game's launch in Japan.

Swallowed Star, a mobile game researched and developed by the Group's investee company Guangzhou Maiji Information Technology Co. Ltd. With China Literature Limited's first heavyweight IP Swallowed Star as the basis. It is a 3D turn-based card game with the theme of doomsday and science fiction. It publishes in April 2023. According to Sensor Tower, the game has USD 1 million in revenue and 400,000 downloads in April 2023.

Overseas game market

As of June 30, 2022, the Group has launched 5 games in multiple overseas regions. The 2022 annual revenue from overseas regions amounted to 361.2 million, accounting for 13.3% of the Group's total revenue. The company plans to launch several new games in Hong Kong, Macao and Taiwan in 2023, including Rakshasa Street: Chosen One, 3D idle card mobile game Sword and Fairy: Wen Qing, Three Kingdoms: The Legend of Cao Cao, Don`t Say Goodnight to Fairy Tales, Daily Life of Chat Group and Code: FA. Besides, the game Soul Land: God of Battle Arise will also be launched in Korea, Europe and the United States in the first half of 2023. The game Dynasty Warriors: Hegemony will be launched in Japan, Europe, and the United States in 2023. In an exclusive interview, the chairman of the Group claimed that Overseas revenue in 2023 is expected to equal domestic revenue (overseas and domestic revenue each account for 50% of total revenue). We believe that although the company deplots and launches several games in the overseas game market this year, which will drive overseas game revenue, considering that the IP of these is not well-known in overseas regions and the performance of the game after launch is doubtful, it is difficult for the chairman to achieve this goal.

In the aspect of game development, the company will consider whether the game theme can be launched in multiple places and localized in the early stage of product development, and continues to acquire global IP, which reflects that the Group attaches great importance to overseas business and hopes to develop overseas markets to reduce policy risk in the mainland. The Group currently mainly develops Southeast Asia (Vietnam, Thailand, Philippines) and Hong Kong, Macao, and Taiwan markets, and plans to develop markets such as Japan, South Korea, and the United States in the future. However, at presents, most of the company's game styles are biased towards Chinese style, and it is difficult to enter the European and American markets. The group needs to develop some high-quality games that meet the tastes of the European and American markets, such as art style and gameplay, which will increase the company's research and development costs.

IP development

According to Gamma Data's 2021 China Self-developed Game IP Research Report, the group's well-known IP Xuan Yuan Sword” and “Sword and Fairy” are among China's most influential TOP50 self-developed game IP products. At present, the group is deeply developing the cooperation of the entire industry chain of “Sword and Fairy” IP, covering games, film and television, animation, content literature, music, derivatives, and live entertainment, etc., and hopes to join hands with top partners in related fields to jointly create the “Sword and Fairy” IP universe. The Group currently has three projects worthy of investors` attention, including “Sword and Fairy: Wen Qin”, “Sword and Fairy: Yuanqi” and “Sword and Fairy: world”. “Sword and Fairy: Wen Qin” is a story-adventure card mobile game, and the license has been approved.

As for “Sword and Fairy: Yuanqi” is a massively multiplayer online role-playing (MMORPG) mobile game that the company cooperates with Alibaba's Lingxi Interactive Entertainment. It has entered the final test but has not yet obtained the license. Given that Lingxi Interactive Entertainment is good at producing high-quality games, such as its games “Romance of the Three Kingdoms” and “Orient Arcadia” have performed very well. According to the data of Sensor Tower, the former has been ranked among the top ten popular mobile games in the world for a long time after its launch, and the latter ranked first in the overseas revenue growth list of Chinese mobile games in October 2022 after its overseas launch. Considering the massively multiplayer online role-playing game's strong ability to attract money and the good reputation of the research and development company, we expect that the launch of this game may become a catalyst for the company's stock price.

“Sword and Fairy: world” is China's first cross-platform Chinese culture Metaverse game with open world elements, and also the first China's Chinese culture Metaverse entertainment and social platform that provides in-depth experience of virtual reality and allows players to use virtual reality equipment to truly incarnate virtual characters. In addition, the company has become a partner of Baidu's ERNIE Bot, and will apply the technology of ERNIE Bot in the game to realize the function of non-player character (NPC) interaction and more convenient User Generated Content (UGC) creation to enhance player gaming experience. At present, the company plans to launch this game in the first half of 2023. We expect that this game will attract many players to try because of its uniqueness and freshness. However, since the concept of “Sword and Fairy” combined with metaverse is too unique and innovative, investors need to pay attention to factors such as player feedback and game quality after the game is launched to evaluate the game's monetization ability and subsequent performance.

Risk factors

Games may not be launched as expected, affecting revenue performance

In addition to the fact that the company's game licenses were not approved as scheduled, which affected the launch of new games, the company also delayed the delayed the launch of game due to other factors in the past, such as game quality not meeting expectations. For example, “The King of Fighters: All Stars” and “Call for Pioneers”, etc. “The King of Fighters: All Stars” has already obtained the license in November 2019, and in the 2020 annual results, the company stated that the game has undergone multiple external open tests and has opened game reservations. It is expected to be officially launched in the first half of 2021. However, in fact, the game's launch time was postponed until November 2022 before it was officially launched. As for “Call for Pioneers” the license was approved in February 2021, and it was stated in the 2022 interim report that it planned to launch in December 2022, but it also did not launch as scheduled.

Valuation and recommendation

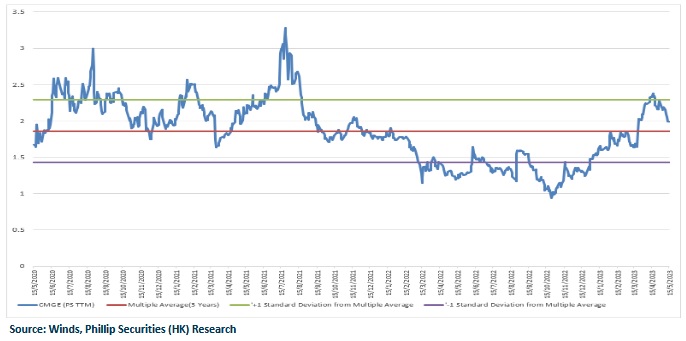

The uniqueness of CMGE is that the company has many well-known IPs, which can attract players who love the IP to try the game because of the IP. At the same time, other game companies will cooperate with them to develop games because of the IPs owned by CMGE and complement each other. With the re-approval of game licenses in the mainland, the negative factors that mainly affect CMGE have been eliminated. In the first half of 2022, the key games hoarded due to the unapproved licenses are being launched one after another, which is expected to greatly improve the company's revenue in 2023. Also, “Sword and Fairy: Yuanqi” is worth looking forward to by investors. We expect CMGE's net sales amount to RMB 3.96 billion and 50.7 billion in FY2023-2024 respectively, the CAGR of 2022 – 2024 is 23.2%. Corresponding P/S ratio are 1.6/1.2x. While the company's average P/S in the past three years was around 1.86, we give CMGE 1.86 P/S in FY 2023 and a target price of $3.00 HKD. (Calculated at the exchange rate of RMB to HKD 1.13), with a “buy” rating. (Current price as of May 15)

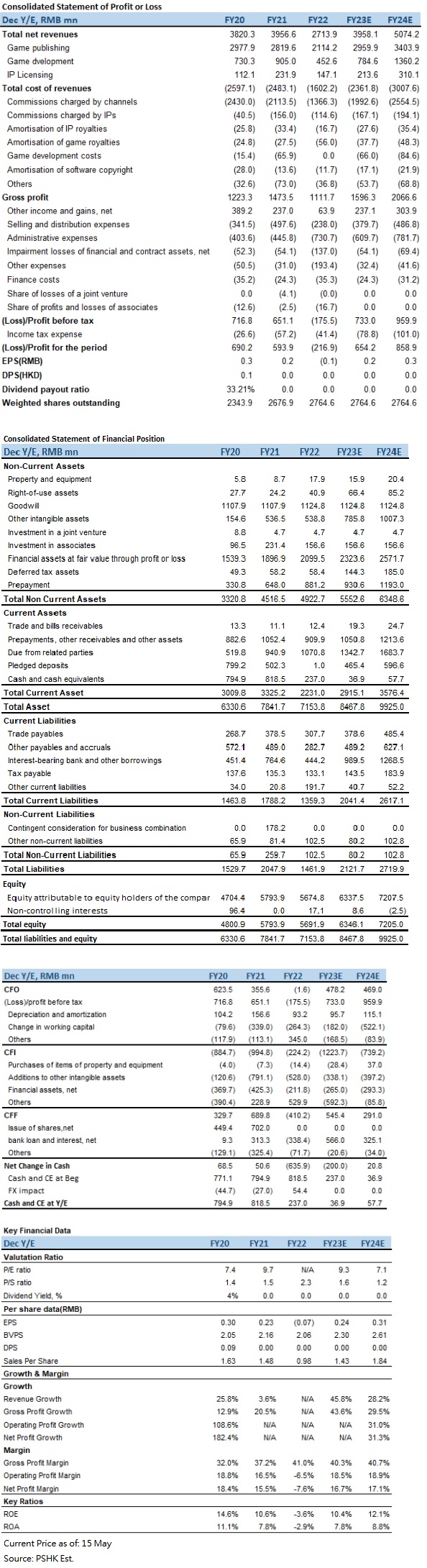

�Financial

Click Here for PDF format...