Overview

Bloomage Biotechnology (688363.SH) is the leader in the global hyaluronic acid industry chain. It has gradually become the world's leading comprehensive supplier of bioactive substances. The company is a hyaluronic acid whole industry chain platform enterprise integrating research and development, production and sales. The technology of microbial fermentation to produce hyaluronic acid is in leading position in the world. It has bioactive materials ranging from raw materials to medical terminal products, functional skin care products, and functional foods. Hyaluronic acid is widely used in medical, cosmetic and functional food fields. As the main component of the intercellular and extracellular matrix, hyaluronic acid widely exists in the joint cavity, skin and other tissues of the human body, and is an indispensable and important substance in human body.

A review of 2022 Results

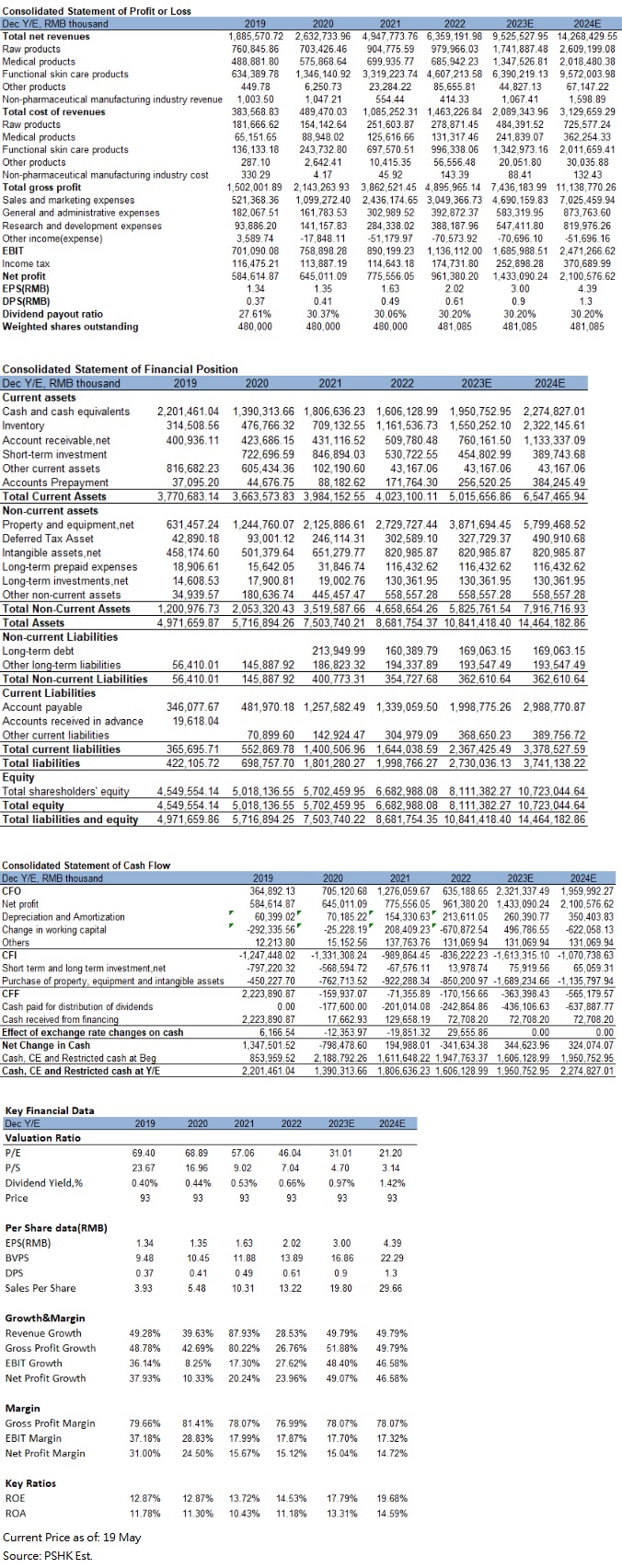

The company's operating income in 2022 was 6.359 billion (RMB, the same below), an increase of 28.53% YoY; The net profit attributable to the owners of the parent company was 970 million, an increase of 24.11% YoY; The net profit of recurring profit and loss was 850 million, an increase of 28.46%YoY. At the end of the reporting period, the total assets were 8.681 billion, an increase of 15.7% YoY; The owner's equity attributable to the parent company was 6.633 billion, an increase of 16.40% YoY. The main factor affecting the operating performance is that the company continues to steadily promote the "four-wheel drive" business layout, and the overall operating income has achieved relatively high growth. The raw material business has grown steadily, the medical terminal business has remained basically flat, and the functional skin care business has maintained rapid growth. The food business has achieved rapid growth in the early stage of commercialization. The company improves operational efficiency through refined management, and the growth rate of total expenses during the period is lower than the growth rate of operating income.

Revenue by Business Type

In 2022, the company's raw material business achieved revenue of 980 million, an increase of 8.31% YoY, accounting for 15.41% of the company's main business revenue. The overall gross profit margin of the raw material business was 71.54%. Among them, the sales revenue of pharmaceutical grade hyaluronic acid was 337 million, a year-on-year increase of 33.73%. In 2022, the company's export raw material sales revenue was 426 million, accounting for 43.45% of the company's raw material business revenue. In 2022, the revenue growth rate of the raw material business slowed down compared with the previous year, mainly due to the impact of the supply and demand relationship in the hyaluronic acid raw material market. The upstream supply end has slightly contracted due to the temporary suspension of production, and the downstream demand end has suffered a decline in demand due to market shocks, resulting in company's domestic sales of hyaluronic acid impacted in the short term. The company continues to promote the internationalization strategy, strengthens the overseas layout of the raw material business, and will optimize existing products through synthetic biology technology and continue to develop new potential bioactive substances to enrich the product matrix. In the future, the pharmaceutical-grade hyaluronic acid raw material business with higher gross profit margin will continue to maintain a relatively high growth rate, and the food-grade hyaluronic acid raw material business and other bioactive substances will maintain stable growth.

In 2022, the company's medical terminal business achieved revenue of 686 million, a year-on-year decrease of 2.00%, accounting for 10.79% of the company's main business revenue, with a gross profit margin of 80.86%. Among them, skin medical products achieved revenue of 466 million, a year-on-year decrease of 7.56%. The revenue of liquid products was 152 million yuan, a year-on-year increase of 22.98%; The total revenue of other products was 68 million yuan, a year-on-year decrease of 5.79%.

In 2022, the company's functional skin care products achieved revenue of 4.607 billion, a year-on-year increase of 38.80%, accounting for 72.45% of the company's main business revenue, with a gross profit margin of 78.37%. Among them, the four brands of Runbaiyan increased by 12.64% year-on-year, Quady increased by 39.73% year-on-year, Mibel increased by 44.06% year-on-year, and BM Muscle Live increased by 106.40% year-on-year. Following the Runbaiyan brand, Quady has become the second brand with a revenue of more than 1 billion. At the same time, BM Muscle Life achieved a revenue of 898 million in 2022. It is expected to become the third brand whose revenue has reached the threshold of 1 billion yuan. From the perspective of revenue structure, the company's products with over 100 million have increased compared with the same period of the previous year, and the business foundation is more stable; The proportion of sales revenue of the company's TOP10 products has increased, and the concentration of core products has further increased. The company started with two to B businesses of raw materials and medical terminals. In recent years, the proportion of its to C business has been increasing all the way. The revenue of functional skin care products has increased from 33.6% to 72.5% in the past four years. It shows the company's multi-brand operation ability, and it will continue to move towards national brands in the future.

In 2022, the company's functional food business achieved revenue of 75 million, a year-on-year increase of 358.19%. The company's functional food business has achieved rapid growth, but its volume still does not have a large scale. At present, the functional food market is still in the early stage of consumer education. The company must not only develop the market, but also invest steadily to control the overall cost. As of 2022, a total of 101 functional food research and development projects have been carried out, focusing on oral beauty food, oral sleep aid food and related functional foods such as hyaluronic acid, GABA aminobutyric acid, bird's nest acid, tremella, etc.

In recent years, the company's gross profit margin has maintained a high level of over 75%, but the net profit margin has declined. The reason is that the functional skin care products business has developed rapidly, and the corresponding sales expenses have increased rapidly, making the sales expense ratio continue to rise and the growth rate is relatively low. In 2022, the company's sales expense ratio/management expense ratio/R&D expense ratio was 47.95%/6.18%/6.10%, respectively. In terms of sales expense ratio, compared with other companies in the same industry, Bloomage Bio's sales expense ratio was generally higher. The online promotion service fee was increasing year by year, which is the primary expenditure of sales expenses; On the other hand, R&D expenses were increasing rapidly. In 2022, the R&D expense ratio reached 6.10%, and the R&D investment was 388 million, a year-on-year increase of 36.52%. It is expected that the R&D expense ratio will rise steadily in the next few years and remain at around 6%. As of 2022, the company has 827 R&D personnel, an increase of 256 compared with the previous period. In the future, with the R & D and innovation of raw materials, technical processes, and application products, the profit level is expected to increase. The company is also one of the enterprises with the largest number of hyaluronic acid patents in China. The company has applied for 719 patents, of which 337 have been authorized. The company's international qualification certification advantages and patented technology advantages ensure that the company maintains its leading position in the industry in domestic and foreign markets.

In 2022, the company's gross profit margin was 76.99%. Among the four major business segments, the medical terminal business (gross profit margin of 80.86%) had the highest gross profit margin in 2022, followed by the functional skin care business (gross profit margin of 78.37%), followed by raw materials (gross profit margin 71.54%). Since 2020, the gross profit margin of each business has been on the decline. If there are major changes in the company's business scale, product structure, customer resources, cost control, etc. in the future, or industry competition intensifies, resulting in a decline in the sales price of the company's products, an increase in costs, or a major change in customer demand, the company will face gross profit margin of the main business cannot maintain a high level or the risk of decline.

Business features

The sales volume of the global hyaluronic acid raw material market is growing rapidly. China is the largest consumer market. According to Frost & Sullivan, it is estimated that by 2026, the sales volume of the global hyaluronic acid raw material market will reach 1285.2 tons, and the CAGR from 2021 to 2026 will be 12.29%. -The CAGR in 2026 will be 12.83%, which is basically in line with the growth rate of the global market. In addition, the global market for hyaluronic acid raw materials is highly concentrated, and company's market share is firmly in the leading position. According to data from Frost & Sullivan, the sales volume of hyaluronic acid in China accounts for more than 80% of the total global sales volume. The top four sales volumes are all Chinese companies, and the total market share of the four companies is as high as 75%. Among them, Bloomage Biotech remained the world's number one with a market share of 44% in 2021.

In terms of industry segmentation, the global sales structure of hyaluronic acid raw materials is relatively stable, and the proportion of food-grade hyaluronic acid raw materials continues to expand. According to Frost & Sullivan, the pharmaceutical grade/cosmetic grade/food grade hyaluronic acid raw material market share (by sales volume) was about 4%/43%/53% in 2021. Pharmaceutical grade/cosmetic grade/food grade market share of hyaluronic acid raw materials (according to sales volume) will be 4%/33%/63% in 2026. The market share of food-grade raw materials will continue to expand, and the market share of pharmaceutical-grade raw materials will remain basically unchanged. The CAGR of the pharmaceutical grade/cosmetic grade/food grade hyaluronic acid raw material market was about 15.1%/9.9%/18.8% from 2017 to 2021. Affected by the epidemic in 2020, the sales growth rate of various raw materials declined. Food-grade raw materials are expected to increase significantly in the next few years. From 2022 to 2026, the CAGR will reach 15.6%, becoming the hyaluronic acid raw material category with the largest growth rate.

The research and development and maturity of hyaluronic acid production technology requires a large amount of capital, labor and time for the enterprise, and the investment cost is huge, the risk of research and development failure must be borne. Hyaluronic acid has strict regulatory access review, and the advantages of patent qualification certification are difficult to surpass. In particular, the domestic registration qualification application for medical products generally takes 3-5 years, and there is a risk of the application being rejected. The raw material production and manufacturing of hyaluronic acid has a high regulatory entry threshold, so the overall threshold of the upstream of the hyaluronic acid industry is relatively high, forming high industry barriers.

Valuation and recommendation

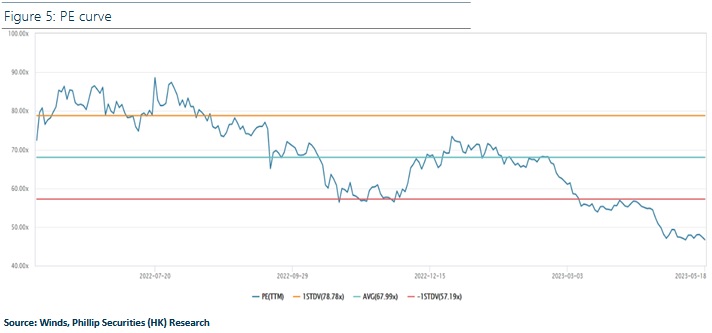

Bloomage Tianjin plant added 300 tons of hyaluronic acid production capacity, built the world's largest pilot transformation platform, and the pilot production line has been officially put into operation. The bidding for the main equipment of the aseptic grade HA production line of Dongying First Factory has been completed in 2022, and it is expected to start production in 2023, which will further occupy the highest-end market of HA. The Bloomage Life and Health Industrial Park project will complete the bidding for equipment and facilities, and some equipment has been installed on site. It is expected to start production in 2023, which will further increase the production capacity of hyaluronic acid terminal products. The realization of the company's new production capacity layout will provide basic support for the development of its own hyaluronic acid terminal business, thereby continuously boosting the company's future performance. We predict that the company's revenue will be 9.525 billion and 14.268 billion in 2023-2024, respectively, with a compound annual growth rate of 49.79%, and EPS will be 3/4.39 yuan, corresponding to a price-earnings ratio (P/E) of 31 / 21x. The company's average P/E in the past year was about 68. In 2022, Bloomage Bio's revenue increased by 28.53% to 6.359 billion, which was lower than the growth rate of 88% in 2021. Due to the decline in revenue growth and the Global and China Hyaluronic Acid (HA) Industry Market Research Report" released by Frost & Sullivan shows that the average price of hyaluronic acid raw materials has gradually dropped from 210 yuan/gram in 2017 to 124 yuan in 2021 /g, a drop of more than 40%. We give the company 38 times P/E in 2023, and a target price of 114 RMB, with a "buy" rating. (Current price as of May 19)

�Financial

Click Here for PDF format...