Company Profile

As one of the leading heavy truck manufacturers in China, Sinotruk specializes in the heavy trucks, light trucks, buses and related major powertrains and parts. With heavy trucks as the main products, the Company serves a wide range of customers in the infrastructure, construction, container service, logistics, mining, steel and chemical industries.

Investment Thesis

Despite a Trough in China's Heavy Truck Industry, the Company Outperforms the Industry Average in 2022

According to the data of cvworld.cn, China's heavy truck industry sold a total of 672 thousand units in 2022, down 720 thousand units or 52% yoy, of which the cumulative sales volume of new energy heavy trucks was 25.1 thousand units, up 140% yoy. In 2022, affected by multiple adverse factors such as the Covid-19 pandemic, economic slowdown, low investment and consumption, sluggish freight, lack of confidence, and demand overdraft, China's heavy truck industry has seen a yoy decline in the sales volume for 12 consecutive months.

Sinotruk sold 158 thousand heavy trucks in 2022, down 44% yoy, a decrease significantly less than the industry average of 52%. The Company occupied a share of 23.5% in China's heavy truck market, up 3.0 ppts over the same period last year, surpassing FAW Jiefang and ranking first. We think that the reasons for Sinotruk's increased market share despite headwinds are mainly as follows: 1) In the domestic market, the Company has made certain breakthroughs in the development of key segments and key customers. Dump trucks and mixer trucks continued to maintain their competitive edge. The market share of high-horsepower tractors, trucks and special vehicles has grown significantly. 2) With the help of Sinotruk International's network layout and strategic breakthroughs, the Company's export sales volume of heavy trucks reached a new high during the reporting period, increasing by 65% yoy to 89 thousand units, accounting for 56% of the Company's total sales volume of heavy trucks, and maintaining the first place in China for 18 consecutive years.

Product Layout Is More Optimized and Exports Continue to Rise

In recent years, the Company has been committed to improving product technology, extending the industrial chain, and broadening market channels, which has achieved obvious results. The Company has adjusted the product structure purely centered on heavy trucks to cover a variety of choices for products including heavy trucks, medium and light trucks, buses and special vehicles. Through in-depth cooperation with MAN and Weichai Power, the Company has become a heavy truck manufacturer with the most complete power and drive types in China, and has built its core competitiveness in both domestic and foreign markets. In the first half of 2022, the average sales price of the Company's heavy trucks has reached RMB318 thousand, up RMB30 thousand over 2021. With the help of high-end products SITRAK and Huanghe, the average sales price of heavy trucks is expected to continue to rise.

On 31 Dec 2022, the Company has developed approximately 240 distribution networks at all levels, approximately 250 service outlets and approximately 220 subassembly outlets in more than 90 countries and regions around the world, and established 28 overseas KD production plants, forming a marketing network system that basically covers developing countries and major emerging economies such as Africa, the Middle East, Central and South America and Southeast Asia, as well as some mature markets such as Australia and East Asia.

FY2022 result in line with warning guidelines, down 58% yoy

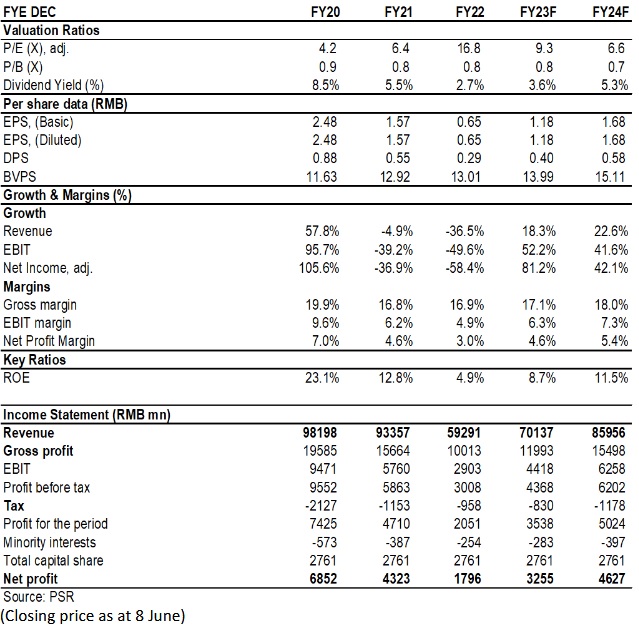

As its FY2022 result report, Sinotruk recorded the net profit attributable to the parent company decreased by 58.4% yoy to 1.8 billion yuan. The management attributed the decline in performance mainly to the fact that the domestic truck market demand declined sharply yoy due to the slowdown in macroeconomic growth, the repeated logistics problems caused by the COVID-19 in various parts of the country and other factors, leading to a significant decline in the company's product sales. We believe that the decline in sales volume led to a decline in capacity utilization, and it was difficult to dilute Fixed cost. Profitability was also affected. The decline in net profit was greater than the decline in sales volume.

The Industry Is Likely to Bottom out

In terms of the domestic economic situation, China needs to boost its economy after the pandemic. With the further implementation of the government's policies to stabilize the economy, infrastructure investment and logistics demand will maintain the momentum of rally, which will provide a foundation for the recovery of the heavy truck market. Secondly, since the implementation of the National VI emission standard in July 2021, the heavy truck industry has fallen into a downturn for one and a half year. While, the heavy trucks in the previous round of peak consumption have gradually entered the replacement period. In addition, the stricter emission regulations of the industry, the overload transportation governance, and the elimination of backward and old models will play a positive role in the recovery of the industry. In February 2023, China ended a 21-month consecutive decline in heavy truck sales, with the growth rate turning positive from negative to a yoy increase of 15%.The sales in March and April increased significantly yoy by 49.6% and 83%, respectively.

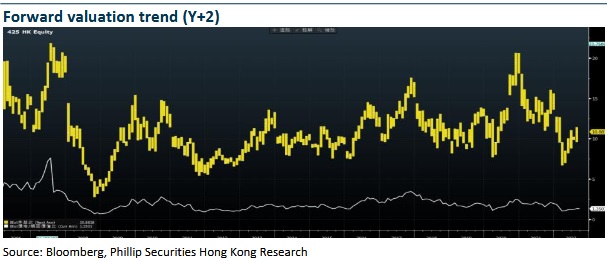

Valuation & Investment Suggestion

We expect the Company to continue to benefit from the recovery of the domestic heavy truck industry and the growth trend of the export market. In the medium to long term, there are opportunities for value enhancement in some segmentations of heavy trucks brought by innovation. We expect the Company's EPS in 2023/2024 to be 1.18/1.68 yuan, respectively, and adjust the target price to 16.1 yuan, corresponding to 12.0/8.4x P/E and 1.0/0.9x P/B in 2023/2024, a `BUY` rating. (Closing price as at 8 June)

Risk

The economic recovery was less than expected, resulting in lower than expected sales of heavy trucks

Overseas market risk, adverse exchange direction risk

Risk of significant increase in raw materials

Financials

Click Here for PDF format...