Xtep International principally engages in the design, development, manufacturing, sales, marketing and brand management of sports products covering footwear, apparel and accessories for adults and children. With a diverse brand portfolio encompassing the core Xtep brand, K-Swiss, Palladium, Saucony and Merrell to strategically target the mass market, athleisure and professional sports segments, has an extensive global distribution network and more than 8,000 stores in Asia-Pacific, North America and EMEA.

Revenue growth in FY2022 better than market expectations and ahead of peers

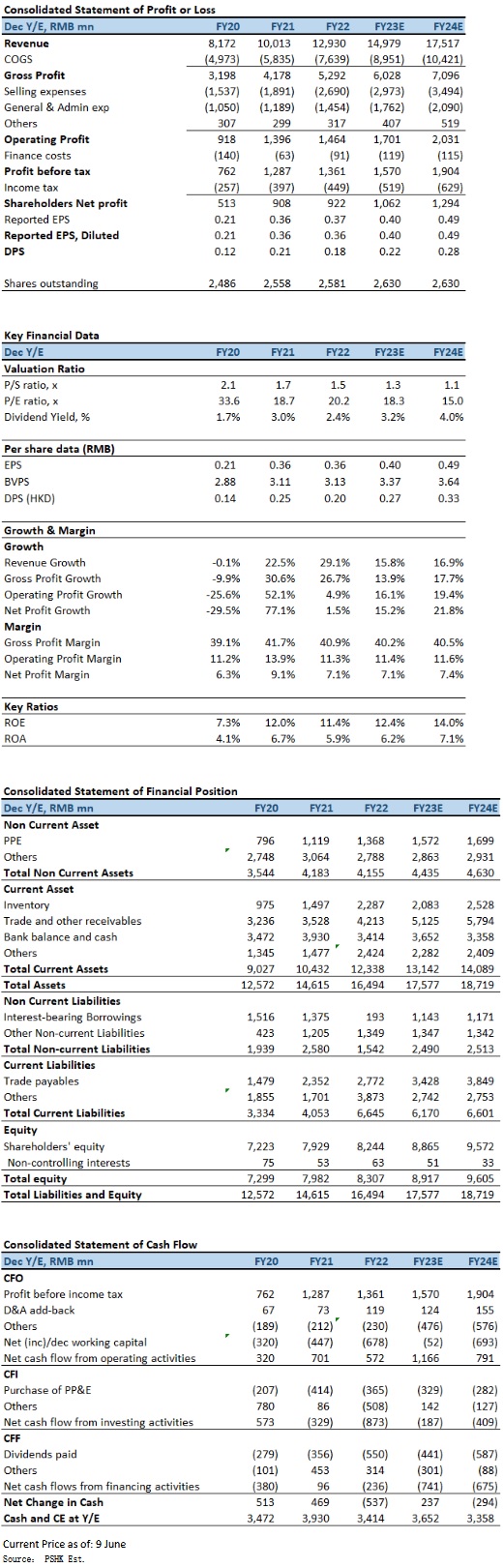

In FY2022, Xtep's revenue rose 29.1% to RMB12,930.4 million (FY2021: RMB10,013.2 million), slightly better than market expectations, and ahead of peers. Profit attributable to ordinary equity holders of reached RMB921.7 million (FY2021:RMB908.3 million), a slight increase of 1.5%. Net profit margin amounted to 7.1% (FY2021: 9.1%). Basic EPS was RMB36.6 cents (FY2021:RMB36.4 cents). The total dividend for FY2022 is HK20.1 cents (FY2021: HK25.0 cents), equivalent to a dividend payout ratio of 50.0% (FY2021: 60.0%).

During the year, overall gross profit margin decreased by 0.8 percentage points to 40.9% (FY2021: 41.7%). The decrease in the overall gross profit margin was mainly contributed by the change in product mix, margin contributions from different brands and products sold. Selling and distribution expenses amounted to RMB2,690.2 million (FY2021: RMB1,891.5 million), representing 20.8% (FY2021: 18.9%) of the total revenue. The increase mainly from the increase in advertising and promotional costs and staff costs. Due to increase in advertising campaigns, the advertising and promotional costs for the year amounted to RMB1,537.3 million (FY2021: RMB1,019.7 million), representing 11.9% (FY2021: 10.2%) of the total revenue. Although the operating profit for the year rose moderately by 4.9% to RMB1,464.3 million (FY2021: RMB1,396.2 million), due to the decrease in operating profit margin from mass market and athleisure during the year, caused the operating profit margin decreased by 2.6 percentage points.

As of 31 December 2022, the turnover days for inventories and trade payables increased by 13 days and 1 day to 90 days and 121 days respectively, while the turnover days for trade receivables decreased by 9 days to 98 days, resulting in an increase in overall working capital turnover days by 3 days to 67 days.

Professional sports brands maintain rapid growth

By brand nature, Revenue of the Mass market (signature brands: Xtep) increased by 25.9% to RMB11,128 million, accounting for 86.1% of the total revenue, and the segment operating profit increased by 9.4% to RMB1,758.6 million; Revenue of the Athleisure (signature brand: K-Swiss, Palladium) increased by 44.4% to RMB1,402.5 million, accounting for 10.8% of the total revenue, and the segment operating losses expanded by 115.3% to RMB188.7 million; Revenue of the Professional sports (signature brands: Saucony, Merrell) increased 99.0% to RMB400.0 million, segment operating loss narrowed 51.2% to RMB19.6 million.

During the year, strong consumer appetite for children's sportswear resulted in another year of accelerated growth for our Xtep Kids business. Its revenue surged 52.3% year on year to RMB1,671 million and accounted for 15.0% of the core Xtep brand's business.

Improvement of inventory turnover & discount level in 1Q2023

According to Xtep announced operating data of 1Q2023, core brand products retail sell-through (including offline and online channels) grew by 20% yoy, and the retail discount level at 30% – 25% (the same as 1Q2022, better than 30% discount at 4Q2022). Inventory turnover is less than five months (better than about five and a half months in 4Q2022). The turnover in March increased by 35% yoy, and the growth trend in March has been maintained since April. Xtep expects that the turnover performance in 2Q2023 will maintain a steady growth, and the 1H2023 core brand revenue growth target has been raised from flat to 5% - 10%.

Company valuation

With Mainland China's swift reopening after nearly three years of stringent epidemic control, the government's unprecedented efforts to promote sports development, and steady growth of sports participation and running population in the country. Xtep's professional sports brand, Saucony, is expected to achieve a break-even point this year, as it plans to open 30-50 new stores. The core Xtep brand and Xtep Kids will simultaneously open more next-generation stores, which is expected to boost store productivity and increase market share. Despite the short-term economic uncertainty triggered by the COVID-19 in China, we expect that consumer confidence will gradually recover, and we maintain a cautiously optimistic outlook for the mid-term recovery prospects of the Chinese sporting goods industry. We have upgraded our investment rating to "Accumulate", but adjusted our 2023 estimated EPS forecast to RMB0.40 (lower than our report in July 2022). Our target price is HKD 9.61, represents of 21.1x forward P/E (which is equivalent to the average P/E over the past two years).

Risk factors

1) Consumer demand recovery is slower than expected; 2) Slowdown in domestic sports apparel consumption expenditure; 3) Intensified competition in the industry; and 4) Slower-than-expected in new brands development.

Financial

Click Here for PDF format...