Originated in 1980, Baguio Green Group (“Baguio”) has developed into a group of providing integrated environmental services, ranging from Professional Cleaning, Recycling, Waste Management and Collection, Horticulture and Landscaping, and Integrated Pest Management. The company's main business is mainly divided into four segments, including: (1) Cleaning services business; (2) Waste management and recycling business; (3) Landscaping services business; and (4) Pest management business, customers cover all walks of life and different Types of institutions, such as HKSAR Government, public utilities, and private corporations.

Core cleaning services recorded a considerable growth

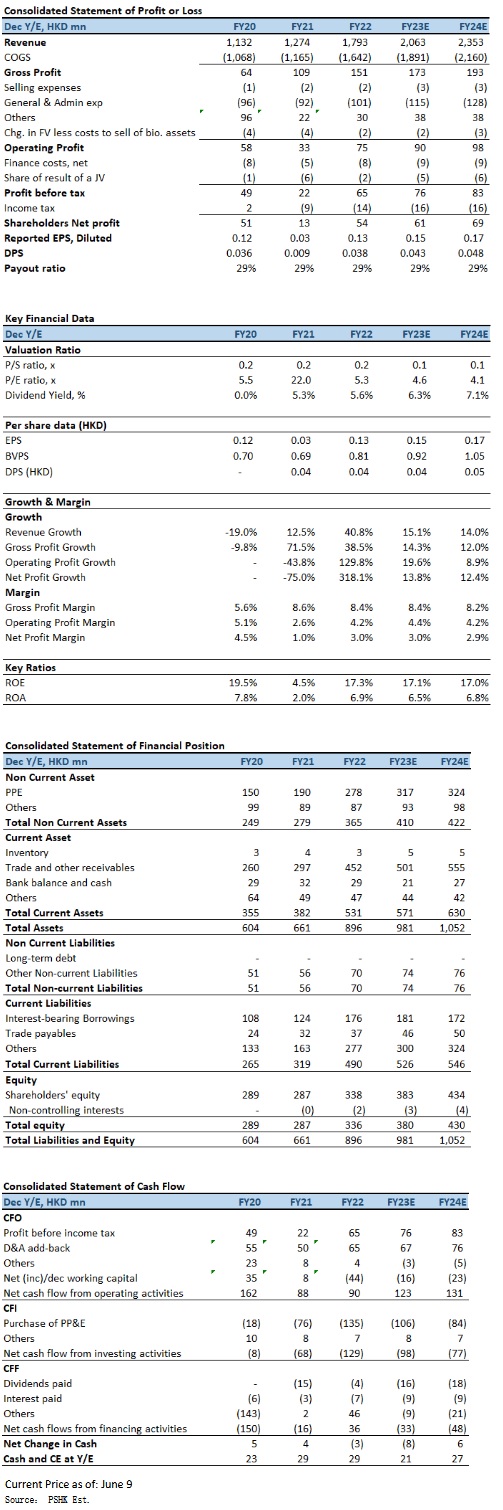

For the year ended 31 December 2022 (FY2022), Baguio's revenue was HK$1,793.1 million, representing an increase of 40.8% YoY. Profit attributable to equity shareholders amounted to HK$53.7 million (FY2021: HK$12.8 million), representing in a yoy increase of 3.2 times. EPS was HK12.9 cents (FY2021: HK3.1 cents). Final dividend for the FY2022 at HK3.8 cents (FY2021: HK0.9 cents) per ordinary share.

Gross profit increased by 38.5% to HK$151.0 million. However, the waste management and recycling segment was affected by the initial operation costs in new projects, its relevant income in short run may not be proportional to its expenditure. In addition, high service level demand in pest management services market with keen competition, together with the high energy price also affect the gross profit margin. The gross profit margin decreased by 0.2 percentage points to 8.4%.

By business segment, cleaning services, as Baguio's core business, recorded a considerable growth in 2022. Revenue of cleaning services increased by 61.2% to approximately HK$1.33 billion, accounting for 74.2% of the overall revenue during the Year. Company secured a number of service contracts worth approximately HK$1.99 billion in total for street cleansing services in Mong Kok, Sha Tin, Yuen Long, Western and Tai Po districts. Demand for cleaning services increased due to the pandemic enabled the Baguio to secure the cleaning services projects with high profit margin, which contributed to an increase in gross profit margin of cleaning business to 9.3% from 8.8% in FY2022.

With regard to the waste management and recycling business, revenue increased by 3.9% YoY to HK$243.2 million, accounting for 13.6% of total revenue. Baguio secured two new contracts with FEHD for the provision of waste collection services during the Year, worth HK$140 million. The company is contracted by the Environmental Protection Department of the HKSAR Government to handle over 5,000 recycling spots (including plastic, glass bottles, metals and waste paper) across Hong Kong. During the Year, Baguio won a new 33-month EPD Plastic Recycling Pilot Scheme contract to provide plastic collection services for three districts (Eastern, Kwun Tong and Central & Western). Baguio also provides plastic collection services for Recycling Stations of ”GREEN@COMMUNITY” and Reverse Vending Machines, which were introduced by EPD and other institutions in Hong Kong. In addition, the company also provides collection and management services of glass bottles for the Hong Kong Island, the New Territories and Islands District. Although the gross profit margin of the segment decreased by 6.0 percentage points to 3.4% from 9.4% in FY2021, with the Municipal Solid Waste (MSW) charging scheme scheduled to be launched in the second half of 2023, the recycling volume is expected to increase rapidly.

With the potential legislation of the Producer Responsibility Scheme on Plastic Beverage Containers this year, when the new regulation becomes effective, producers of plastic beverage containers will add a deposit to the selling price and refund the deposit to consumers when they return their plastic beverage containers. The recycling volume of plastic beverage containers is expected to have a significant increase. It is expected that these two programs will directly stimulate the business volume of Baguio recycling services and provide higher return.

In the landscaping services, revenue increased by 8.8% yoy to HK$122.2 million, accounting for 6.8% of total revenue; the gross profit margin of the segment increased by 4.6 percentage points yoy to 10.0%. During the year, Baguio secured a contract for the provision of landscaping services to Hong Kong University of Science and Technology and Tung Chung East Promenade.

For the pest management business, revenue decreased by 4.9% yoy to HK$97.0 million, accounting for 5.4% of total revenue; the gross profit margin of the segment decreased slightly by 0.3 percentage points yoy to 7.4%. During the year, Baguio won the FEHD's contract for pest management services in the Wong Tai Sin and Tai Po districts worth HK$150 million.

In 2022, new contracts awarded amounted to a total of HK$3.08 billion. As a result, recorded a historical high for its contracts on hand of HK$3.59 billion, representing a surge of 67.3%. In addition, the company continued to maintain a high tender success rate at 43.7% in 2022 (2021: 39.5%).

Investment Thesis

Currently, ~80% of the Baguio's revenue was generated from contracts with government and quasi-government organizations, the amount of contracts on hand (generally with a term of 2–3 years) as of 31 December 2022, ~HK$1,795.1 million will be recognized by the end of 2023 (~HK$1,164.6 million will be recognized in 2024 and the rest of ~HK$629.8 million will be recognized in 2025 and beyond), while this value is higher than the revenue for the whole year of 2022 (HK$1,793.1 million). With potential new contracts to be obtained in 2023, despite the unsatisfactory in the global macroeconomic environment, it is expected that the company's business and revenue growth in FY2023 still has high certainty. We raised the company's FY2023E-FY2024E EPS forecast to 14.7 cents and 16.6 cents, with PT of HK$1.18, implies a FY2023 Est. P/E ratio of 8.0x (in line with ~3-yrs historical average). Our investment rating is “Buy”.

Risk factors

1) Market competition intensifies; 2) Soaring in operating cost; and 3) Unexpected slowdown in service demand.

Financial

Click Here for PDF format...