Overview

China Lit(772.HK) is a comprehensive cultural industry group based on Chinese online literature and centered on IP cultivation and development as its core. Its subsidiaries include well-known brands in the industry such as QQ Reading, Qidian and New Classics Media(NCM). It has a lineup of writers and a rich reserve of literatures, covering more than 200 content categories, reaching hundreds of millions of users, and adapting a large number of web text IPs, such as Joy of Life, The King's Avatar and Soul Land, into animation, film and television and games and other products.

A review of Q3 2022 Results

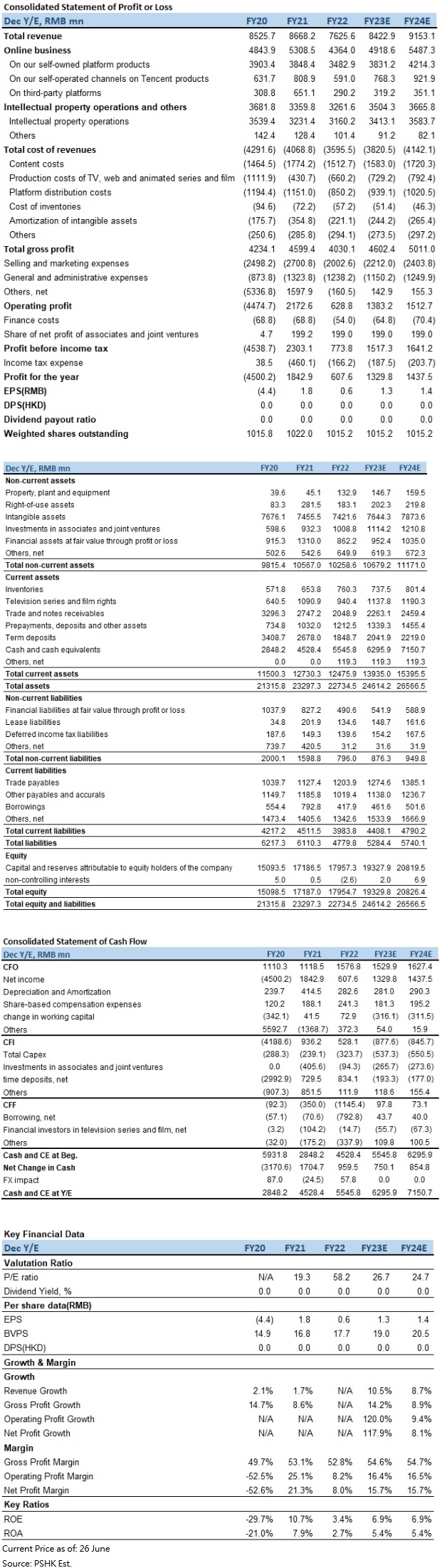

China Lit (772.HK) has announced the annual report ended December 31, 2022. The company's revenue amounted to RMB 7.6 billion, decreasing 12.0% YoY. Cost of revenue amounted to RMB 3.6 billion, decreasing 11.6% YoY. Gross profit amounted to RMB 4.0 billion, decreasing 12.4% YoY. Gross profit margin was 52.8%, slightly decreasing 0.3 percentage point YoY. Operating profit was RMB 0.6 billion, decreasing 71.1% YoY. Profit attributable to non-IFRS shareholders amounted to RMB 1.4 billion, increasing 9.6% YoY.

Revenue by Business Type

The company's business is mainly dividend into two parts, namely online business and IP operations and others. Online business revenue mainly reflects revenue from online paid reading, online advertising and distribution of third-party online games on company's platform, accounting for 57.2% of total revenue. IP operations and others mainly reflect revenues from production and distribution of TV, web and animated series, films, licensing of copyrights, operation of self-operated online games and sales of physical books, accounting for 42.8% of total revenue.

Revenue from online business on company's self-owned platform products amounted to RMB 3.5 billion, decreasing 9.5% YoY, accounting for 45.7% of total revenue, mainly due to reduced marketing spending on user acquisition as company implemented cost control and operational efficiency improvement measure for business. Despite these cost-cutting efforts, revenues from Qidian Reading, one of company core products, increased over 30% YoY, as company focused on supporting the growth of company premium products by investing in high-quality content offerings, effective anti-piracy measures, and improved product operation.

Revenues from online business on company channels on Tencent products amounted to RMB 0.6 billion, decreasing 26.9% YoY, accounting for 7.7% of total revenue, mainly attributable in part to a reduction in advertising revenues caused by broader market factors and in part to the channel optimization carried out as a part of company initiatives to improve operational efficiency.

Revenue from online business on third-party platforms amounted to RMB 0.3 billion, decreasing 55.4% YoY, accounting for 3.8% of total revenue, primarily due to the suspension of collaboration with certain third-party distribution partners.

Revenue from IP operation amounted to RMB 3.2 billion, decreasing 2.2% YoY, accounting for 41.4% YoY, mainly due to a decrease in revenues from its self-operated online game in 2022. However, company achieved solid growth in revenues from its TV and web series, films, animation series, and licensing of copyrights during the year.

Revenue from others, mainly generated by sales of physical books, amounted to RMB 0.1 billion, decreasing 21.0% YoY, accounting for 1.4% of total revenue. As the company continued to adjust its physical book business in tandem with its business development strategy.

Business features

The Chinese literature market consists of three segments, including online literature, e-books and physical books. As the company is the leader of China's online literature platform, traffic and literature are particularly important to the company's development. If the company's platform has enough traffic, it can attract more authors to enter the platform and create more literatures, and the platform has more high-quality literatures could attract more traffic, it will form a good cycle between traffic and literatures. The company's platform can not only collect copyright fees, subscription fees, and advertising fees, but also adapt popular online literature into TV series, movies, and games to fully monetize popular IPs.

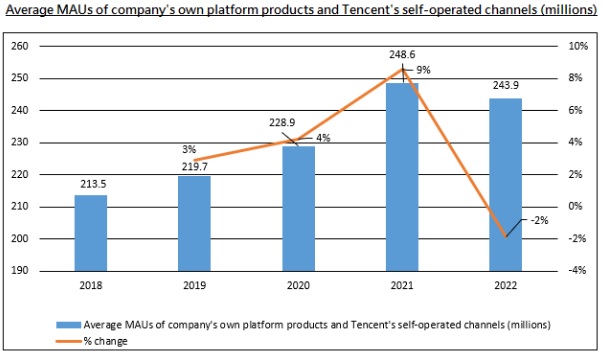

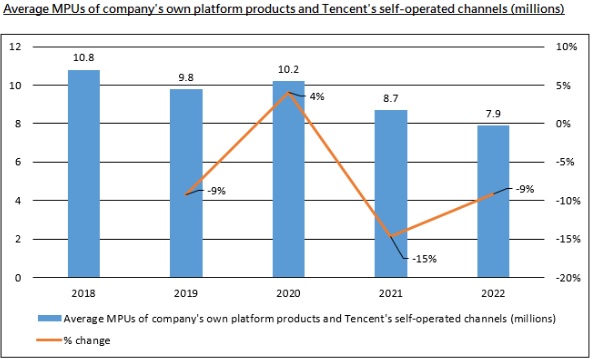

According to the 2022 China Online Literature Report, the scale of China's online literature market in 2022 amounted to RMB 38.9 billion, increasing 8.8% YoY, the number of users amounted to 0.5 billion, and the number of overseas online literature access users amounted to 0.9 billion. In terms of the company's own development, as of December 31, 2022, the average MAUs of the company's own platforms products and self-operated channels of Tencent products are 244 million, with a market share of 49.6%, representing the company's leading position in the Chinese online literature market, but only 7.9 million are premium users, and the payment rate is 3.2%, reflecting that the company is not satisfactory in monetizing active users.

User data and characteristics

Average MAUs on company self-owned platform products and self-operated channels on Tencent products have maintained a slow single-digit growth in recent years, CAGR of 3.4% from 2018 to 2022, the company's YoY growth in 2021 amounted to 8.6%, mainly due to the expansion of free reading business in Tencent's self-operated channels. However, due to the company's cost-cutting and efficiency-enhancing measures in 2022, which reduced marketing expenses related to user acquisition, the MAUs of its own platform products amounted to 110 million, decreasing to 5.8% YoY. As for the monthly active users of Tencent's self-operated channels, it remained stable, with a YoY increase of 1.6% to 133.9 million. The following figure shows the overall average MAU performance trend in the past five years:

�The average MPUs of the company's own platform products and Tencent's self-operated channels have continued to decline in recent years. It fell by 14.7% YoY to 8.7 million in 2021, mainly due to the expansion of the company's free reading business and more users reading free content. It fell by 9.2% YoY to 7.9 million in 2022, mainly due to channel optimization and the reduction of marketing to users with low return on investment. However, the company focuses on improving content supply, combating piracy in innovative ways, and enhancing the user experience of core products, so that the average MPUs of its own platform products will achieve a YoY growth of 14% in the second half of 2022. The following figure shows the overall average MPUs performance trend in the past five years:

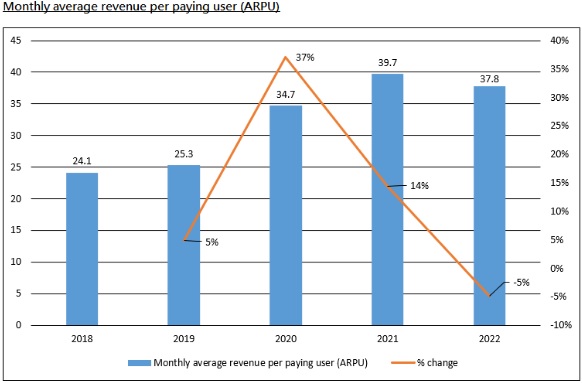

The average monthly income per paying user (ARPU) increased by 37.2% and 14.4% YoY in 2020 and 2021 respectively, mainly due to the company's continuous improvement of content operations, enriching themes of literature, optimizing community functions and improving recommendation efficiency, users are more willing to pay for high-quality content. As for 2022, it fell by 4.8% YoY to RMB $37.8, mainly due to the revenue mix of different products. The following figure shows the trend of average monthly revenue per paying user over the past five years:

Development direction and bottleneck

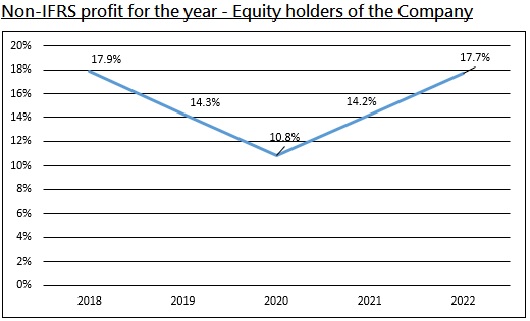

We believe that the number of digital reading users in China is gradually becoming saturated, and the company needs to work hard to increase revenue and reduce expenditure in the future as the industry's development dividends fade. In terms of cutting expenditure, the company adopt a series of cost reduction and efficiency enhancement measures in 2022 to improve operating efficiency, such as reducing online business promotion and advertising expenses. In practice, the profit margin attributable to non-IFRS company holders increased from 14.2% in 2021 to 17.7% in 2022, an increase of 2.5 percentage points. The rebound for two consecutive years reflects the effectiveness of the company's measures to reduce costs and increase efficiency. The following figure shows the trend of profit margin attributable to non-IFRS company holders in the past five years:

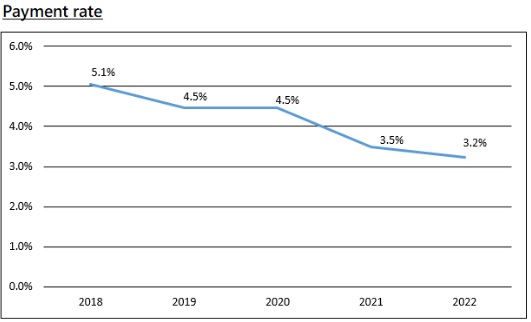

As of broaden the sources of revenue, how to increase the payment ratio and monetize popular literary IP in more channels will be the core issues that the company needs to solve. In terms of increasing the payment rate, the company's payment rate has continued to decline from 5.1% in 2018 to 3.2% in 2022. Comparted with other companies that provide online entertainment, such as Bilibili's (9626.HK) payment ratio in 2022 is 8.8%, China Lit's payment rate is about 3.2%, which is in a very low level. The following figure shows the payment rate trend of China Lit in the past five years:

China Lit's low payment rate reflects a problem that has plagued Chinese online literature for years, piracy. According to the 2021 China Online Literature Copyright Protection and Development Report, the scale of online literature losses due to piracy reached RMB 6.2 billion, an increase of 2.8% YoY. It is conservatively estimated that the scale of the online literature market has reached 17.3%. The MAUs of pirated websites are 43.71 million, accounting for 14.1% of online reading users. The report shows that more than 80% of writers have been infringed, and 96.6% of them said that being pirated has affected their creative motivation, but only 25.2% of writers are willing to take the initiative to defend their rights.

We believe that the main reason why piracy is rampant, but only a small number of writers are wiling to take the initiative to defend their rights, is that with the advancement of technology, the cost of engaging in piracy is far lower than the cost of rights protection of infringed websites. In term of piracy costs, pirate gangs only need to apply for a paid account on the genuine website, and then they can automatically download articles from the genuine website through technologies such as web crawlers and text recognition, eventually upload them to the self-built pirated website. The pirated content can also charge advertisement fees after attracting traffic, and the cost of the whole process is quite low. Only a small-scale team, or even one person can do it, and it is profitable, which makes there are still a large number of pirated websites in the mainland search engines.

On the contrary, the copyright protection cost of legitimate websites is relatively high. Genuine websites can mainly start from two aspects of law and anti-theft. Legally, if a genuine website wants to take the pirated website owner to court, certain investigations and evidence collection are required. In addition, if the owner is located overseas, it is difficult to contact the owner and issue a blocking notice, and even if the legitimate website wins the lawsuit, the compensation is often not enough for the cost of rights protection. In terms of anti-theft, it also needs to invest a considerable amount of cost. In 2022, China Lit officially raised copyright protection to the company's strategic height, and take a number of anti-theft measures, such as establishing an anti-piracy platform, calling on authors and readers to complain about pirated websites, improving the protection level of the entire platform, including using AI to identify abnormal behaviors, content encryption, reverse detection, etc.; authors are advised to open a free channel three months after the novel is released, so that readers who do not want to spend money can read the genuine version on the free website, etc.

According to the anti-theft results announced by China Lit, its website has intercepted 150 million pirated visits in one year and has carried out more than 3000 iterations of the anti-theft system. After the official launch of the anti-theft system on Qidiandushu APP, the representative of its boutique paid products, 40% of the new users converted from pirated versions within 30 days, the MAU in December 2022 increased by 80% YoY, and the annual revenue increased by 30% YoY. In addition, about 540,000 new authors and 950,000 novels were added to the company's online reading platform, and the number of new literatures with an average subscription (average subscription per chapter) of more than 3,000 on the entire platform increased by more than 50% YoY. We believe that the anti-piracy measures have achieved initial results. To a certain extent, the income of online writers can be guaranteed, so that online writers have the motivation to continuously update their literature, reduce the rate of authors stop updating, and attract more newcomers to join the online literature industry, making the ecological development of the entire industry healthier. Moreover, with the anti-piracy measures and the strengthening of mainland citizens` awareness of copyright, the payment rate of China Lit is also expected to rebound.

In terms of monetization of popular literary IPs, the company mainly releases the value of IPs through multiple channels by adapting popular literary IPs into works such as film and television, animation, and comics. In the field of film and television, the company launched a number of popular new works in 2022. For example, the Chinese New Year comedy film Too Cool to Kill, has a box office of RMB 2.62 billion, and the drama series A Lifelong Journey has set a new high in the ratings of CCTV's prime time in the past 8 years., ranking first on all lists on the entire network. The company currently plans to develop popular IP dramas in two directions. The first direction is to serialize some popular dramas, such as Joy of Life, Battle Through the Heavens and My heroic Husband is about to start filming. The second direction is cross-channel linkage, adapting popular IP dramas into animations and games, etc., to extend the popularity of these IPs, and bring more monetization opportunities for the company. In addition, the company build the framework of the IP derivatives system in 2022 and build a dedicated IP derivatives team to develop in the fields of consumer goods and trendy toys. For example, in 2022, the cumulative GMV of several statues of Battle Through the Heavens launched by the company exceeded RMB 20 million, one of the sets is limited to 688 sets, and the statue with a price of RMB 6980 was sold out after 40 minutes of pre-sale, reflecting the huge potential market for popular IP derivatives. In the future, the company will continue to develop derivatives for the popular IP in hand and explore the potential of related markets.

In the field of animation and comics, the company continues to adapt popular IPs into animations, so that its IPs could have second explosion in popularity and increase opportunities for monetization. For example, the company published popular IPs in 2022, including new season of Battle Through the Heavens and Stellar Transformations. According to the Guduo data platform, among the top 10 works on the new domestic animation popularity list on Tencent Video in 2022, 7 are adapted from the IP of China Lit. As for comics, the company will continue to increase content production capacity and accelerate the process of IP visualization. As of the end of 2022, the company has cooperated with Tencent Comics to launch more than 230 comics, some of which have become hit titles, such as Dafeng Guardian and Since the Red Moon Appeared, etc.

In the field of games, the company currently mainly cooperates with external developers to transform the IP content in hand into games. In addition, the company is also strengthening its own game development and operation capabilities. Since popular IPs have been recognized by the public in other fields, it is guaranteed that relevant themes have a certain amount of audience attention in disguise. In addition, compared with original games, IP-adapted games do not need to design additional character backgrounds and game plots, etc., which is slightly simpler in game development. We expect more IP-adapted games to be launched in the future.

Valuation and recommendation

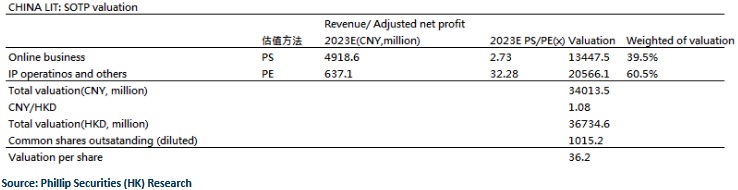

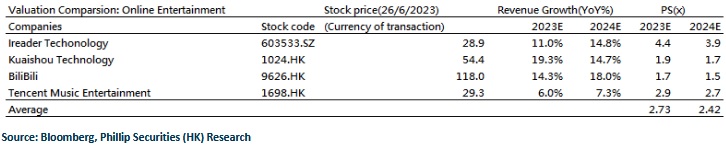

We believe that the company's series of anti-theft measures have achieved initial results and have a positive impact on the company's online literature business. However, since the piracy problem has deeply plagued the entire online literature market for many years, it is difficult to solve it. We suggest investors to continue pay attention to the subsequent impact of the anti-theft measure. As for the advertising business, as the mainland's anti-epidemic policies have been relaxed and economic activities have largely returned to normal, we expect a recovery in this segment. In terms of copyright operations, with the normalization of the approval of game licenses in the mainland, it is expected that the company will have more cooperation in converting popular IPs into games. In addition, the company will launch popular IP dramas such as Joy of Life 2 and My Heroic Husband 2 in 2023. We expect this part of the revenue to grow significantly. We use SOTP method and set a target price of HK$36.2 (calculated at RMB/HKD exchange rate of 1.08), including: 1) In line with the average P/S of other online entertainment companies (2.73x), the online business is valued at HK$14.3 per share (accounting for 39.5% of the overall valuation); 2) In line with other IP content creation company P/E average (32.3x), IP operations and other businesses are valued at HK$21.9 per share (accounting for 60.5% of the overall valuation), with a “Neutral” rating. (Current price as of June 26)

Online business: valuation per share 14.3HKD

We give the online business a 2.73x P/S valuation in 2023, which is in line with the average P/S of other online entertainment companies (2.73x). The corresponding valuation of this segment is RMB 13447.5 million, or HK$ 14.3 per share.

IP operation and others business: valuation per share 21.9 HKD

We are optimistic about the long-term monetization ability of the company's IP and give the IP operation and other businesses a 32.3x forecast P/E valuation in 2023, which is consistent with the average P/E of other IP content creation companies (32.3x). The corresponding valuation of this segment is RMB 20566.1 million, or HK$21.9 per share.

Risk factors

The piracy problem reduces the number of paying users / the weakening of IP popularity affects the monetization ability

Financial

Click Here for PDF format...