|

WEICHAI POWER(2338)

Analysis:

WEICHAI POWER (2338) has issued a positive profit alert. The Group is expected to record approximately RMB3,587 million to RMB4,065 million in the net profit attributable to the shareholders of the parent for the six months ended 30 June 2023, representing an increase of approximately 50% to 70% as compared with that for the six months ended 30 June 2022. Benefited from the improvement of the domestic economy and the thriving demand of the export market, there has been a recovery in the demand of the heavy duty truck industry in the first half of 2023. Attributable to the Group`s continuous efforts in promoting structural reform of its products and business and an intense breakthrough in the strategic market, the sales of the relevant products of the Group had recorded an accelerated trend of growth, and its strategic new business such as large diameter and hydraulic operations continued to deliver an increased contribution, which together, resulted in a substantial year-on-year increase in the Group`s performance. (I do not hold the above stock)

Strategy:

Buy-in Price: $11.90, Target Price: $13.50, Cut Loss Price: $11.20

|

STATE GRID (600131)

Analysis:

The company is positioned as a cloud network integrated service provider, including cloud network integration infrastructure, cloud platform, "Internet plus" industry cloud applications, and the actual controller is the National Grid. The company's cloud network infrastructure, enterprise digital application and power digital application accounted for 52%, 28% and 20% respectively. In 2022, the Company achieved a revenue of 7.6 billion yuan, up 2% year on year; The net profit attributable to the parent company was 802 million yuan, up 12.9% year on year. In the first quarter of 2023, it achieved a revenue of 1.323 billion yuan, a year-on-year increase of 10.36%; The net profit attributable to shareholders of the listed company is approximately 72.1 million yuan, an increase of 46.93% year-on-year. In the first half of 2022, the State Grid is building 11 ultra-high voltage projects, with a total length of 6828 kilometers and a total investment of 90 billion yuan; In the second half of the year, it is planned to start construction of eight UHV projects, with a total investment of more than 150 billion yuan, and the plan exceeds expectations. As a leading enterprise in cloud network infrastructure, the company focuses on communication infrastructure construction and is expected to fully benefit from the performance growth driven by ultra-high voltage construction.

Strategy:

Buy-in Price: RMB19.65, Target Price: RMB22.50, Cut Loss Price: RMB18.00

|

|

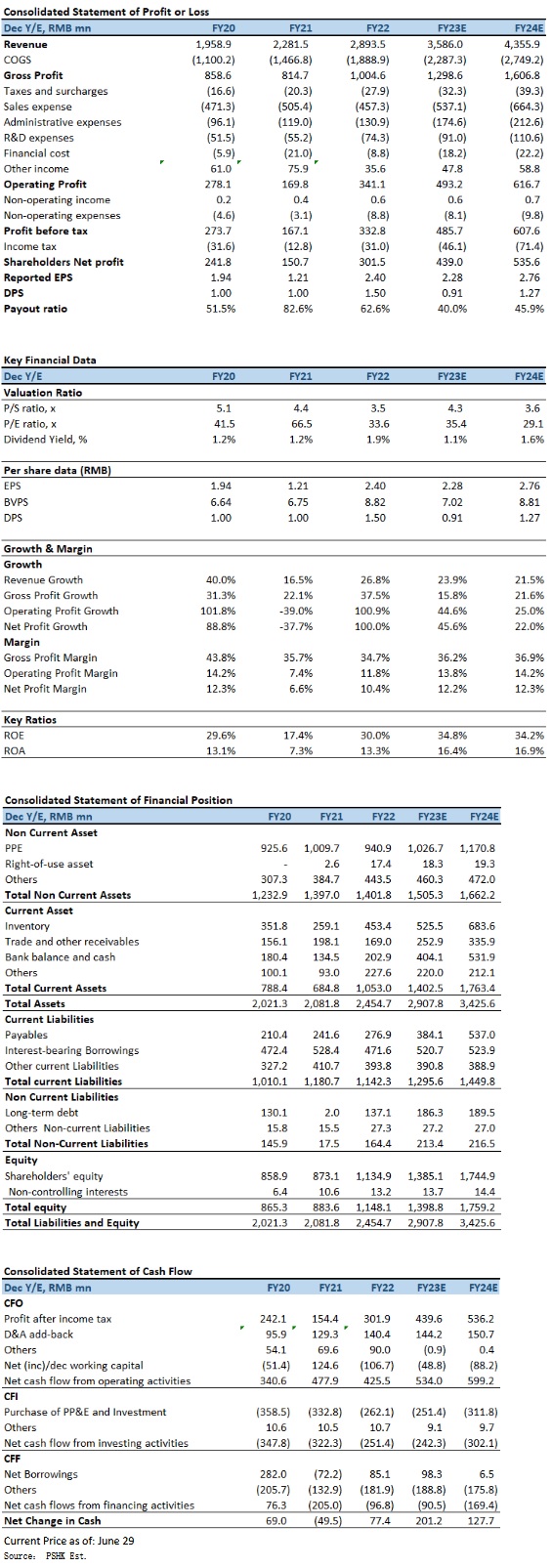

Yankershop Food Co., Limited (002847.SZ) - The results for FY2023Q1 in line with expectations, revenue growth momentum remains strong

Yankershop Food (002847.SZ), established in 2005, is a publicly traded company specializing in the research, development, production, and sales of snack foods, focusing on six core categories: spicy snacks, deep-sea snacks, baked goods, potato chips, konjac, and dried fruits. The company's snack product lines include the " Yankershop" series of savory snacks (deep-sea snacks, bean-based snacks, vegetarian snacks, meat and fish snacks, etc.) and the "Handou Baba" (憨豆爸爸) series of casual baked goods (cakes, bread, potato chips, jelly puddings, etc.). In addition to bulk packaging, the company also actively develops pre-packaged, small-sized, and large-sized products to meet the snacking needs of consumers in various scenarios. While maintaining coverage of Key-Account (KA) and AB-class supermarkets, the company also focuses on developing e-commerce, convenience stores (CVS), snack specialty stores, campus stores, and more. It has formed deep partnerships with popular snack brands such as Snack Busy (零食很忙), Snack Youming (零食有鳴), Dai Yonghong (戴永紅), Haoxianglai (好想來), Wife Lady (老婆大人), Sugar Nest (糖巢), and Best Snacks (零食優選). The company also utilizes Tiktok and livestreaming to attract customers and expand sales channels. In FY2022, Yankershop's total revenue reached RMB2.894 billion, a YoY increase of 26.83%. Net profit attributable to shareholders was RMB301 million, up 100.01% YoY. Non-GAAP Net profit was RMB276 million, a YoY increase of 201.47%. Among the product categories, all products achieved positive growth, except for dried fruit. In particular, casual baking (including snacks) generated RMB652 million in revenue, a YoY increase of 14.01%, accounting for 22.53% of operating income; deep-sea snacks generated RMB559 million in revenue, a YoY increase of 17.68%, accounting for 19.33% of operating income; meat, poultry, and egg products generated RMB 289 million in revenue, a YoY increase of 23.91%, accounting for 9.99% of operating income; potato chips generated RMB277 million in revenue, a YoY increase of 52.20%, accounting for 9.58% of operating income; and casual konjac products generated RMB257 million in revenue, a YoY increase of 120.32%, accounting for 8.90% of operating income. As of December 2022, the company had 2,483 distributors, a net increase of 734, covering all 31 provinces, autonomous regions, and municipalities in China. The revenue growth momentum for FY2023Q1 remains strong Entering Q1 FY2023, the company's business growth remained strong, with operating income reaching RMB893 million, a YoY increase of 55.37%. Net profit attributable to shareholders was RMB112 million (in line with the performance forecast of RMB100 million to RMB120 million), a YoY increase of 81.67%. Non-GAAP Net profit was RMB98.3524 million (in line with the performance forecast of RMB86.8 million to RMB106.8 million), a YoY increase of 100.33%; basic EPS were RMB0.88. The company's strong revenue growth is mainly due to the low base last year and the continuous optimization of sales products and channels (including snack specialty channels, e-commerce channels, etc.). Core product categories achieved steady growth across all channels, such as casual konjac products, which grew by 120% in FY2022 and by more than 200% in FY2023Q1. During the period, the company's gross profit margin fell by 4.0 percentage points YoY to 34.6%, mainly due to the increasing proportion of low-margin channels (such as direct-operating KA supermarkets) and the decreasing proportion of high-margin channels (such as distribution and emerging channels). As a result, the company's sales expense ratio decreased by 6.3 percentage points YoY. With the decline in both management and financial expense ratios, the company's net profit margin in FY2023Q1 increased by 1.9 percentage points YoY to 12.6%. Investment ThesisBased on the performance evaluation requirements of the company's latest incentive plan for the three fiscal years FY2023 to FY2025, compared to FY2022, the revenue/net profit growth for FY2023 should not be less than 25%/50%, for FY2024 should not be less than 56%/95%, and for FY2025 should not be less than 95%/154%. In other words, the annual growth rates of revenue for FY2023/FY2024/FY2025 are ~ 25%/25%/25%, and the annual growth rates of net profit are ~50%/30%/30%. In terms of amount, the revenue for FY2023/FY2024/FY2025 should be no less than RMB 3.617/4.514/5.642 billion, and the net profit should be no less than RMB 0.479/0.623/0.812 billion. As all revenue and net profit targets for the FY2019 to FY2021 fiscal years were achieved, it is expected that the incentive plan can continue to improve employee motivation and have a greater positive impact on the company's medium-term revenue and profit growth. Looking at global snack industry leaders, many international snack brands (such as Mondelez and General Mills) are long-term bull stocks with consumer attributes that transcend cycles. Mondelez alone has a market value of nearly US$ 100 billion. In contrast, the domestic snack market is still fragmented, so high-quality domestic brands have enormous development potential. We expect FY2023 to FY2024 EPS will be RMB2.28 and RMB2.76, respectively, and the PT will be RMB103.23, implies a FY2023E P/E of 45.4x (~3-yrs historical average minus 1 SD). Our investment rating is “Buy”. Risk factors1)The momentum of macroeconomic recovery has slowed down;2)The increase in raw material costs exceeded expectations;3)Consumption of snack food is weaker than expected. Financial

Click Here for PDF format...

| Recommendation on 4-7-2023 | | Recommendation | Buy | | Price on Recommendation Date | $ 83.340 | | Suggested purchase price | N/A | | Target Price | $ 103.230 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|