Company Profile

Haichang Ocean Park Holdings Ltd. is a leading marine-life theme park developer and operator in China. As at 31 December 2022, the Group owned and operated six marine culture-based theme parks and one theme park under construction, and authorized four theme parks to use the brand of “Haichang”.

Investment Summary

Three-year Pandemic Has Caused Pressure and Significant Decline in Performance

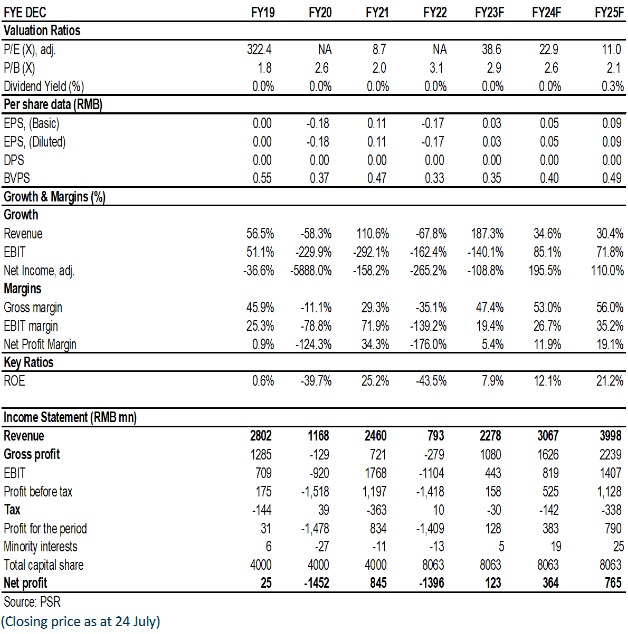

The revenue of Haichang Ocean Park decreased by 67.8% to RMB793 million (RMB, the same below) in 2022 as compared to the previous year, mainly due to the recurring pandemic affecting the prevention and control guidelines and requirements of the relevant authorities in various regions, as well as the sell-off of some of the parks at the end of 2021. Shanghai Haichang Ocean Park, the regional focus, had only 280 operating days in 2022, compared to 364 and 289 in 2021 and 2020, respectively. The EBITDA and net profit attributable showed a loss of RMB773 million and RMB1,396 million, respectively, compared to a profit of RMB2.17 billion and RMB845 million in the same period a year earlier. Excluding the impairment and divestiture of assets, the adjusted EBITDA was -RMB423 million, compared to RMB527 million in the same period of the previous year; the adjusted net profit attributable was -RMB1.06 billion, compared to -RMB570 million in the same period of last year.

From a perspective of department, excluding the RMB837 million revenue gap generated by the divestiture of parks in 2021, operating revenue of the retained parks for the year 2022 declined by 24.2% to RMB749 million, from RMB988 million in the previous year. The share of the revenue in the total rose to 94.4%. Moreover, revenue from the tourism & leisure services and solutions department decreased to RMB44.0 million, or 5.6% of the total, mainly due to lower delivery of such projects caused by the pandemic, while the decline is partially offset by that from Haichang Aquarium/Discovery Pavilion. Finally, there was no revenue from property sales during the period, compared to RMB584 million from the department in the same period last year.

In terms of operating costs, total costs fell 38.4% yoy to RMB1072 million, a smaller decline than the drop in revenue, as theme park costs are relatively fixed. As a result, the Company registered a gross loss of RMB280 million, compared to a gross profit of RMB720 million a year earlier. The gross margin fell to -35.2% from 29.3% last year, while that in the normal years before the pandemic was between 45-55%. The departmental gross margin for the theme parks hit hard by the pandemic, dropped from 23% to -39.4%. The asset-light tourism & leisure services and solutions department was also hit by the pandemic, recording a gross margin of only 15.7% in 2022.

Sales expenses slumped by approximately 62.3% yoy to RMB85.0 million, mainly due to the significant reduction in sales and marketing expenses during the pandemic and the expenses of the parks divested that were no longer recorded. Administrative expenses fell by approximately 47.2% to RMB606 million, mainly caused by a higher base last year and the expenses of the parks divested that were no longer recorded. Similarly, financial expenses decreased by 35.7% yoy to RMB315 million due to the sell-off of assets for debt repayment, which significantly reduced debt ratio and financial pressure.

With the Gradual Recovery of Tourism Demand after the Pandemic, Shanghai Park Has Recovered Rapidly and Its Performance Is Expected to Rebound

After the pandemic, along with the accelerated recovery in the consumer market, the domestic tourism market has fully rallied since 2023, and the Company's theme parks have seen a rapid rebound in various business types. According to data released by the Company, the average daily number of visitors received by its theme parks during the May Day period recovered to 104.9% growth over the same period in 2019, with an increase of 73.5% in turnover. During the Dragon Boat Festival, the number of visitors received by the parks increased by more than 20% compared with the same period in 2019, including a 40% increase in Shanghai Park. In addition, due to the faster recovery of individual travel compared to group travel and the continuous implementation of IP, the unit price has seen a sharp rise compared with that in the past. In addition to the rapid rebound of the existing projects, the Haichang Jinqiao Penguin Hotel adjacent to Shanghai Park is set to open in 2024. Phase II project of Shanghai Park, under expansion through an asset-light model, is expected to open in 2025 and will encompass elements such as hot spring hotel, ocean hotel, ocean discovery centre, and commercial street, and the Phase II project is also under planning. The capacity of the Shanghai Park and the stay time of tourists will then be enhanced. What's more, Zhengzhou Park, with a total area equivalent to 140% of Shanghai Park, is in the final stage of construction, with Phase I expected to open in H2 of 2023 and Phase II in 2024. The 2-hour transportation circle can include 450 million people. The Company's theme park business is rapidly taking off again as new flagship projects are put into operation, which are expected to gradually turn the huge investment made in the previous years into revenue.

Asset-light Projects Are Accelerating and IP Strategy Is Developing Further

In terms of asset-light business, the Company has nearly 20 years of experience in cultural and tourism operation, and is able to provide mature solutions for the entire industry chain. The Boutique Ocean Pavilion is an asset-light project system that the Company is currently promoting rapidly. Since the first batch of 5 Haichang Aquariums/Discovery Pavilions came out on May 1, 2022, 25 have been developed by the end of April 2023. It is expected to reach 50 by the end of this year, and in the future, it is planned to put 100 into operation in 3-4 years. In addition, the Children's Ice and Snow Centre, jointly constructed and operated by the Company in April this year, opened in Shenzhen. It is another asset-light project system launched by the Company and is expected to be successfully replicated and promoted in the future. We believe that the operation of asset-light projects will gradually improve the Company's gross margin and ease the financial pressure.

In recent years, the Company has been focusing on building a new growth curve with IP as the core, and is now developing further, including continuously enriching the existing IP, introducing and developing external IPs such as Ultraman/One Piece/Baby Shark/Making Havoc in Heaven, and creating its own IPs, such as Sea-Land Mecha. In July 2022 and January 2023, the world's first Ultraman-themed entertainment zone and hotel opened in Shanghai Park, making remarkable results in enriching the playing experience, enhancing the loyalty of tourists and increasing the proportion of secondary sales. With the rapid replication of the core IP-driven strategy and model innovation in other Haichang parks, IP Operation and New Consumption is accelerating to become a new driver of profit growth.

Investment Thesis

The Company has gradually formed a multi-level business ecosystem development direction for the theme park operation, the IP operation and expansion, the tourism & leisure services and solutions output business. China's marine-life theme park industry has huge growth prospects and high barriers to entry. The Company's business belongs to the industry's first echelon, and it is expected to continue to benefit from the prosperity of domestic tourism consumption in the future.

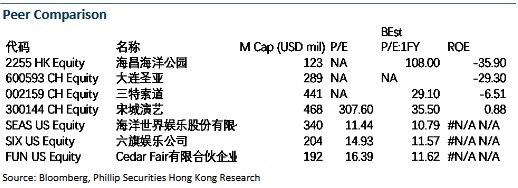

We expect the company's net profit for 2023/2024/2025 to reach 123/364/765 million yuan and the target price of HK$1.5, corresponding to 2023/2024/2025 51.3/30.3/14.6x P/E, Buy rating. (Closing price as at 24 July)

Financials

Click Here for PDF format...