Sectors:

Air & Automobiles (Zhang Jing)

TMT, Semiconductors, Consumer & Healthcare (Eric Li)

Automobile & Air (ZhangJing)

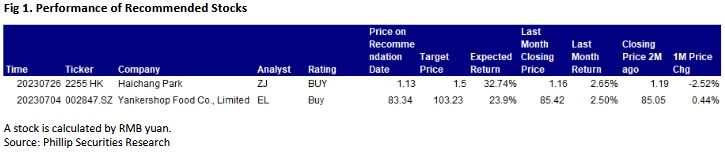

This month I released updated reports of Haichang Ocean Park (2255.HK).

Haichang Ocean Park Holdings Ltd. is a leading marine-life theme park developer and operator in China. As at 31 December 2022, the Group owned and operated six marine culture-based theme parks and one theme park under construction, and authorized four theme parks to use the brand of “Haichang”.

The revenue of Haichang Ocean Park decreased by 67.8% to RMB793 million (RMB, the same below) in 2022 as compared to the previous year, mainly due to the recurring pandemic affecting the prevention and control guidelines and requirements of the relevant authorities in various regions, as well as the sell-off of some of the parks at the end of 2021. The EBITDA and net profit attributable showed a loss of RMB773 million and RMB1,396 million, respectively, compared to a profit of RMB2.17 billion and RMB845 million in the same period a year earlier. Excluding the impairment and divestiture of assets, the adjusted EBITDA was -RMB423 million, compared to RMB527 million in the same period of the previous year; the adjusted net profit attributable was -RMB1.06 billion, compared to -RMB570 million in the same period of last year.

After the pandemic, along with the accelerated recovery in the consumer market, the domestic tourism market has fully rallied since 2023, and the Company's theme parks have seen a rapid rebound in various business types. According to data released by the Company, the average daily number of visitors received by its theme parks during the May Day period recovered to 104.9% growth over the same period in 2019, with an increase of 73.5% in turnover. During the Dragon Boat Festival, the number of visitors received by the parks increased by more than 20% compared with the same period in 2019, including a 40% increase in Shanghai Park. In addition, due to the faster recovery of individual travel compared to group travel and the continuous implementation of IP, the unit price has seen a sharp rise compared with that in the past. What's more, Zhengzhou Park, with a total area equivalent to 140% of Shanghai Park, is in the final stage of construction, with Phase I expected to open in H2 of 2023 and Phase II in 2024. The 2-hour transportation circle can include 450 million people. The Company's theme park business is rapidly taking off again as new flagship projects are put into operation, which are expected to gradually turn the huge investment made in the previous years into revenue.

In recent years, the Company has been focusing on building a new growth curve with IP as the core, and is now developing further, including continuously enriching the existing IP, introducing and developing external IPs such as Ultraman/One Piece/Baby Shark/Making Havoc in Heaven, and creating its own IPs, such as Sea-Land Mecha. In July 2022 and January 2023, the world's first Ultraman-themed entertainment zone and hotel opened in Shanghai Park, making remarkable results in enriching the playing experience, enhancing the loyalty of tourists and increasing the proportion of secondary sales. With the rapid replication of the core IP-driven strategy and model innovation in other Haichang parks, IP Operation and New Consumption is accelerating to become a new driver of profit growth.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released report of Yankershop Food Co., Limited (002847.SZ).

Yankershop Food (002847.SZ), established in 2005, is a publicly traded company specializing in the research, development, production, and sales of snack foods, focusing on six core categories: spicy snacks, deep-sea snacks, baked goods, potato chips, konjac, and dried fruits. The company's snack product lines include the " Yankershop" series of savory snacks (deep-sea snacks, bean-based snacks, vegetarian snacks, meat and fish snacks, etc.) and the "Handou Baba" (憨豆爸爸) series of casual baked goods (cakes, bread, potato chips, jelly puddings, etc.). In addition to bulk packaging, the company also actively develops pre-packaged, small-sized, and large-sized products to meet the snacking needs of consumers in various scenarios.

In FY2022, Yankershop's total revenue reached RMB2.894 billion, a YoY increase of 26.83%. Net profit attributable to shareholders was RMB301 million, up 100.01% YoY. Non-GAAP Net profit was RMB276 million, a YoY increase of 201.47%.

Entering Q1 FY2023, the company's business growth remained strong, with operating income reaching RMB893 million, a YoY increase of 55.37%. Net profit attributable to shareholders was RMB112 million (in line with the performance forecast of RMB100 million to RMB120 million), a YoY increase of 81.67%. Non-GAAP Net profit was RMB98.3524 million (in line with the performance forecast of RMB86.8 million to RMB106.8 million), a YoY increase of 100.33%; basic EPS were RMB0.88.

The company's strong revenue growth is mainly due to the low base last year and the continuous optimization of sales products and channels (including snack specialty channels, e-commerce channels, etc.). Core product categories achieved steady growth across all channels, such as casual konjac products, which grew by 120% in FY2022 and by more than 200% in FY2023Q1. During the period, the company's gross profit margin fell by 4.0 percentage points YoY to 34.6%, mainly due to the increasing proportion of low-margin channels (such as direct-operating KA supermarkets) and the decreasing proportion of high-margin channels (such as distribution and emerging channels). As a result, the company's sales expense ratio decreased by 6.3 percentage points YoY. With the decline in both management and financial expense ratios, the company's net profit margin in FY2023Q1 increased by 1.9 percentage points YoY to 12.6%.

Based on the performance evaluation requirements of the company's latest incentive plan for the three fiscal years FY2023 to FY2025, compared to FY2022, the revenue/net profit growth for FY2023 should not be less than 25%/50%, for FY2024 should not be less than 56%/95%, and for FY2025 should not be less than 95%/154%. In other words, the annual growth rates of revenue for FY2023/FY2024/FY2025 are ~ 25%/25%/25%, and the annual growth rates of net profit are ~50%/30%/30%. In terms of amount, the revenue for FY2023/FY2024/FY2025 should be no less than RMB 3.617/4.514/5.642 billion, and the net profit should be no less than RMB 0.479/0.623/0.812 billion. As all revenue and net profit targets for the FY2019 to FY2021 fiscal years were achieved, it is expected that the incentive plan can continue to improve employee motivation and have a greater positive impact on the company's medium-term revenue and profit growth.

Click Here for PDF format...