|

TAI HING GROUP(6811)

Analysis:

Tai Hing Group (6811) implements a multi-brand strategy. Apart from its flagship “Tai Hing” brand, the Group has launched, acquired and licensed multiple brands, including “Men Wah Bing Teng ”, “TeaWood”, “Asam Chicken Rice”, “Trusty Congee King”, “Phở Lê”, “Dao Cheng”, “Dimpot”, “Dumpling Station”, “King Fong Bing Teng”, “Tommy Yummy”, “Tori Yoichi” and “Sing Kee Seafood Restaurant”. As at 31 December 2022, the Group had a network of 209 restaurants, among which, 207 restaurants were operated by the Group and 2 restaurants were operated by its franchisee. The Group had 158 restaurants and 50 restaurants in Hong Kong and Mainland China, respectively, and one restaurant in Macau. According to its positive profit alert, the Group is expected to record profit attributable to the Shareholders in the range of approximately HK$43 million to HK$47 million for the six months ended 30 June 2023, as compared to a loss attributable to the Shareholders of approximately HK$52 million for the six months ended 30 June 2022. The expected turnaround from loss to profit was mainly due to the following: (1) the revenue of the Group arising from its businesses in both Hong Kong and Mainland China increased during the Review Period. The increase in revenue was mainly attributable to (a) the Group continuing to streamline its restaurant network, backed by its well established multi-brands strategy and enhanced product offering which helped secure income; and (b) the increase in the number of operating days during the Review Period as compared to the corresponding period in 2022 and that the local economy gradually recovered in the first half of the year and the consumption atmosphere improved accordingly with the improvement in visitors flow to Hong Kong and Mainland China as a result of the lifting of travel restrictions and social distancing measures in relation to the COVID-19 pandemic since January 2023; and the Group continued to implement various constructive cost-control measures such as adopting a more cautious approach when choosing new store location, exercising reasonable control on food costs and optimising organizational structure as well as actively optimizing internal management and restaurant network. These measures helped improve the operating efficiency of the Group and also increase the gross profit margin and profit. (I do not hold the above stock)

Strategy:

Buy-in Price: $0.95, Target Price: $1.05, Cut Loss Price: $0.90

|

CANVEST ENV(1381)

Analysis:

In 2022, Canvest Environmental Protection Group (01381) revenue increased by 21.4% year-on-year to HK$8,246.6 million, and the profit attributable to equity holders of the company increased by 0.8% year-on-year to HK$1,332.8 million. The increase in revenue was mainly contributed by the increase in power sales and waste treatment fees from operating plants and the construction revenue from the additional projects. During the year, the company innocuously treated 13,993,553 tonnes of waste, generated 5,249,545,000 kWh of green energy, offset 6,769,000 tonnes of carbon dioxide equivalent emissions, and saved 1,381,000 tonnes of standard coal. In addition, the company had secured 38 WTE projects with a total daily MSW processing capacity of 56,740 tonnes. The company has a total of 31 projects in operation with a total daily MSW processing capacity of 41,890 tonnes, of which phase 1 of Linfen WTE plant, Baoshan WTE plant, Taizhou WTE plant and phase 1 of Dazhou WTE plant were put into trial operating during the year with an increase of 6,650 tonnes in daily processing capacity. Against the backdrop of diminishing national subsidies, stringent environmental supervision, and insufficient waste supply, the company would continue to promote its "Incineration +" model, gradually transitioning from the growth in "quantity" to the enhancement in "quality". Through enhance operating efficiency which will in return promote the benign cycle of project production and operation.

Strategy:

Buy-in Price: $4.60, Target Price: $4.94, Cut Loss Price: $4.31

|

|

Vinda International (3331.HK) - Revenue growth in 2Q slows down, 1H profit margins still under pressure

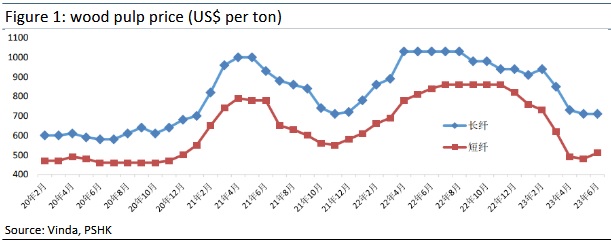

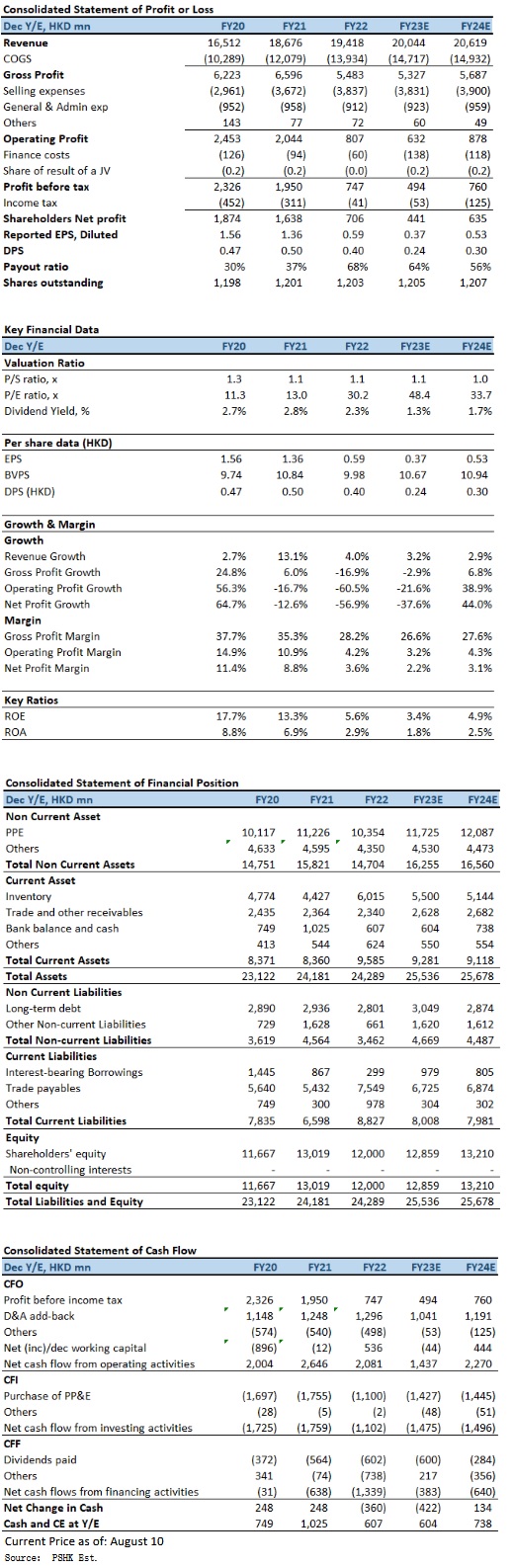

Vinda is a leading hygiene company in Asia, with core business segments including tissue, incontinence care, feminine care, baby care and professional hygiene solution under key brands Vinda, Tempo, Tork, TENA, Dr. P, Libresse, Libero and Drypers. Revenue growth in 2Q slows down, 1H profit margins still under pressure In 1HFY2023, total revenue of Vinda amounted to HK$10,070 million, representing an increase of 10.1% organically and of 4.0% (presented in Hong Kong Dollar). 1Q and 2Q revenues were HK$4,969 million and HK$5,101 million, a year-on-year increase of 15.5% and 5.5% respectively. 1H Net profit declined by 81.1% to HK$121 million. The net profit margin narrowed by 5.4 ppts to 1.2%. Basic EPS was 10.0 HK cents (1HFY2022: 53.0 HK cents), and an interim dividend of 10.0 HK cents (1HFY2022: 10.0 HK cents) per share. Despite the gradual reduction of the pulp prices since the end of 2022, costs in the first half of the year were still impacted by the inventories with relatively high price, and on gross margin, which decreased by 6.9 ppts year-on-year to 25.1%. Gross profit was down by 18.5% to HK$2,527 million. EBITDA fell by 42.3% to HK$818 million while EBITDA margin was narrowed by 6.5 ppts to 8.1%. Total foreign exchange loss was HK$0.3 million (H1 2022: HK$22.4 million loss), of which HK$5.4 million loss came from operating activities (H1 2022: HK$26.2 million loss), and HK$5.1 million gain was due to financing activities (H1 2022: HK$3.8 million gain). In terms of business segments, revenue from tissue segment amounted to HK$8,361 million in 1HFY2023, which delivered a year-on-year increase of 5.0% or an organic sales growth of 11.5%, representing 83% of Vinda's total revenue (1HFY2022: 82%). The gross margin of tissue segment was 23.8% during this Period (H1 2022: 31.6%). Vinda adhered to focus on premium categories, resulting in a double-digit growth of the premium tissue portfolio in mainland China as well as an increasing proportion of revenue. The impact from the high-cost wood pulp inventory and promotion had been relieved to an extent by the premium categories for its relatively higher profit margin. Revenue from the personal care business decreased by 0.5% to HK$1,708 million in 1HFY2023, which was a 3.7% increase at constant exchange rates and represented 17% of the Vinda's total revenue (1HFY2022: 18%), revenue by category was HK$556 million for baby care, HK$400 million for feminine care and HK$752 million for incontinent care. Gross margin of the personal care segment was 31.2% (1HFY2022: 34.1%), of which baby care was 24.0%, feminine care was 46.7% and incontinent care was 28.2%. In terms of capacity planning, the annual designed production capacity of the Vinda's papermaking facilities was 1,390,000 tons as at 30 June 2023. The Southeast Asia regional headquarters in Malaysia was officially put into operation on 16 December 2022. It is Vinda's first overseas innovation and R&D centre, which would help Vinda to accurately meet consumer demand in the Southeast Asian market and strengthen its regional supply chain footprint, improving Vinda's production and sales efficiency in Southeast Asia. In terms of sales channel, traditional distributors, key accounts managed supermarkets and hypermarkets, B2B corporate customers and e-commerce platforms accounted for 24%, 21%, 9% and 46%, respectively, of the total revenue. The e-commerce revenue recorded the most significant growth with an organic increase1 of 23.6% year-on-year. Despite the gradual reduction of the pulp prices in the first half of the year, due to inventory cycle factors, the expected cost reduction trend will not be reflected until the second half of the year.

Company valuationeconomic recovery and consumer sentiment remain uncertain, we adjusted the gross profit margin forecasts for 2023 to 2024 from 30.2% / 31.1% to 26.6% / 27.6% respectively, and further lowered the company's EPS forecast for FY2023E-FY2024E to 36.6 cents and 52.8 cents respectively (lowered by 50.3% and 43.9% compared to the report in March 2023), with TP HKD$9.78, implies a FY2024E P/E of 18.6x, in line with its 5-years average +1SD. Our investment rating is “Sell”. Risk factors1) wood pulp prices rise more than expected; 2) Large fluctuations in RMB; 3) Economic recovery momentum slower than expected, consumer confidence weakens further; and 4) Industry competition is intense than expected. �Financial

Click Here for PDF format...

| Recommendation on 15-8-2023 | | Recommendation | Sell | | Price on Recommendation Date | $ 17.700 | | Suggested purchase price | N/A | | Target Price | $ 9.780 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|