Company Profile

Minth Group is a world-renowned supplier engaged in the design, manufacturing and sales of automotive interior and exterior trim and body structure parts. The domestic market share of its core products exceeds 30%. The company has production bases in China, the United States, Mexico, Thailand, Germany, Serbia and other countries, and its customers cover major vehicle companies in the market. Based on a variety of new materials and surface treatment technologies, in recent years the company has developed new electrified and smart product lines such as aluminum power battery boxes and smart front faces, forming a series of competitive terminal products.

Investment Summary

Performance in 2022H2 Grows by 38.5% yoy, with a Significant hoh Improvement

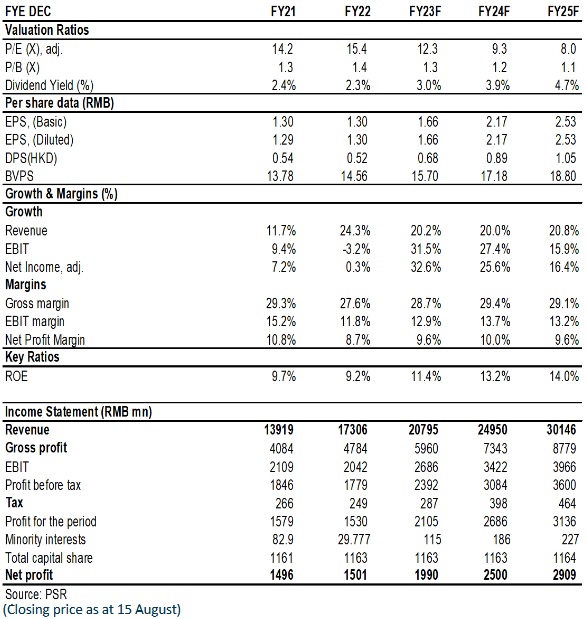

Minth Group (hereinafter referred to as the “Group”), in 2022, recorded a total revenue of RMB17,306 million, which was up by 24.3% year-on-year and better than our expectations (RMB17.2 billion). The net profit attributable to the parent company amounted to RMB1.5 billion, which increased by 0.3% year-on-year and was slightly lower than our expectation of RMB1.59 billion, mainly resulting from the gross margin in the second half of the year slower than our expectations. The Group's revenues in the first and second half of the year were RMB7.25 billion and RMB10.1 billion, with year-on-year increases of 8.9% and 38.5%, respectively. The net profits attributable to the parent company stood at RMB660 million and RMB840 million, decreasing by 27% and increasing by 48% year-on-year, respectively. Less the influencing factors in 2021, such as the one-off gains due to the disposal of subsidiaries in the same period and relocation, the Group's actual growth rate of the net profit attributable to the parent company was up to 41%.

Overseas Business Grows Rapidly by 37%, and Battery Housing Business Rises by More than Six Times

Driven by the overseas business with clients, such as BMW, Mercedes-Benz, Volkswagen, and General Motors, and the continuous mass production of the new overseas plants, the Group's revenue from overseas markets reached RMB7.8 billion, with an annual increase of approximately 36.5%, which was faster than the domestic business, made up for the decreased growth of the domestic business. It accounted for 45.1% of the total revenue of the Group, representing an increase when compared to 41.1% in 2021.

The domestic revenue of the Group was RMB9.5 billion, representing a year-on-year increase of 15.9%, whose proportion dropped by 4 percentage points to 54.9%, which was primarily due to the mass production in battery housing for multiple OEM customers and the growth in the Chinese OEM business.

The revenues of the four products of the Group, namely metal and trim products, plastic products, aluminium products, and battery housing products, amounted to RMB5.31 billion, RMB4.78 billion, RMB3.79 billion, and RMB2.04 billion, up by 6.9%, 14.4%, 14.6%, and 658.3% year-on-year, respectively.

The Gross Profit Margin Decreased by 1.7 Percentage Points, and the Expense Ratio Declined Slightly

This was mainly due to factors such as changes in product structure (i.e., the growth of battery-housing, body and chassis components and modular product business), and the increasing percentage of revenue from certain overseas companies during their ramp-up period, despite that the Group benefited from improved economies of scale driven by revenue growth, which resulted in the decrease of overall gross profit margin. During the Period, the Group's overall gross profit margin was approximately 27.6%, representing a decrease of approximately 1.7 percentage points from 29.3% in the previous year. In this regard, the Group promoted supply chain integration and adopted measures such as lean production and technology upgrade to continuously improve production efficiency and production yield, so as to partially offset the decrease in the overall gross profit margin. In particular, the gross profit margin of battery-housing products has recorded a significant improvement.

The gross profit margins of the four products of the Group, namely metal and trim products, plastic products, aluminium products, and battery housing products, were 26.3%, 24.2%, 34%, and 18.8%, respectively, with year-on-year decreases of 1.5%, 0.8%, and 0.04%, and a year-on-year increase of 8.1%. Thanks to the constant yield growth, the gross profit margin of battery housing products will continue benefiting from the scale effect, and is expected to jump to 23% or higher in 2023.

Throughout the year, the total selling, administration and R&D expense ratio dropped by 1.7 percentage points year-on-year to 19.3%. Specifically, the selling expense ratio decreased by 0.3 percentage points year-on-year, while the administration expense ratio declined by 1.4 percentage points year-on-year, reflecting the improvement of operating efficiency and the reduction of options tariff. In consideration of the pandemic and the increased ocean freight in the first half of the year, the Group controlled its expenses well. The R&D expense ratio remained the same, 6.8%, as that of the previous year.

Battery Housing Business Is Going through an Explosive Period, and New Orders Hit a New High

Upon years of input and accumulation, the battery housing business has made a great leap forward in both revenue and operational efficiency. Its revenue increased by more than 650% year-on-year to RMB2,044 million, and its segment margin further improved to 18.8%. During the Period, the Group won an order for battery housings of a major global platform vehicle model of Mercedes-Benz, and increased its battery housing business share in BMW. Meanwhile, it secured orders for battery housing of two platform models from Stellantis. Besides, as for the Group's NEV start-up customers, the Group also secured orders for battery housing from Lucid, XPeng and Li Auto. Moreover, in the business of composite material housing cover, the Group secured orders from GAC Motor and EVE Energy. With respect to intelligent products, the Group secured orders for illuminated emblems and illuminated grilles from clients such as Geely, Volkswagen and General Motors, and won an order for smart B pillar cover assembly from a Chinese OEM. It also successfully secured orders for intelligent tailgates from Nissan and XPeng.

Annualized new order intake reached a new high. The annualized revenue stood at RMB15.6 billion. The current order backlog rose by RMB49 billion to RMB199 billion from the end of the previous year. Based on the expectations of constantly strong growth of business such as the battery housing business, the Management set a goal of an increase of 20% in revenue in 2023.

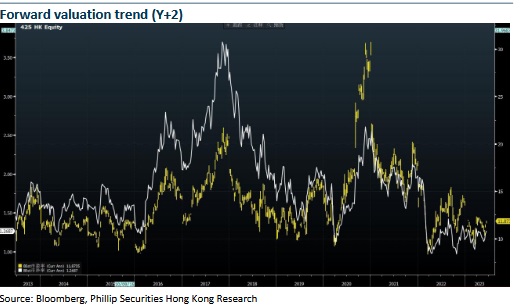

Valuation

We slightly decreased the expected earnings per share for 2023/2024 to 1.66/2.17(vs 1.81/2.19), taking into account the pressure on the overall gross profit margin from new business during the ramp-up period and the new opportunities brought by the growth of the new energy market in North America to leading suppliers of parts like the Group.

We believe that it is reasonable to give the Company a valuation of 15.3/11.6/10x P/E and 1.6/1.5/1.3x P/B for 2023/2024/2025, equivalent to target price of HK$ 28 and BUY rating. (Closing price as at 15 August)

�Financials

Click Here for PDF format...