|

MEITU(1357)

Analysis:

Meitu (1357) achieved a turnaround in the first half of 2023. Net profit attributable to the owners of the Company was RMB227.6 million for the six months ended June 30. Adjusted net profit attributable to owners of the Company was RMB151.3 million, growing 320.4% year-over-year. Besides non-cash gains from reversal of impairment losses of cryptocurrency positions, the growth is driven by subscription revenues related to its Artificial Intelligence-Generated Content (“AIGC”)-powered photo, video and design products. As of June 30, 2023, VIP users of its apps added up to over 7.2 million, increasing by 44% year on year, with a payment penetration rate of approximately 2.9%. The Company's total revenue increased by 29.8% to RMB1,260.9 million in the first half of 2023. Since the beginning of 2023, the Comapny has been consistently launching new AIGC features such as AI Anime, AI Doodle, AI Posters and AI Portraits, etc. Apart from launching new standalone AIGC features such as AI Portraits, it has also systematically added AIGC features into the core image and video editing work flow. These features include AI Removal, AI Image Quality and AI Background Expansion etc. Looking ahead, it will continue to execute its integrated AIGC strategy, launching more apps and features that address the productivity use cases, as well as optimizing its pricing strategies. There will be ample room for both subscriber penetration and ARPPU to grow in the future. (I do not hold the above stock)

Strategy:

Buy-in Price: $2.90, Target Price: $3.30, Cut Loss Price: $2.75

|

Proya(603605)

Analysis:

The company released the semi-annual results of 2023. In the first half of 2023, the operating income was 3.627 billion yuan, a year-on-year increase of 38.12%, the net profit attributable to the parent company was 499 million yuan, a year-on-year increase of 68.21%, the gross profit rate was 70.51%, a year-on-year increase of 2.39 pct, and the net profit rate was 14.56%, a year-on-year increase of 2.81pct. In the second quarter, the revenue was 2.005 billion yuan, a year-on-year increase of 46.22%, and the net profit attributable to the parent company was 291 million yuan, a year-on-year increase of 110.41%. The gross profit rate was 70.90%, a year-on-year increase of 2.27 pct. The net profit rate was 15.26%, a year-on-year increase of 5.12pct. The main brand is growing rapidly, and the sub-brands are growing at double digits. The main brand Proya achieved revenue of 2.892 billion yuan, a year-on-year increase of 35.86%. Caitang achieved revenue of 414 million yuan, a year-on-year increase of 78.65%. Off&Relax achieved revenue of 97 million yuan, a year-on-year increase of 94.17%. Yuefuti achieved revenue of 132 million yuan, a year-on-year increase of 64.80%. The reason for the increase in revenue is that the company's e-commerce channel refinement operation ability has been demonstrated, the unit price of customers and repurchase rate have increased, the gross profit margin has increased, and the asset impairment loss has been eliminated this year. We are optimistic about the company's long-term development.

Strategy:

Buy-in Price: RMB111.75, Target Price: RMB121.00, Cut Loss Price: RMB102.80

|

|

Oriental Energy (002221.SZ) - The leading position of PDH manufacturing is stable, and the profit is gradually restored

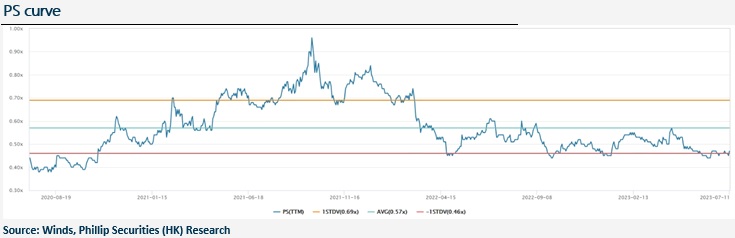

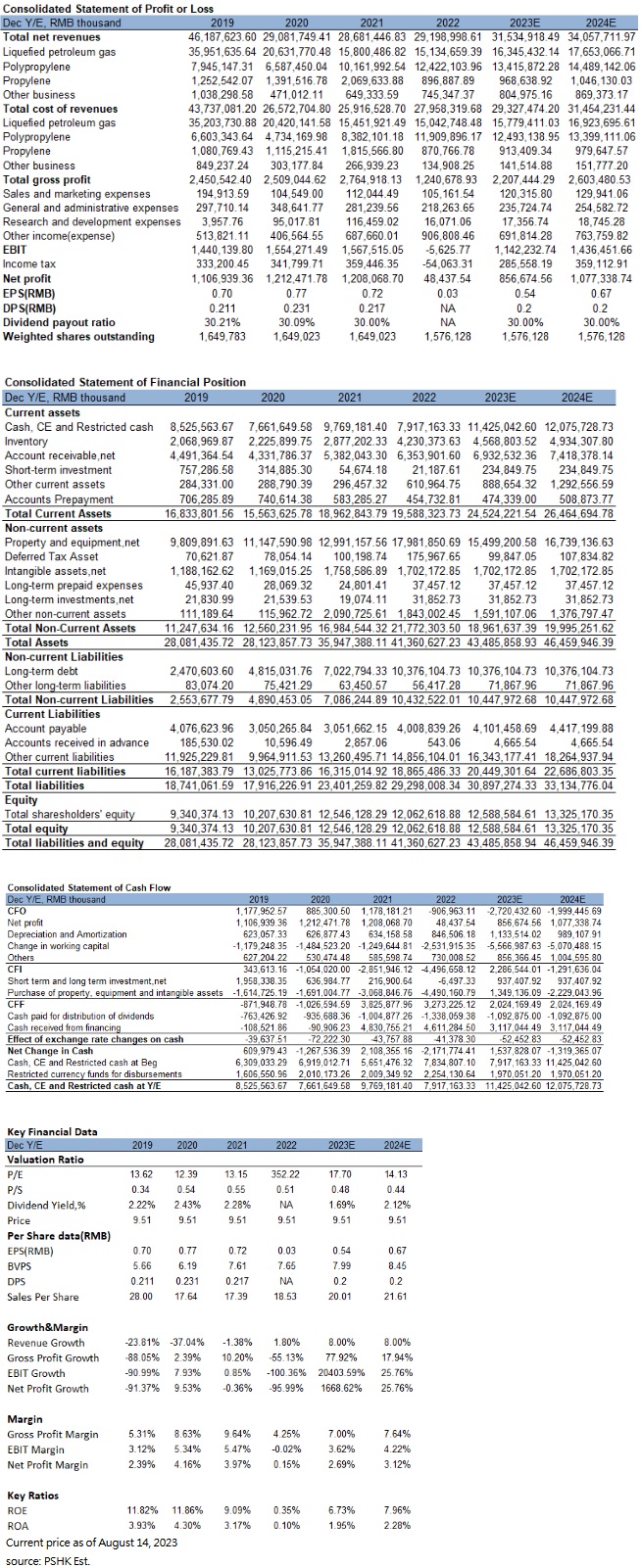

OverviewOriental Energy is a leading propane dehydrogenation (PDH) manufacturer. It has successfully transformed from a world-class LPG integrated operator into a world-leading propane dehydrogenation manufacturer. The company mainly deploys PDH devices and downstream polypropylene devices, and vigorously develops polypropylene high-end composite materials business. The company's PDH production route has great advantages in terms of investment cost, construction period, and production cost. The construction of Maoming Phase I project has made significant progress. It has been fully transferred to the trial run stage. With the completion of Zhangjiagang, Ningbo and Maoming production bases, the company is expected to become the world's largest polypropylene production base. Company performance reviewIn 2022, the company achieved sales revenue of 29.19 billion, a year-on-year increase of 1.8%; net profit attributable to the parent company of 40 million, a year-on-year decrease of 96.7%; earnings per share of 0.027 yuan, a year-on-year decrease of 96.2%. The net profit attributable to shareholders of listed companies after deducting non-recurring gains and losses was 10 million, a year-on-year decrease of 99.2%; the company's gross profit margin was 4.2%, a year-on-year decrease of 5.4 percentage points, and the net profit rate was 0.2%, a year-on-year decrease of 3.8 percentage points. The reason for the decrease in profits is that due to the impact of the Russia-Ukraine war, geopolitical conflicts pushed up the prices of raw materials such as crude oil and propane in the first half of the year. The market prices of propylene and polypropylene rose all the way and then fluctuated at high levels. The prices of propylene and polypropylene are constantly shifting between being affected by high upstream cost prices and being affected by low downstream demand, which has led to pressure on the domestic propylene and polypropylene markets. In the first quarter of 2023, the company achieved operating income of 7.16 billion, a year-on-year increase of 2.5%; realized net profit attributable to the parent company of 50 million, a year-on-year decrease of 51.4%. The performance is slightly lower than the forecast in the first quarter of 2023 to achieve a revenue of 7.8 billion and a net profit of 80 million. Affected by factors such as high raw material prices and insufficient downstream demand, profitability continued to be under pressure, but it recovered significantly from the previous quarter in 2022Q4 and turned losses into profits. Main business analysisPropylene is an important basic raw material product in China's chemical industry and an important monomer of synthetic resin materials. Its downstream products involve construction, automobile, packaging, textile and other fields. The downstream products of propylene are mainly polypropylene, acrylonitrile, propylene oxide, acrylic acid, etc., among which polypropylene is used in the largest amount. There are many varieties of downstream consumption of polypropylene, including drawing, fiber and other varieties. Polypropylene is increasingly widely used in new materials, automobiles, green building materials, medical equipment, food-grade packaging, electrical appliances, etc., and there is still great potential for future demand. In recent years, global polypropylene production capacity has maintained a steady growth trend. From 2018 to 2022, the compound annual growth rate of global polypropylene production capacity was about 6%, and the global polypropylene production capacity in 2022 increased by nearly 4% compared with 2021. With the strong promotion of the domestic "double carbon" strategy, the domestic polyolefin industry will undergo major structural changes in the next few years. The global basic petrochemical industry is transitioning from heavy oil to light resources, and new raw materials, new technologies, and low emissions have become major trends. In the technology roadmap of key areas of "Made in China 2025", high-performance carbon fiber and its composite materials are classified as key strategic materials. The company's deep layout of the acrylonitrile and carbon fiber industry chain has transformed and developed by leaps and bounds again. Of the few propylene production-focused processes, propane dehydrogenation (PDH), which converts low-value propane to high-value propylene, has proven to be the most efficient. The company has transformed into a PDH manufacturer. PDH is to separate the two hydrogens in propane (C3H8) through a catalytic reaction to produce propylene (C3H6) and hydrogen. PDH technology has low energy consumption, more cost advantages, less carbon emissions, which is in line with the domestic clean energy development route. The company has 1.8 million tons/year of PDH and 1.6 million tons/year of polypropylene PP production capacity. The Maoming Phase I project under construction includes 600,000 tons/year of PDH, 400,000 tons/year of PP, and 300,000 tons/year of synthetic ammonia. With the increase of PDH production capacity, the output of by-product hydrogen has also been greatly increased. Under the background of the country's promotion of carbon peaking and carbon neutrality, there is a great potential for hydrogen energy demand. In 2022, the company's polypropylene business achieved revenue of 12.42 billion, a year-on-year increase of 22.2%, accounting for 42.5% of the company's main business revenue. The production volume of polypropylene is 1.627 million tons, and the sales volume is 1.668 million tons. The overall average selling price of the sector is 74.46 Yuan/ton, a year-on-year decrease of 4.7%. The gross profit margin of the polypropylene business was 4.1%, a year-on-year decrease of 13.4 percentage points. The company's propylene business realized revenue of 890 million, a year-on-year decrease of 56.6%, accounting for 3% of the company's main business income. The production volume of propylene was 1.618 million tons, and the sales volume was 133,000 tons, the overall average selling price of the sector was 6,723 yuan/ton, a year-on-year increase of 2.8%. The gross profit margin of the propylene business was 2.9%, a year-on-year decrease of 9.3 percentage points. The reason for the decline in the gross profit of the polypropylene business and the propylene business was that due to the impact of rising global bulk raw material and energy prices, the company's main raw material costs rose, resulting in a decline in profitability. PDH-PP (Propane dehydrogenation-polypropylene) industry profits have narrowed significantly. According to the Global Trade Monitoring and Analysis Center of the General Administration of Customs and the Shanghai Petroleum and Natural Gas Trading Center, the average contract price (CP) of propane in 2022 was US$713/ton, a year-on-year increase of 9%; The average price of PP was 8352 yuan/ton, a year-on-year decrease of 4%. In 2023Q1, the average contract price (CP) of propane was US$647/ton, a decrease of 21% year-on-year and an increase of 8% month-on-month; the average price of PP was 7784 yuan/ton, a decrease of 10% year-on-year and a decrease of 2% month-on-month. The price difference between propylene and propane is usually US$300-500/ton. In terms of international pricing benchmarks, according to the data released by Saudi Aramco in July 2023, the propane contract price (CP) in July was US$400/ton, a decrease of US$50 from the previous month, a decrease of 11.1% from the previous month, and a decrease of 44.8% from the same period last year. The continuous decline in raw material prices is conducive to the recovery of the company's profitability. The company's liquefied petroleum gas business realized revenue of 15.1 billion, a year-on-year decrease of 4.2%, accounting for 51.8% of the company's main business income. The gross profit margin of the liquefied petroleum gas business was 0.6%, a year-on-year decrease of 1.6 percentage points due to the high positive correlation between international price of LPG and crude oil prices. In 2022, the price of LPG showed a trend of rising rapidly and falling slowly. In the first half of the year, due to the conflict between Russia and Ukraine, international oil prices rose strongly. As a by-product of crude oil, the price of LPG jumped to the highest point in the year. In the second half of the year, the cost-side support provided by crude oil and overseas imports weakened, and the demand was weak, resulting in a weaker LPG price shock. From the perspective of crude oil prices, international oil prices rose slightly month-on-month in July. OPEC+ oil-producing countries implemented production cuts and Saudi Arabia promised to reduce production by an additional 1 million barrels per day in July, and Russia's seaborne oil exports fell. In addition, U.S. crude oil inventories have fallen more than expected, and the U.S. has begun to repurchase crude oil to fill its strategic oil reserves, which will help tighten oil supply, thereby prompting a rebound in international oil prices. The recent uptrend of international oil price fluctuations will affect the rise of domestic and foreign LPG market prices, which is conducive to the recovery of the company's profitability. Valuation and recommendationThe price of propane raw materials has a strong correlation with oil prices. Under medium and high oil prices, the profitability of propane dehydrogenation is higher than that of traditional steam cracking processes in refineries. In 2023, international oil prices will be stimulated by the fall of the US dollar, strong demand from China and developing countries, and supply cuts by major oil exporters. It is predicted that the future oil price will be at a medium to high level. In addition, the price reduction promotion policy of new energy vehicles is favorable, and the demand for polypropylene continues to recover, which will bring greater performance flexibility to the recovery of PDH's profitability. After Maoming's production capacity is put into operation in 2023, the company will form a scale advantage, and there is potential for further improvement in gross profit margin. In terms of business development, the by-product hydrogen of the company's PDH project helps the rapid development of the hydrogen energy industry. A large amount of cheap, high-purity by-product hydrogen is produced in the propane dehydrogenation unit, which provides a large amount of low-cost hydrogen for the development of the hydrogen energy industry and reduces the operating cost of the hydrogen energy industry. The government of Maoming strongly promotes the development of hydrogen energy. As the leader in the propane dehydrogenation industry, the company is expected to realize the comprehensive utilization of hydrogen energy and provide income from by-products. We predict that the company's revenue will be 31.5 billion and 34 billion in 2023-2024 respectively, with a compound annual growth rate of 8%, and sales per share will be 20.01/21.61x, corresponding to a price-to-sales ratio (P/S) of 0.48/ 0.44 x. The company's average P/S in the past three years was about 0.57x. We give the company 0.55 times P/S in 2023, and a target price of 11 RMB, with a "buy" rating. (Current price as of August 14) Risk factorsRaw material prices fluctuate, downstream demand falls short of expectations, and the industry has overcapacity.

Financial

Click Here for PDF format...

| Recommendation on 4-9-2023 | | Recommendation | Buy | | Price on Recommendation Date | $ 9.510 | | Suggested purchase price | N/A | | Target Price | $ 11.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|