|

MENGNIU DAIRY(2319)

Analysis:

Focusing on the three key strategic approaches of “Greener, More Nutritious and Smarter”, MENGNIU DAIRY (2319) achieved stable and high-quality growth. Its core business demonstrated strong and resilient growth momentum while its innovation business made significant breakthroughs, bolstering the overall strengths of its brand. The revenue of the Group amounted to RMB51,118.5 million for the six months ended 30 June 2023, representing a year-on-year increase of 7.1%. Benefiting from cost reduction, efficiency enhancement and product structure improvement, the Group`s operating profit increased by 29.9% year-on-year to RMB3,274.9 million, while its operating profit margin increased to 6.4%, representing a significant year-on-year increase of 110 basis points. In terms of developing rare nutritional ingredients, the HMO developed by Mengniu has passed the safety assessment of the Ministry of Agriculture and Rural Affairs of China and the technical review of the National Health Commission, making Mengniu the first domestic dairy company to successfully develop an HMO and obtain an approval from the Chinese regulatory authority. The HMO will be industrialized in the future. HMO is the third largest solid component in breast milk, behind lactose and fat, but ahead of protein. It has important health effects, such as regulating immunity, helping brain development and regulating intestinal flora. However, it is very scarce and is difficult to obtain from cow`s milk or goat`s milk. With regard to other innovative business, in February 2023, Mengniu launched China`s first liquid protein nutritional supplement, M-ACTION Sports Protein Drink, entering the field of sports nutrition. (I do not hold the above stock)

Strategy:

Buy-in Price: $27.20, Target Price: $30.00, Cut Loss Price: $25.80

|

CSPC PHARMA(1093)

Analysis:

CSPC reported a revenue of 16.08 billion yuan in the first half of 2023, a year-on-year increase of 3%; Shareholders should account for a profit of 3.16 billion yuan, an increase of 3% year-on-year.. From a segmented perspective, the revenue of functional food businesses such as patent drugs, raw materials, and caffeine increased by 5.2%, -9.6%, and 3.5% year-on-year, respectively. The stable business of traditional Chinese medicine is mainly due to the rebound of the neural line month on month and the narrowing of the decline in tumors/cardiovascular diseases; Revenue from raw materials remains low (due to the impact of declining VC and caffeine prices). Several new drugs of the company were submitted to the market. The COVID-19 mRNA vaccine containing the BA.5 core mutation site independently developed by the company, Duente, was included in the emergency use of the country in March 2023. The whole human source PD-1 enransubizumab, amphotericin B liposome for the treatment of deep fungal infection, and oral DPP-4 inhibitor Prugliptin tablets Omazzumab for chronic spontaneous urticaria and Bartolizumab for the treatment of systemic myasthenia gravis have been approved for marketing. At present, the company has 60 drugs in the clinical or application stage, 8 have submitted marketing applications, and 16 are in the critical clinical NDA stage II/III.

Strategy:

Buy-in Price: $5.56, Target Price: $6.70, Cut Loss Price: $4.89

|

|

Binhai Investment (2886.HK) - Gas prices expect to fall in 2H, drive financial performance for the year

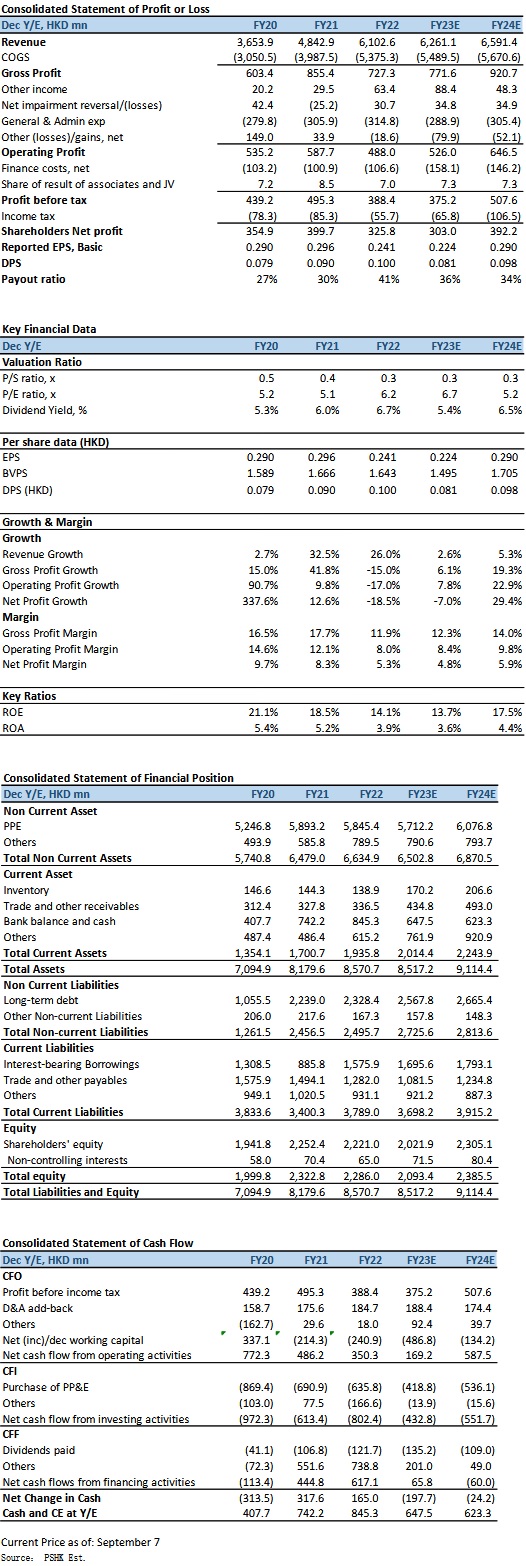

Binhai Investment Company Limited (Binhai) is principally engaged in the sales of piped natural gas, construction and gas pipeline installation service and gas passing through service. The natural gas business of Binhai Investment and its subsidiaries is distributed in seven provinces and two cities across the country, with a total of 40 gas project companies. At present, the largest shareholder of Binhai Investment is Tianjin TEDA Investment Holding Company, holding 40.00% of Binhai's shares, and the second largest shareholder is Sinopec Great Wall Gas Investment Company, holding 29.99% of Binhai's shares. Suffer from rising purchase cost of natural gas in 2022, 1H margins under pressure In FY2022, total revenue of Binhai amounted to HK$6102 million (FY2021: HK$4843 million), representing an increase of 26.0% YoY. Profit attributable to equity owners of the Company was HK$326 million (FY2021: HK$400 million), representing a decrease of 18.5% YoY. Profit attributable to equity owners of the company excluding the net foreign exchange loss recognized (FY2022: net exchange loss of HK$84 million) in profit or loss amounted to HK$410 million, representing an increase of 9% YoY. The number of regular customers from the construction and installation of gas engineering works of the company increased by 106 thousand, down by 35% YoY, and the aggregate number of customers amounted to 2299 thousand. The recorded sales volume of piped natural gas was 2.03 billion cubic metres, up by 3% YoY, among which the sales volume of pipeline gas amounted for 1.44 billion cubic metres, up by 15% YoY, and achieved 0.59 billion cubic metres of natural gas pipeline transmission for the year, down by 17% YoY. Gross profit was HK$727 million (FY2021: HK$855 million) and the gross profit margin was 11.9% (FY2021: 17.7%). The decrease in gross profit margin was mainly due to the increase in purchase cost of natural gas.

In 1HFY2023, total revenue of Binhai amounted to HK$3119 million (1HFY2021: HK$3047 million), representing an increase of 2.4% YoY. As the high price of gas supply last year was extended to the 1Q of 2023, caused the cost increased, and the real estate industry continued to operate at a low level, which affected the performance of the connection business. During the period, the gross profit fell by 11.4% YoY to HK$384 million; the gross profit margin dropped to 12.3% (1HFY2022: 14.2%). The profit attributable to owners of the company was HK$166 million during the period, representing a decrease of 35.5% YoY. Such decrease was mainly because of the decrease of gross profit and the increase of finance costs. Basic EPS were HK$12.31 cents, representing a decrease of HK$6.78 cents for the corresponding period last year. In terms of operating segments, sales of piped natural gas amounted to HK$2790 million, representing an increase of 5%, accounting for about 89.6% of total revenue, due to the increase in natural gas sales volume and the increase in unit price of sales. During the Period, the sales volume of piped natural gas by domestic and industrial users was approximately 183 million cubic meters and 581 million cubic meters respectively, consumption of piped natural gas amounted to 6,433 x 106 and 20,408 x 106 mega-joules respectively, a slight decrease of 0.8% and an increase of 10.0% YoY. The overall pipeline gas sales volume was 764 million cubic meters, a YoY increase of about 7.2%, and has reached about 50% of the FY2023 target. In terms of gross difference, it has increased by RMB 0.03 YoY in 1HFY2023, and increased by RMB 0.05 MoM, indicating that the recovery of gross difference is optimistic.

Income from construction and gas pipeline installation service (constructs gas pipelines for its clients and connects such pipelines to the company's main gas pipeline networks. The company then charges construction and gas pipeline installation service fees from industrial and commercial customers, property developers and property management companies) amounted to approximately HK$300 million, representing a decrease of 11% YoY, accounting for about 9.6% of total revenue. During the period, the number of new customer contracts increased by exceeded 61,000, and the cumulative number of customers exceeded 2.36 million, representing a 4.5% YoY growth. As at 30 June 2023, the aggregate length of city medium-pressure gas pipeline networks was 3,825 kilometers, representing an increase of 104 kilometers, while the aggregate length of high-pressure and sub-high-pressure gas pipeline networks was 649 kilometers, representing an increase of 1 kilometer from the length of 648 kilometers as at 31 December 2022.

For the gas passing through service, the company transports gases for clients through gas pipeline networks and charges passing through fees. During the Period, the volume of gases transported by the company for its clients amounted to 313 million cubic meters and gas passing through service income amounted to HK$26 million, representing a decrease of 17%, accounting for about 0.8% of total revenue.

Gas prices continue to fall in 2H, drive financial performance for the year In the first half of 2023, national natural gas consumption reached 194.1 billion cubic meters, representing a year-on-year increase of 5.6%. In its quarterly Natural Gas Market Report, the International Energy Agency indicated that it expects China's natural gas consumption to grow by more than 6% in 2023, providing support to the Asia region's overall natural gas consumption growth of nearly 3%. Last year, the industry was plagued by the problem of low dollar margins and the high price of gas supply was extended to the first quarter of this year. Nevertheless, Binhai managed to stabilize its dollar margins in the first half of the year through by the recovery of domestic consumption and favorable policies for the industry. The average monthly Henry Hub Natural Gas Spot Price in the US fell by 34% in the first half of 2023, while the price of natural gas in Europe fell by more than 60% this year. Looking ahead to the second half of the year, gas prices will continue to fall, and the rebound in gross profit will be supported by the increase in gas sales prices. Coupled with the resilience of the company's business income, the rebound in gross profit is expected to drive the Binhai's financial performance for the year as a whole. Investment ThesisSince the beginning of the year, a lot of places in China have been promoting the improvement of the upstream and downstream price linkage mechanism for natural gas. Since June, the local development and reform commissions have successively introduced policies for residents to follow the price. As of August 2023, A total of 11 subsidiaries of the company in Hebei, Shandong and Jiangsu have completed price adjustments, ranging from RMB 0.16 to RMB 0.47, with an increase ranging from 5.7% to 19.2%. It is expected to have a certain boost to further repairing the gross difference in the 2H of 2023. The improvement of the price adjustment mechanism is conducive to the recovery and stability of natural gas price differentials, and it eases the procurement pressure of city fuel enterprises. In addition, Sinopec Natural Gas has also agreed to support the Group in lowering the cost of natural gas procurement through trading and the formation of a profit model for the trading business through its superiority in upstream resources, assist the company to meet the requirements of relevant natural gas storage and peak-shaving policy requirements and the development of gas trading business, and help the company connect upstream resources and downstream markets to open up the industrial chain. In the future, there will still be room for natural gas price rationalization adjustment, and the consumption attributes of natural gas will continue to be strengthened. In terms of business expansion, the company stated that it is accelerating the development of the integrated energy business. In addition to provide comprehensive customized development and utilization solutions for new and clean energy such as photovoltaic and geothermal energy in the TEDA Science and Technology Innovation City. Binhai Investment (Tianjin) and Sinopec New Star (Tianjin) New Energy Company Limited entered into the Cooperation Framework Agreement for Integrated Energy Project to cooperate closely in the fields of energy integrated management, integrated energy development, distributed energy planning, construction, and operation; Meanwhile, the company also entered into a strategic framework agreement with Tianjin Capital Environmental Protection Group on the heating service of the energy supply project in Balitai Town, and jointly promote the comprehensive energy heating method that combines regenerative water source heat pumps and gas boilers. We expect FY2023E-FY2024E EPS to be HK$0.224 and HK$0.290 respectively, with PT of HK$2.20, implies a FY2023E P/E of 9.9x (~5-yrs historical average). Our investment rating is “Buy”. Risk factors1) Natural gas procurement costs rise more than expected; 2) Large fluctuations in RMB; 3) Economic recovery momentum slower than expected. Financial

Click Here for PDF format...

| Recommendation on 13-9-2023 | | Recommendation | Buy | | Price on Recommendation Date | $ 1.500 | | Suggested purchase price | N/A | | Target Price | $ 2.200 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|