|

WEICHAI POWER(2338)

Analysis:

WEICHAI POWER`s (2338) businesses comprise four segments, namely power system, commercial vehicle, agricultural equipment and intelligent logistics. Based on its positive profit alert being issued recently, tthe Group is expected to record approximately RMB5,961 million to RMB6,624 million in the net profit attributable to the shareholders of the parent for the nine months ended 30 September 2023, representing an increase of approximately 80% to 100% as compared with that for the nine months ended 30 September 2022. Such increase in the net profit attributable to the shareholders of the parent was mainly due to the fact that during the nine months ended 30 September 2023, the Company seized opportunities such as the recovery of demand in the heavy duty truck industry and the strong demand in export markets, and constantly promoted the restructuring of its products, business and market structure, which drove the performance of the Company to achieve a substantial year-on-year growth. Going forward, under the national economic tone of “stabilizing infrastructure, expanding consumption, protecting people`s livelihood, and preventing risks”, and coupled with export demand, the recovery of consumption will play a supporting role in bulk logistics and trunk logistics and drive the overall sales level of heavy-duty trucks. The gradual acceleration of infrastructure investment will drive the demand for construction vehicles such as dump trucks and mixer trucks. As evidenced by the spring plowing three-summer operation experience, customers` recognition of National IV agricultural equipment products has increased significantly. The demand for renewal of agricultural machinery will gradually pick up. (I do not hold the above stock)

Strategy:

Buy-in Price: $11.00, Target Price: $12.10, Cut Loss Price: $10.50

|

BYD COMPANY(1211)

Analysis:

The company announced its performance forecast for the first three quarters, predicting net profit for the first three quarters of 20.5 billion yuan to 22.5 billion yuan, a year-on-year increase of 120.16% to 141.64%. Net profit in the third quarter was 9.5 billion to 11.5 billion yuan, a year-on-year increase of 67% to 102%, exceeding market expectations. In the third quarter, the output of new energy vehicles reached 837,000 units, a year-on-year increase of 54.1%; sales reached 824,000 units, a year-on-year increase of 52.9%, and a month-on-month increase of 17.1%. Sales and profits in a single quarter hit new highs. A total of 71,000 new energy vehicles were exported in the third quarter, a year-on-year increase of 3.23 times. Overseas vehicles are sold at higher prices and contribute higher gross profits. Even as price competition for electric vehicles intensifies, BYD's net profit per vehicle still reaches a record high, mainly due to continued sales growth, increased brand premiums, good cost control, and an increase in export sales contribution to 9%.

Strategy:

Buy-in Price: $257.40, Target Price: $280.60, Cut Loss Price: $234.48

|

|

Fuyao Glass (3606.HK) - High-value-added Products` Proportion Continue to Rise

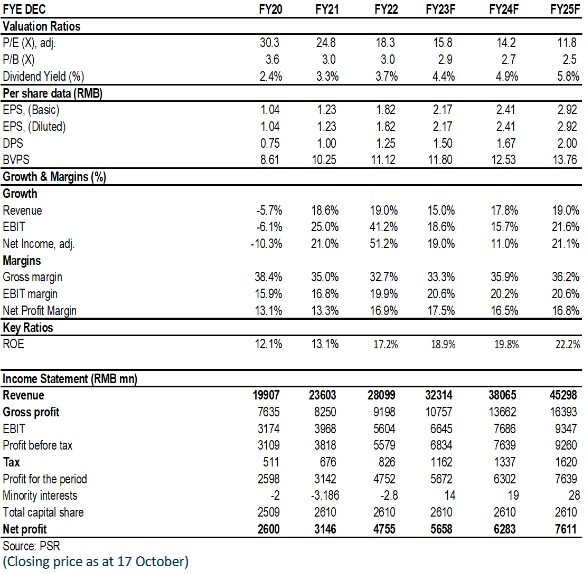

Investment SummaryRevenue in Q2 Hits a Record High, Core Profitability Is Robust Fuyao Glass (hereinafter referred to as the “Company”) released its 2023 Interim Report. In the first half of 2023, the Company recorded the operating revenue of RMB15,031 million, with a year-on-year increase of 16.49%, higher than the overall growth rate of 10% of the downstream automotive industry. The net profit attributable to the parent company stood at RMB2,836 million, up by 19.07% year-on-year. Less non-recurring profit or loss, the figures will become RMB2,793 million and 20.89%. In the first and second quarters this year, the operating revenue was RMB7,052 million and RMB7,979 million, rising by 7.7% and 25.5% year-on-year, respectively, while the net profit attributable to the parent company amounted to RMB915 million and RMB1,922 million, climbing by 4.97% and 27.21% year-on-year, respectively. The earnings hit a record high in the second quarter mainly because of the increased proportion of high-value-added products, which continued to improve the product structure, and decreased ocean freight.During the Reporting Period, the profit before tax grew by 24.36% from the same period of 2022. Additionally, exchange, decreased ocean freight, increased energy prices, and the increased prices of sodium carbonate affected the profit before tax by RMB90 million, RMB153 million, -RMB114million, and -RMB38 million, respectively. Less such influencing factors, the profit before tax would go up by 25.89% from the same period last year. Core earnings showed a rapid growth. Fuyao Glass` gross margin in the first half of the year was 34.14%, down by 0.08 ppts year-on-year, mainly due to the decrease of the gross margin of float glass by 2.1 ppts. Yet, the gross margin of automobile glass increased by 0.35 ppts year-on-year to 29.37%. The second quarter witnessed good gross margin, up by 2.3 ppts and 1.8 ppts year-on-year and quarter-on-quarter, respectively. We estimate that the main reasons include the continuous improvement in the Company's product structure, the favourable trends of exchange rates, the quarter-on-quarter rally of float glass, and the decreased ocean freight. The overall expenses in the first half of the year were diluted, as the revenue rose: The marketing expense ratio, the management expense ratio, and the R&D expense ratio were 4.81%, 7.66%, and 4.44%, respectively, wherein the first two indicators dropped by 0.3 ppts and 0.62 ppts year-on-year, while the third one increased by 0.22 ppts year-on-year. High-value-added Products` Proportion Continue to Rise The Company maintained high R&D input to push forward the upgrade of product technology and the added value of products. The adoption of new energy and smart solutions in the automotive industry has further raised the glass ratio per vehicle. Therefore, Fuyao Glass` average sales price (ASP) continues rising. In the first half of the year, the proportion of high-value-added products, including ceiling glass, HUD, camera glass, coated glass, and tempered soundproof car door glass, grew by approximately 10.1 ppts to 52.4%. The ASP of automobile glass increased by approximately 10%. The future trend of automobile glass to be safe, comfortable, energy-saving, environmentally friendly, intelligent, and integrated will bring structured opportunities for the Company regarding the sales of automobile glass. The Company completed the capital expenditure of RMB2.46 billion, with a year-on-year increase of 98.3%, accounting for 38.5% of the planned capital expenditure for the whole year. It is estimated that the capital expenditure concentrated mainly on the capacity expansion of high-value-added products and the production expansion of domestic aluminium trim business. As at the end of the first half of the year, the Company enjoyed a favourable financial profile, had RMB19.4 billion cash&bank deposit in hand, and was in a net cash position. Investment ThesisIn the short run, the prices of raw materials and energy may decline in the second half of the year. The subsequent loss reduction of SAM and the continuous capacity expansion of the American factory will hopefully bring more potential profitability. In the medium and long run, we expect that, of automobile glass, high-value-added products` proportion will still increase. As a global leader in automobile glass, the Company will probably continue to benefit from industrial advantages. The Company has also raised funds to enter the field of photovoltaic glass, and has been expanding its product scope to open room for long-term sustainable development. We forecast its EPS to be RMB 2.17/2.41/2.92 in 2023/2024/2025E. Overall, considering the steady leading position, continuous optimization of the product structure and a high dividend rate, we give the "BUY" rating, with a revised target price to be HK$45.7, equivalent to 19.4/17.5/14.4x P/E for 2023/2024/2025E. (Closing price as at 17 October) RisksDemand for automobiles keeps sluggish; cost of raw materials increases; RMB appreciates CatalystSuccess market development of overseas automobile market; rebound of domestic demand for automobile; depreciation of RMB Financials

Click Here for PDF format...

| Recommendation on 19-10-2023 | | Recommendation | BUY | | Price on Recommendation Date | $ 37.250 | | Suggested purchase price | N/A | | Target Price | $ 45.700 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2023 Phillip Securities (HK) Ltd. All Rights Reserved.

|